Updated on May 8th, 2026 by Nathan Parsh

Vital Infrastructure Property Trust (NWHUF), formerly known as NorthWest Healthcare Properties Real Estate Investment Trust, has three appealing investment characteristics:

#1: It is a REIT so it has a favorable tax structure and pays out the majority of its earnings as dividends.Related: List of publicly traded REITs

#2: It is a high-yield stock based on its 6.3% dividend yield.Related: List of 5%+ yielding stocks

#3: It pays dividends monthly instead of quarterly.Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

Vital Infrastructure Property Trust has the trifecta of favorable tax status as a REIT, a high dividend yield, and a monthly dividend makes it appealing to individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about Vital Infrastructure Property Trust.

Business Overview

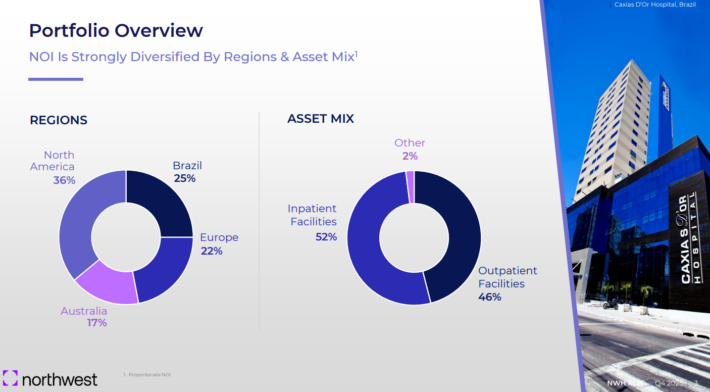

Vital Infrastructure Property Trust is an open-ended real estate investment trust with a portfolio of high-quality international healthcare real estate infrastructure comprised of interests in a portfolio of 133 income-producing properties and 13 million square feet of gross leasable area located throughout major markets in Canada, Brazil, Europe, Australia, and New Zealand.

Source: Investor Presentation

The REIT’s portfolio of medical office buildings, clinics, and hospitals is characterized by long-term indexed leases and stable occupancies. With a fully integrated and aligned senior management team, the REIT leverages over 200 professionals across nine offices in five countries to serve as a long-term real estate partner to leading healthcare operators.

Vital Infrastructure Property Trust has a high occupancy rate of 96.4% and a weighted average lease duration of about 12.3 years. The long lease duration offers great visibility into future cash flows. The REIT is also highly diversified geographically, and, more importantly, it is somewhat protected from high inflation thanks to contractual rent growth year after year.

Vital Infrastructure Property Trust reported its Q4 and full-year results on February 24th, 2026. For the quarter, revenue from investment properties was $78.5 million while net operating income totaled $58.0 million.

Portfolio occupancy was 96.4% with a 12.3-year WALE. Importantly, 95.7% of rental income was subject to inflation linked or fixed-rate increases, supporting strong cash flow visibility. FFO for the quarter was $0.09 per unit and was up from $0.07 in the prior year period. AFFO was also $0.09 per unit.

During the quarter, the trust completed the sale of three properties for total proceeds of $58.3 million, which was used to further strengthen the balance sheet. Debt to gross book value (IFRS) improved to 46.4% at year end, and available liquidity totaled about $339.8 million. Following the previously announced suspension of the DRIP effective after September 2025, no units were issued under the plan in Q4.

For the year, FFO per share was $0.26, which was $0.01 higher than the prior year. We porject FFO per share of $0.32 for 2026.

