Updated on June 3rd, 2026 by Bob Ciura

The average dividend yield in the S&P 500 Index remains low at just 1.2%.

As a result, income investors should focus on higher-yielding securities, if they want additional income from their stock portfolios.

Even better, investors can buy high dividend stocks when they are also undervalued, which could lead to high total returns in the coming years.

After all, the goal of rational investors is to maximize total return under a given set of constraints. High dividend stocks can contribute a significant portion of a stock’s total return.

With this in mind, we compiled a list of high dividend stocks with dividend yields above 4%. You can download your free copy of the high dividend stocks list by clicking on the link below:

The free high dividend stocks list spreadsheet has our full list of ~200 individual securities (stocks, REITs, MLPs, etc.) with 4%+ dividend yields.

Interestingly, all returns come from only three sources:

Dividends (or distributions, interest, etc.)

Growth on a per share basis (typically measured as earnings-per-share)

Valuation multiple changes (typically measured as a change in the price-to-earnings ratio)

Combined, these three sources make up total return.

Historical total return, while interesting, is not what matters in investing. It’s expected future returns that we care about.

And since total returns can only come from the three sources mentioned above, you can use the expected total return framework to clarify your thinking on where you expect total returns to come from.

The following list represents the 10 most undervalued stocks in the Sure Analysis Research Database that also have yields above 4%.

The 10 undervalued hidden gems below are sorted by expected return from valuation changes, from lowest to highest.

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

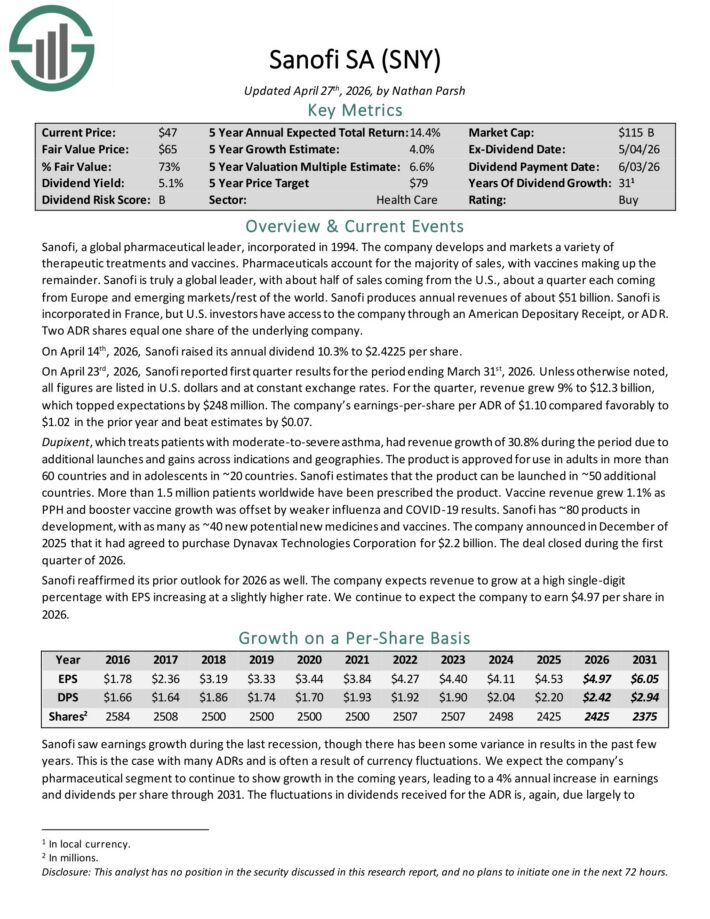

Undervalued Hidden Gem #10: Sanofi (SNY)

Annual Valuation Return: 8.7%

Dividend Yield: 5.7%

Sanofi is a global pharmaceutical leader that develops a variety of therapeutic treatments and vaccines.

Pharmaceuticals account for the majority of sales, with vaccines making up the remainder. Sanofi produces annual revenues of about $51 billion.

Sanofi is incorporated in France, but U.S. investors have access to the company through an American Depositary Receipt, or ADR. Two ADR shares equal one share of the underlying company.

On April 14th, 2026, Sanofi raised its annual dividend 10.3% to $2.4225 per share.

On April 23rd, 2026, Sanofi reported first quarter results for the period ending March 31st, 2026. For the quarter, revenue grew 9% to $12.3 billion, which topped expectations by $248 million.

Earnings-per-share per ADR of $1.10 compared favorably to $1.02 in the prior year and beat estimates by $0.07.

