AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Related Coverage

Stock $36.78 (+7.7%)

EPS YoY +134.1%|Rev YoY +17.6%|Net Margin 28.1%

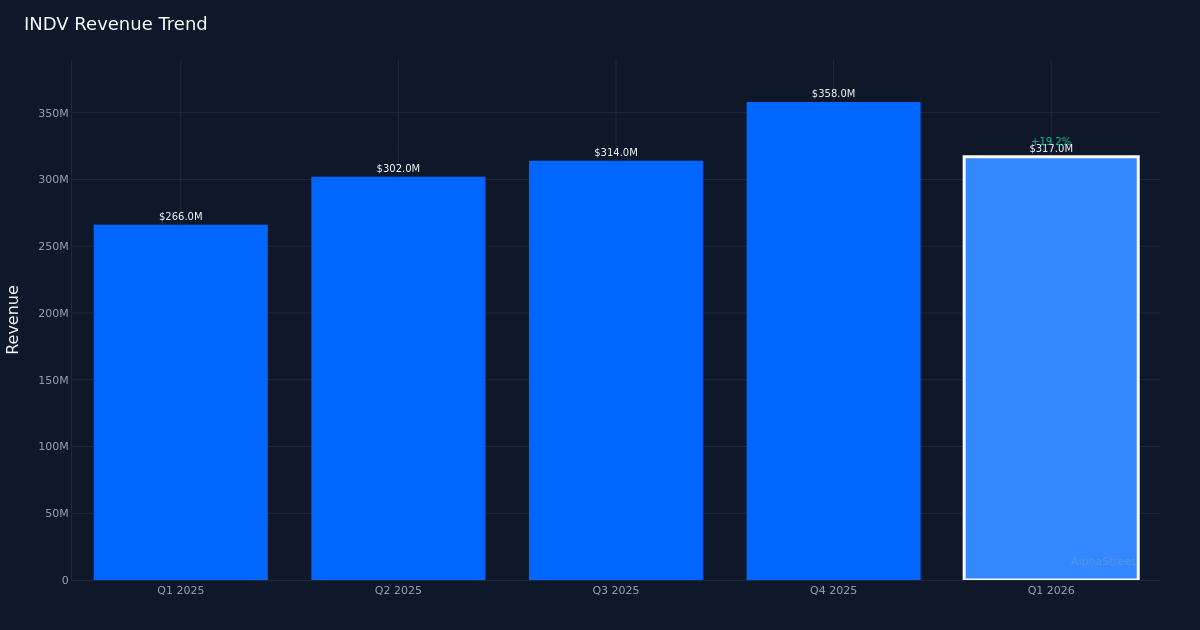

Indivior Pharmaceuticals delivered a blowout first quarter, crushing analyst expectations with adjusted earnings of $0.96 per share versus the $0.67 consensus—a beat of 43.3% that sent shares up 7.7% to $36.78. The specialty pharmaceutical maker reported revenue of $317.0M, up 19.0% year-over-year, driven almost entirely by surging demand for SUBLOCADE, its long-acting buprenorphine injection for opioid use disorder. This wasn’t a story of financial engineering or one-time tailwinds; the quarter showcased genuine operating leverage as the company converted strong topline growth into margin expansion across every layer of the income statement.