Growth Prospects

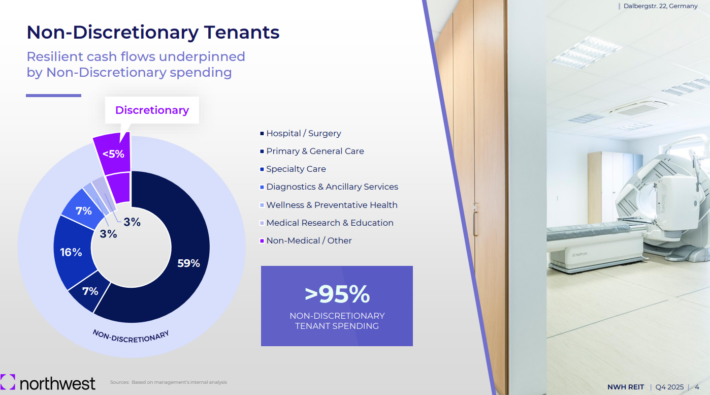

The healthcare real estate market has many attractive characteristics. Firstly, it is one of the largest industries in the world, accounting for more than 10% of global GDP. Approximately $8 trillion is spent on global healthcare annually. Additionally, healthcare spending is growing at an annual rate of ~5% per year for the next 25 years.

As healthcare spending increases, related services will be in higher demand. This benefits the trust given its tenant makeup.

Source: Investor Presentation

Moreover, the healthcare industry benefits from favorable demographics, thanks to a growing and aging global population. As the 65+ group continues to grow, it is the group with the greatest spending power, and global healthcare spending is likely to continue growing at a rapid pace for the next several years.

Furthermore, Vital Infrastructure Property Trust has built a rapidly growing asset management platform. Thanks to this platform, the trust enjoys fast-growing management fees. While management fees somewhat cooled in the latest quarter, they are likely to remain a material growth driver in the upcoming years.

Overall, Vital Infrastructure Property Trust has ample room for future growth thanks to the secular growth of the healthcare industry. On the other hand, high interest rates are likely to take their toll on the trust’s bottom line in the upcoming quarters.

Additionally, the trust’s share count has exploded over the last decade with a growth rate of more than 15% annually over this period. This has greatly impacted FFO results, which have declined 10% annually over the last 10 years and 14.6% over the past five years.

Given the trust’s habit of diluting its share count, we project 0% FFO growth over the next five years.

Dividend & Valuation Analysis

Vital Infrastructure Property Trust is currently offering a dividend yield of 6.3%. It is thus an interesting candidate for income-oriented investors, but the latter should be aware that the dividend may fluctuate significantly over time due to the fluctuations in exchange rates between the Canadian dollar and other foreign currencies, as well as the USD.

Moreover, the REIT typically has an elevated payout ratio of nearly 100%, which significantly reduces the safety margin of the dividend. It should be noted that the projected payout ratio for 2026 is 87%, but a sub-100% payout ratio has not been the norm for the trust.

Regarding valuation, Vital Infrastructure Property Trust is currently trading at only 13.7 times its expected FFO per share for the year. The low valuation has resulted primarily from the expected impact of higher interest expenses on the bottom line and the effect of high inflation on the valuation, as high inflation significantly reduces the present value of future cash flows.

Given the lack of growth expected, we assume a fair price-to-FFO ratio of 10.0 for the stock. Therefore, the current FFO multiple is higher than our assumed fair price-to-FFO ratio. If the stock trades at our fair valuation target in five years, it will result in a 6.1% annual headwind to total returns over this period.

Taking into account the 0.0% annual FFO-per-unit growth, the 6.3% dividend, and a mid-single-digit headwind from multiple contraction, Vital Infrastructure Property Trust could offer a 0.9% average annual total return over the next five years.

This is an extremely low expected return. Given the lack of dividend growth over the years and weak expected total returns, Vital Infrastructure Property Trust receives a sell recommendation.

Final Thoughts

Vital Infrastructure Property Trust has the advantage of operating assets in the global healthcare industry, which enjoys strong and reliable secular growth. Despite its high payout ratio of close to 100%, the stock is offering a high dividend yield of 6.3%. Hence, it is an attractive candidate for the portfolios of income-oriented investors, though total returns are projected to be very low.

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

")

{kind=link}