Dupixent, which treats patients with moderate-to-severe asthma, had revenue growth of 30.8% during the period due to additional launches and gains across indications and geographies.

The product is approved for use in adults in more than 60 countries and in adolescents in ~20 countries. Sanofi estimates that the product can be launched in ~50 additional countries.

Click here to download our most recent Sure Analysis report on SNY (preview of page 1 of 3 shown below):

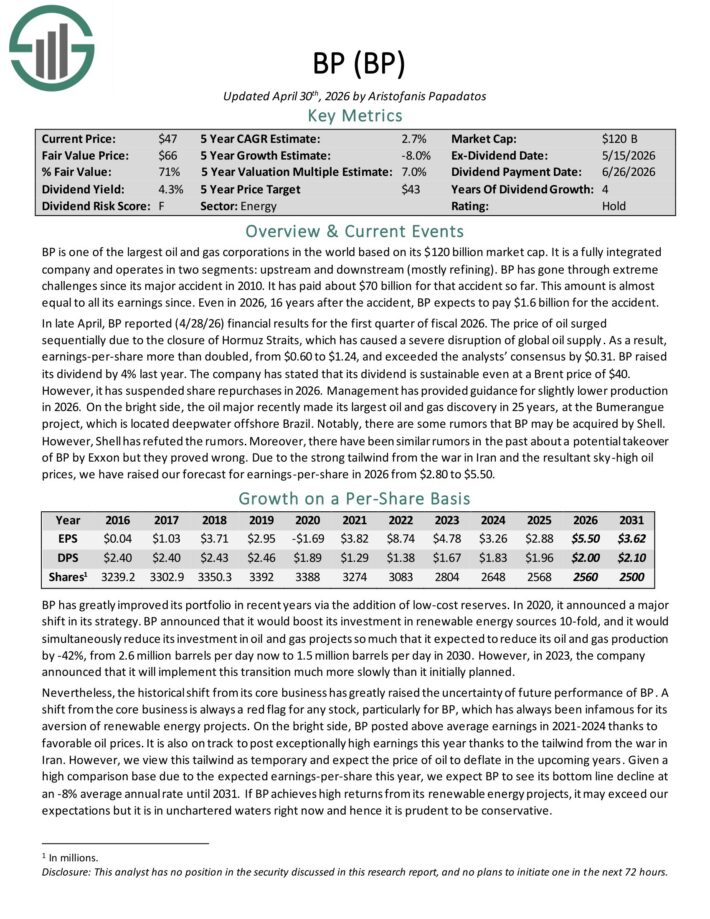

Undervalued Hidden Gem #9: BP plc (BP)

Annual Valuation Return: 8.7%

Dividend Yield: 4.6%

BP is one of the largest oil and gas corporations in the world. It is a fully integrated company and operates in two segments: upstream and downstream (mostly refining).

In late April, BP reported (4/28/26) financial results for the first quarter of fiscal 2026. The price of oil surged sequentially due to the closure of Hormuz Straits, which has caused a severe disruption of global oil supply.

As a result, earnings-per-share more than doubled, from $0.60 to $1.24, and exceeded the analysts’ consensus by $0.31.

BP raised its dividend by 4% last year. The company has stated that its dividend is sustainable even at a Brent price of $40. However, it has suspended share repurchases in 2026.

Management has provided guidance for slightly lower production in 2026. On the bright side, the oil major recently made its largest oil and gas discovery in 25 years, at the Bumerangue project, which is located deepwater offshore Brazil.

Click here to download our most recent Sure Analysis report on BP (preview of page 1 of 3 shown below):