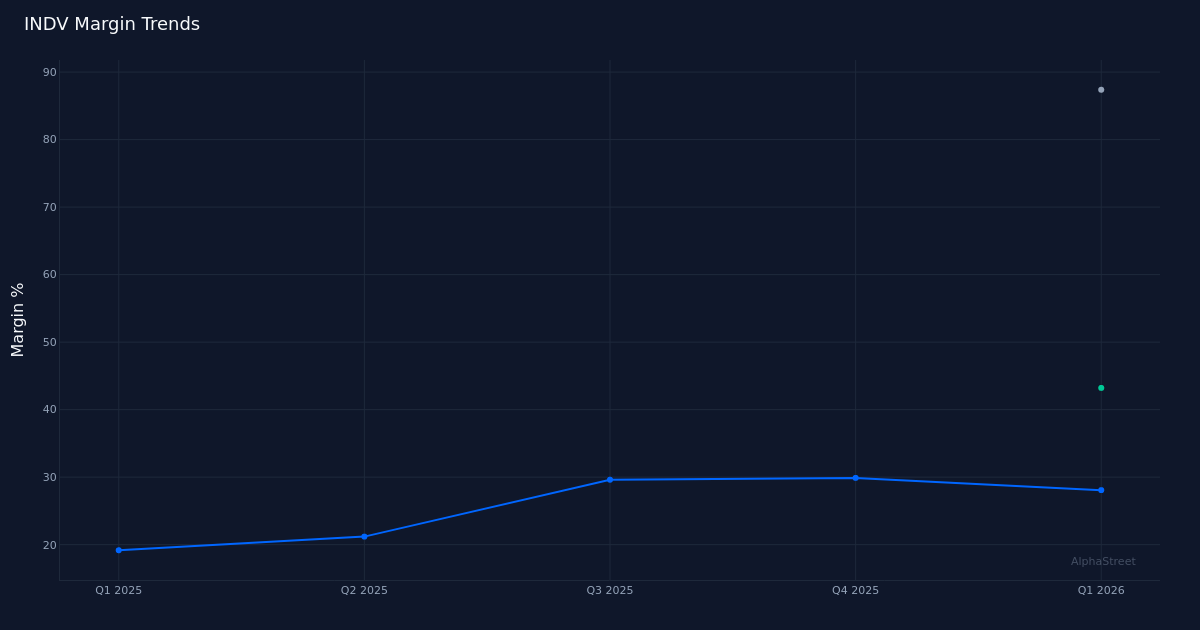

The margin profile tells the story of a business hitting inflection. Net margin expanded to 28.1% in Q1 2026 from in the year-ago period—a jump of that translated into net income of $89.0M versus last year. Operating margin reached while gross margin stood at a pharmaceutical-typical 87.4%, demonstrating that revenue growth is flowing through to the bottom line with minimal incremental cost. Management highlighted this operating leverage explicitly, noting “We delivered adjusted EBITDA of $164 million, up 112% year over year and margin improvement of 23 percentage points.” The 134.1% year-over-year EPS growth from $0.41 to $0.96 significantly outpaced the 19.2% revenue expansion, confirming that scale is driving disproportionate profitability gains as the company leverages its fixed cost base.

Sequential revenue momentum presents a more nuanced picture than the strong year-over-year comparison might suggest. The four-quarter trend shows Q1 2026 revenue of $317.0M following Q4 2025’s $358.0M, Q3 2025’s $314.0M, and Q2 2025’s $302.0M. The sequential decline from Q4 is notable, though not necessarily alarming given typical pharmaceutical seasonality and the fact that Q1 still represents the second-highest quarterly revenue in this dataset. More telling is the EPS trajectory: $0.96 in Q1 2026 represents continued sequential improvement from $0.82, $0.72, and $0.51 in the preceding quarters. The consistent quarterly EPS gains even when revenue dipped sequentially from Q4 reinforces the margin expansion narrative—this business is becoming structurally more profitable as it scales.

SUBLOCADE dominance is both the growth driver and the key risk concentration. The product generated $232.0M in net revenue with 32.0% year-over-year growth, accounting for the vast majority of the company’s $317.0M total revenue. Management disclosed that 500,000 patients have been prescribed SUBLOCADE, and emphasized that growth is coming from both volume and favorable mix: “Importantly and what I would focus you to is the 13% increase in revenue which is driven by the strong dispense unit growth, but also now the favorable outlook that we have in terms of mix.” The company reported 20% dispense unit growth in Q1, which management noted as “We grew total supplicade net revenue 32% year over year to $232 million reflecting strong year over year dispense unit growth of 20%.” The gap between 20% unit growth and 32% revenue growth suggests meaningful pricing or mix benefits that could prove sustainable if the company is successfully shifting patients toward higher-dose or longer-duration formulations.

The tension between Q1 performance and full-year guidance suggests management conservatism or anticipated headwinds. One management comment revealed investor questioning about growth deceleration: “So you did 20% in the first quarter but the guidance for the full year seems to be still around the mid teens level.” This implies full-year dispense unit growth guidance in the mid-teens range despite Q1’s 20% performance, suggesting either normal quarterly variability, tough comparisons later in the year, or deliberate sandbagging. The company’s 100% beat rate over the last quarter (beating 1 of 1 quarters) provides limited historical context, but the magnitude of this quarter’s 43.3% EPS beat could indicate a pattern of conservative guidance setting that creates runway for repeated positive surprises.

The 7.7% stock price gain to $36.78 represents measured enthusiasm rather than euphoric repricing. While the magnitude of the earnings beat and the margin expansion story would typically justify a more dramatic response, investors may be weighing the single-product concentration risk and the implied deceleration in full-year guidance. The positive reaction confirms that the market views these results as credible and the margin gains as sustainable, but the relatively contained move suggests uncertainty about whether the 20% dispense unit growth rate can persist throughout 2026.

The fundamental question facing Indivior is whether SUBLOCADE can maintain its growth trajectory as the patient base scales. With 500,000 patients already prescribed the treatment, the addressable market depth and competitive dynamics will determine if the company can sustain dispense unit growth in the high teens or if normalization toward mid-single-digit growth is inevitable. The favorable mix trends management highlighted suggest opportunities for revenue growth even if patient additions moderate, but that would represent a different—and potentially less valuable—growth profile than pure market expansion.

What to Watch: The key forward metric is whether Q2 dispense unit growth for SUBLOCADE holds near the 20% level or declines toward the mid-teens full-year guidance range, which would clarify if Q1 was an outlier or the start of sustained acceleration. Monitor whether net margin can hold above 25% as the company scales, validating the operating leverage thesis. Any commentary on competitive threats from new long-acting buprenorphine formulations or biosimilars will be critical given the extreme revenue concentration. Finally, watch for updates on the 500,000 prescribed patient base—growth in this metric would provide early indication of market penetration limits or runway for continued expansion.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

(Rookie Reply)")

")

{kind=link}