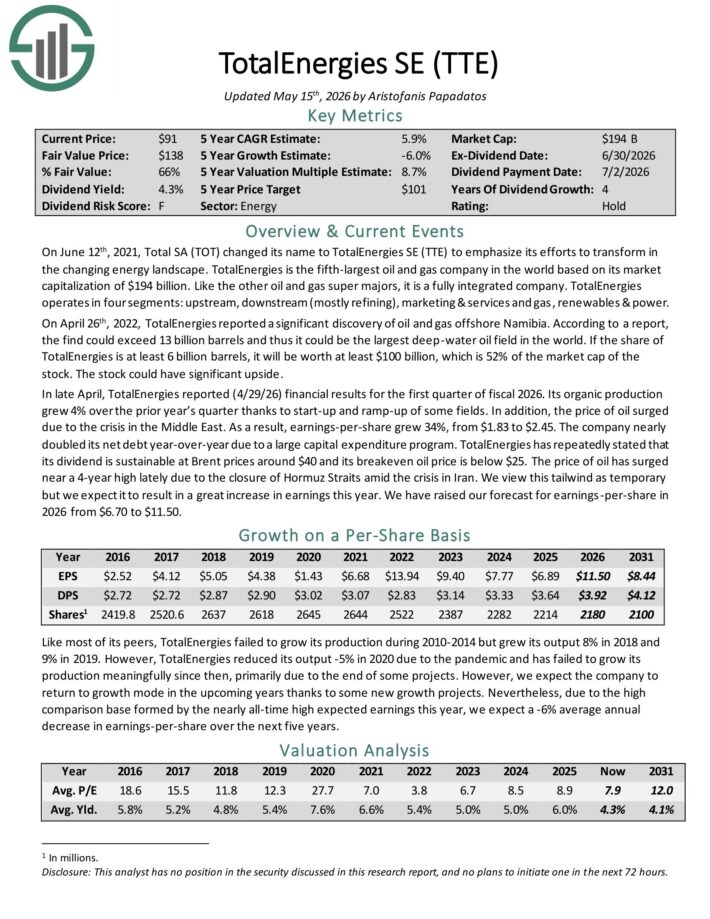

Undervalued Hidden Gem #8: TotalEnergies SE (TTE)

Annual Valuation Return: 9.1%

Dividend Yield: 4.4%

TotalEnergies is the fifth-largest oil and gas company in the world based on its market capitalization. Like the other oil and gas super majors, it is a fully integrated company.

TotalEnergies operates in four segments: upstream, downstream (mostly refining), marketing & services and gas, renewables & power.

In late April, TotalEnergies reported (4/29/26) financial results for the first quarter of fiscal 2026. Its organic production grew 4% over the prior year’s quarter thanks to start-up and ramp-up of some fields.

In addition, the price of oil surged due to the crisis in the Middle East. As a result, earnings-per-share grew 34%, from $1.83 to $2.45.

Click here to download our most recent Sure Analysis report on TTE (preview of page 1 of 3 shown below):

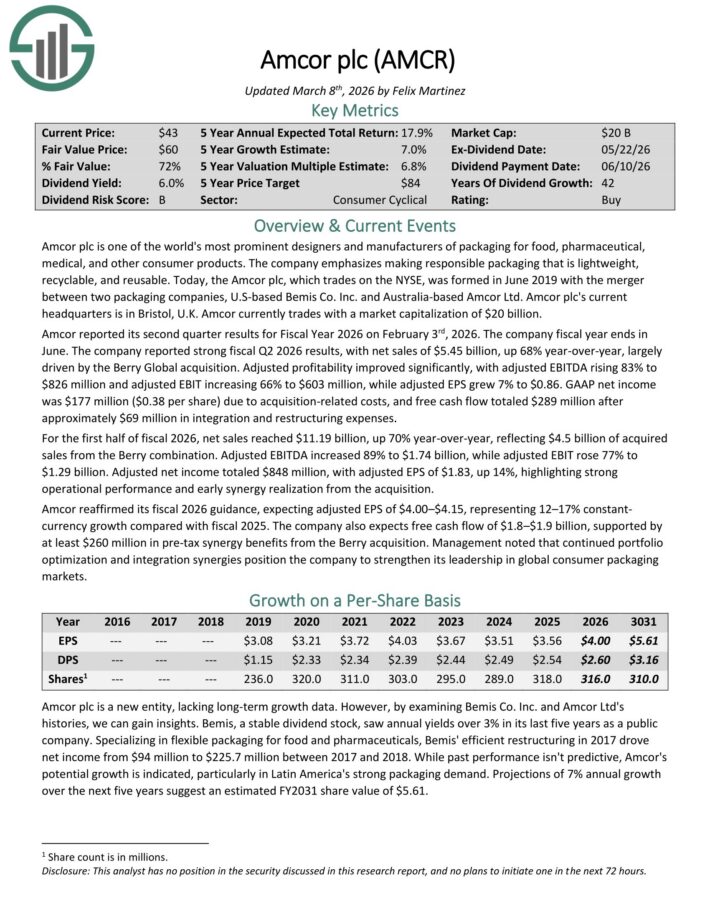

Undervalued Hidden Gem #7: Amcor plc (AMCR)

Annual Valuation Return: 9.1%

Dividend Yield: 6.7%

Amcor plc is one of the world’s most prominent designers and manufacturers of packaging for food, pharmaceutical, medical, and other consumer products.

Amcor reported its second quarter results for Fiscal Year 2026 on February 3rd, 2026. The company reported strong fiscal Q2 2026 results, with net sales of $5.45 billion, up 68% year-over-year, largely driven by the Berry Global acquisition.

Adjusted profitability improved significantly, with adjusted EBITDA rising 83% to $826 million and adjusted EBIT increasing 66% to $603 million, while adjusted EPS grew 7% to $0.86.

GAAP net income was $177 million ($0.38 per share) due to acquisition-related costs, and free cash flow totaled $289 million after approximately $69 million in integration and restructuring expenses.

For the first half of fiscal 2026, net sales reached $11.19 billion, up 70% year-over-year, reflecting $4.5 billion of acquired sales from the Berry combination.

Amcor reaffirmed its fiscal 2026 guidance, expecting adjusted EPS of $4.00–$4.15, representing 12–17% constant currency growth compared with fiscal 2025.

The company also expects free cash flow of $1.8–$1.9 billion, supported by at least $260 million in pre-tax synergy benefits from the Berry acquisition.

Click here to download our most recent Sure Analysis report on AMCR (preview of page 1 of 3 shown below):

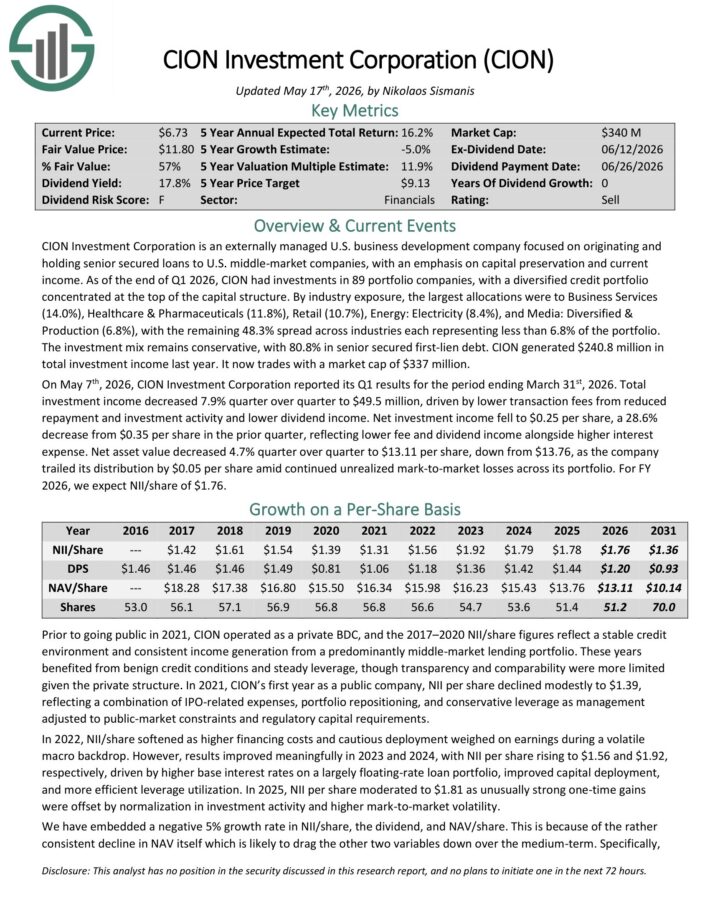

Undervalued Hidden Gem #6: CION Investment Corp. (CION)

Annual Valuation Return: 11.0%

Dividend Yield: 17.1%

ION Investment Corporation is an externally managed U.S. business development company focused on originating and holding senior secured loans to U.S. middle-market companies, with an emphasis on capital preservation and current income.

As of the end of Q1 2026, CION had investments in 89 portfolio companies, with a diversified credit portfolio concentrated at the top of the capital structure.

By industry exposure, the largest allocations were to Business Services (14.0%), Healthcare & Pharmaceuticals (11.8%), Retail (10.7%), Energy: Electricity (8.4%), and Media: Diversified & Production (6.8%).

The remaining 48.3% is spread across industries each representing less than 6.8% of the portfolio. The investment mix remains conservative, with 80.8% in senior secured first-lien debt.

On May 7th, 2026, CION Investment Corporation reported its Q1 results. Total investment income decreased 7.9% quarter over quarter to $49.5 million, driven by lower transaction fees from reduced repayment and investment activity and lower dividend income.

Net investment income fell to $0.25 per share, a 28.6% decrease from $0.35 per share in the prior quarter, reflecting lower fee and dividend income alongside higher interest expense. Net asset value decreased 4.7% quarter over quarter to $13.11 per share, down from $13.76.

Click here to download our most recent Sure Analysis report on CION (preview of page 1 of 3 shown below):

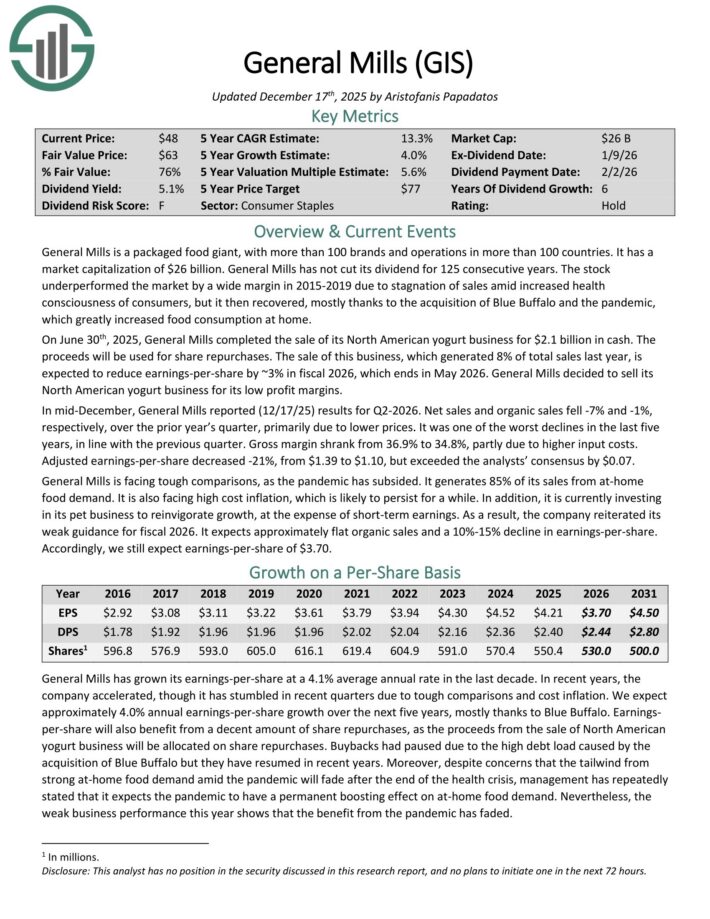

Undervalued Hidden Gem #5: General Mills (GIS)

Annual Valuation Return: 11.1%

Dividend Yield: 7.4%

General Mills is a packaged food giant, with more than 100 brands and operations in more than 100 countries. It has a market capitalization of $26 billion. General Mills has not cut its dividend for 125 consecutive years.

On June 30th, 2025, General Mills completed the sale of its North American yogurt business for $2.1 billion in cash. The proceeds will be used for share repurchases.

The sale of this business, which generated 8% of total sales last year, is expected to reduce earnings-per-share by ~3% in fiscal 2026, which ends in May 2026. General Mills decided to sell its North American yogurt business for its low profit margins.

In mid-December, General Mills reported (12/17/25) results for Q2-2026. Net sales and organic sales fell -7% and -1%, respectively, over the prior year’s quarter, primarily due to lower prices.

It was one of the worst declines in the last five years, in line with the previous quarter. Gross margin shrank from 36.9% to 34.8%, partly due to higher input costs.

Adjusted earnings-per-share decreased -21%, from $1.39 to $1.10, but exceeded the analysts’ consensus by $0.07.

General Mills is facing tough comparisons, as the pandemic has subsided. It generates 85% of its sales from at-home food demand. It is also facing high cost inflation, which is likely to persist for a while.

In addition, it is currently investing in its pet business to reinvigorate growth, at the expense of short-term earnings.

As a result, the company reiterated its weak guidance for fiscal 2026. It expects approximately flat organic sales and a 10%-15% decline in earnings-per-share.

Click here to download our most recent Sure Analysis report on GIS (preview of page 1 of 3 shown below):

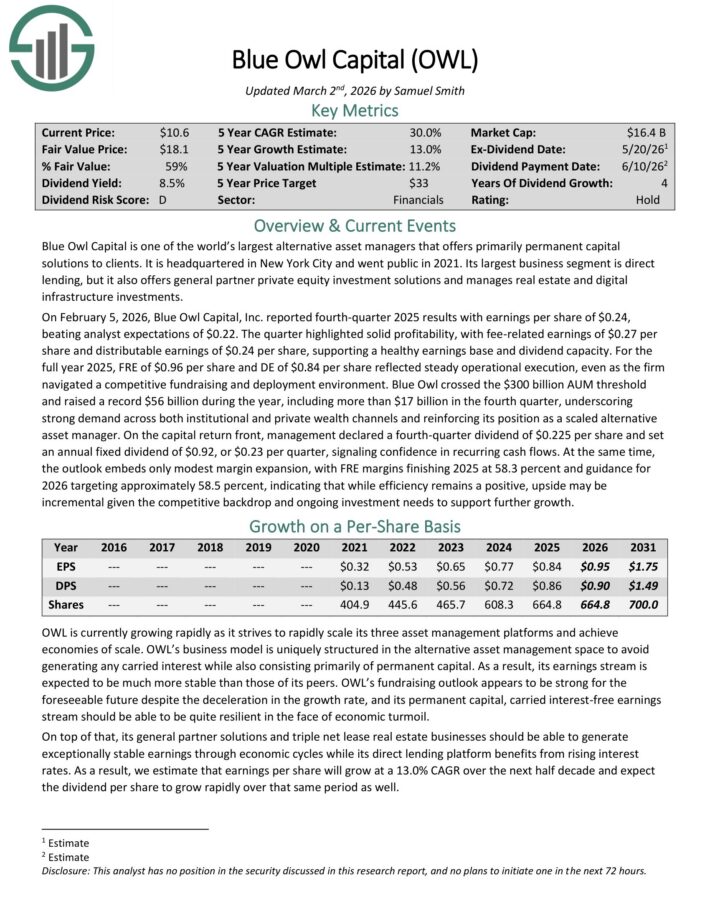

Undervalued Hidden Gem #4: Blue Owl Capital (OWL)

Annual Valuation Return: 12.3%

Dividend Yield: 9.1%

Blue Owl Capital is one of the world’s largest alternative asset managers that offers primarily permanent capital solutions to clients.

It is headquartered in New York City and went public in 2021. Its largest business segment is direct lending, but it also offers general partner private equity investment solutions and manages real estate and digital infrastructure investments.

On February 5, 2026, Blue Owl Capital, Inc. reported fourth-quarter 2025 results with earnings per share of $0.24, beating analyst expectations of $0.22.

Fee-related earnings were $0.27 per share and distributable earnings were $0.24 per share, supporting a healthy earnings base and dividend capacity.

For the full year 2025, FRE of $0.96 per share and DE of $0.84 per share reflected steady operational execution, even as the firm navigated a competitive fundraising and deployment environment.

Click here to download our most recent Sure Analysis report on OWL (preview of page 1 of 3 shown below):

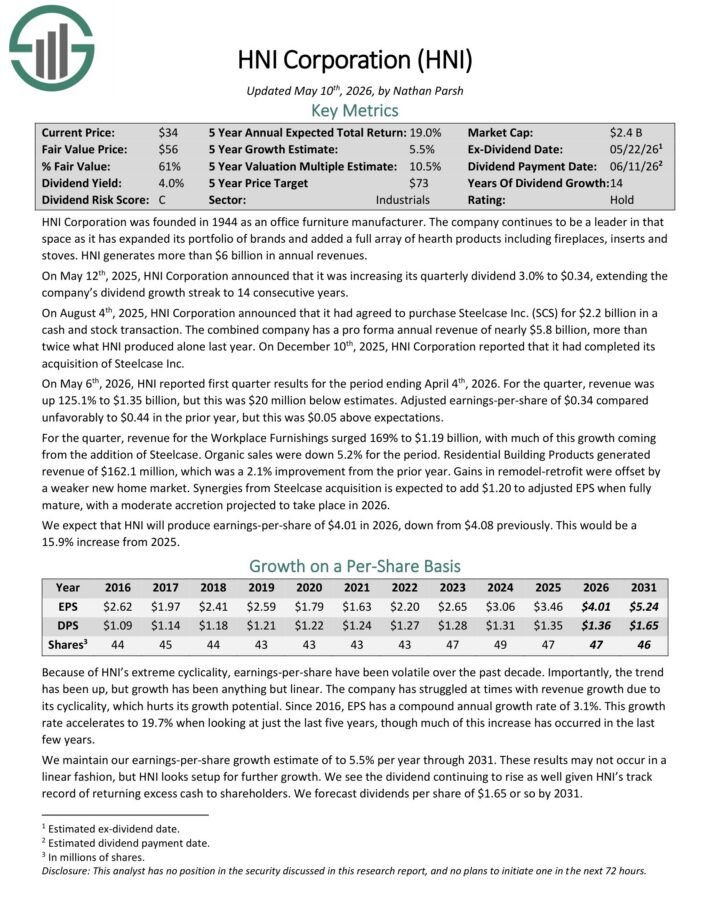

Undervalued Hidden Gem #3: HNI Corp. (HNI)

Annual Valuation Return: 12.7%

Dividend Yield: 4.6%

HNI Corporation was founded in 1944 as an office furniture manufacturer. The company has a full array of hearth products including fireplaces, inserts and stoves. HNI generates more than $6 billion in annual revenue.

On May 6th, 2026, HNI reported first quarter results for the period ending April 4th, 2026. For the quarter, revenue was up 125.1% to $1.35 billion, but this was $20 million below estimates.

Adjusted earnings-per-share of $0.34 compared unfavorably to $0.44 in the prior year, but this was $0.05 above expectations.

For the quarter, revenue for the Workplace Furnishings surged 169% to $1.19 billion, with much of this growth coming from the addition of Steelcase. Organic sales were down 5.2% for the period.

Residential Building Products generated revenue of $162.1 million, which was a 2.1% improvement from the prior year. Gains in remodel-retrofit were offset by a weaker new home market.

Synergies from Steelcase acquisition is expected to add $1.20 to adjusted EPS when fully mature, with a moderate accretion projected to take place in 2026.

Click here to download our most recent Sure Analysis report on HNI (preview of page 1 of 3 shown below):

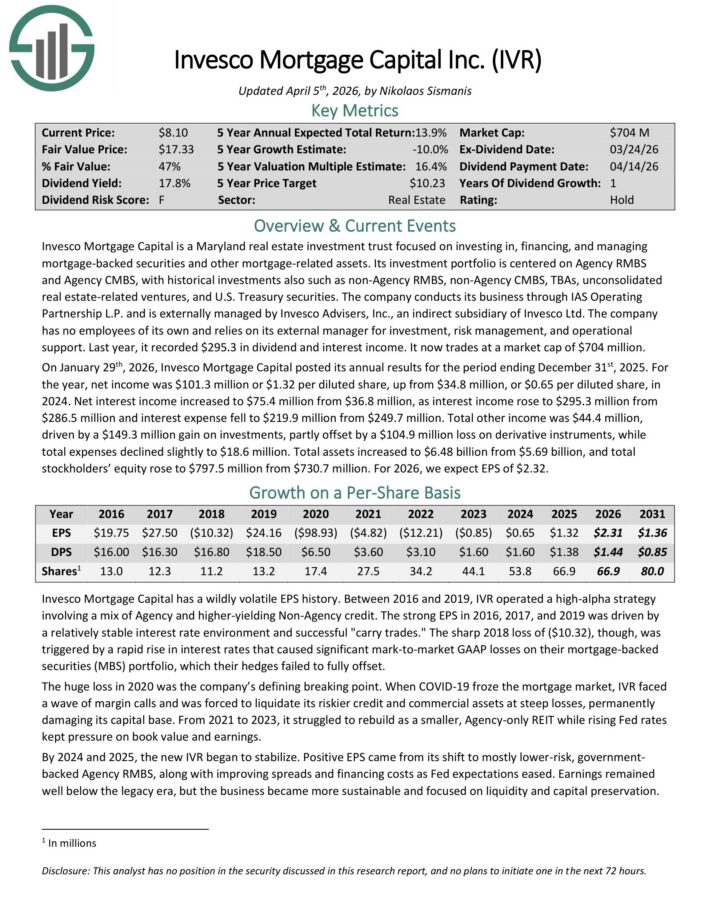

Undervalued Hidden Gem #2: Invesco Mortgage Capital (IVR)

Annual Valuation Return: 18.3%

Dividend Yield: 13.8%

Invesco Mortgage Capital is a Maryland real estate investment trust focused on investing in, financing, and managing mortgage-backed securities and other mortgage-related assets.

Its investment portfolio is centered on Agency RMBS and Agency CMBS, with historical investments also such as non-Agency RMBS, non-Agency CMBS, TBAs, unconsolidated real estate-related ventures, and U.S. Treasury securities.

The company conducts its business through IAS Operating Partnership L.P. and is externally managed by Invesco Advisers, Inc., an indirect subsidiary of Invesco Ltd.

The company has no employees of its own and relies on its external manager for investment, risk management, and operational support. Last year, it recorded $295.3 in dividend and interest income.

On January 29th, 2026, Invesco Mortgage Capital posted its annual results for the period ending December 31st, 2025. For the year, net income was $101.3 million or $1.32 per diluted share, up from $34.8 million, or $0.65 per diluted share, in 2024.

Net interest income increased to $75.4 million from $36.8 million, as interest income rose to $295.3 million from $286.5 million and interest expense fell to $219.9 million from $249.7 million.

Total other income was $44.4 million, driven by a $149.3 million gain on investments, partly offset by a $104.9 million loss on derivative instruments, while total expenses declined slightly to $18.6 million.

Total assets increased to $6.48 billion from $5.69 billion, and total stockholders’ equity rose to $797.5 million from $730.7 million.

For 2026, we expect EPS of $2.32.

Click here to download our most recent Sure Analysis report on IVR (preview of page 1 of 3 shown below):

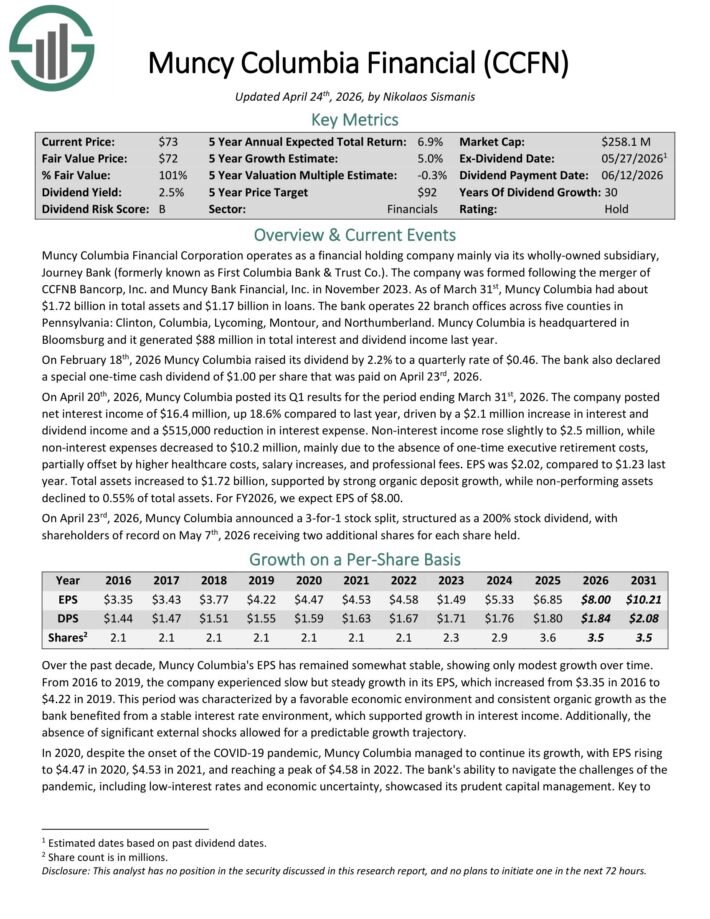

Undervalued Hidden Gem #1: Muncy Columbia Financial (CCFN)

Annual Valuation Return: 22.1%

Dividend Yield: 6.9%

Muncy Columbia Financial Corporation operates as a financial holding company mainly via its wholly-owned subsidiary, Journey Bank (formerly known as First Columbia Bank & Trust Co.).

As of March 31st, Muncy Columbia had about $1.72 billion in total assets and $1.17 billion in loans. The bank operates 22 branch offices across five counties in Pennsylvania: Clinton, Columbia, Lycoming, Montour, and Northumberland.

On February 18th, 2026 Muncy Columbia raised its dividend by 2.2% to a quarterly rate of $0.46. The bank also declared a special one-time cash dividend of $1.00 per share that was paid on April 23rd, 2026.

On April 20th, 2026, Muncy Columbia posted its Q1 results for the period ending March 31st, 2026. The company posted net interest income of $16.4 million, up 18.6% compared to last year, driven by a $2.1 million increase in interest and dividend income and a $515,000 reduction in interest expense.

Non-interest income rose slightly to $2.5 million, while non-interest expenses decreased to $10.2 million, mainly due to the absence of one-time executive retirement costs, partially offset by higher healthcare costs, salary increases, and professional fees.

EPS was $2.02, compared to $1.23 last year. Total assets increased to $1.72 billion, supported by strong organic deposit growth, while non-performing assets declined to 0.55% of total assets. For FY2026, we expect EPS of $8.00.

Click here to download our most recent Sure Analysis report on CCFN (preview of page 1 of 3 shown below):

Final Thoughts & Additional Reading

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

Other Sure Dividend Resources

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}