Updated on May 28th, 2026 by Bob Ciura

There are good reasons for investors to own international stocks, such as diversification. Many companies that operate outside the U.S. have access to geographic markets that could outperform the U.S. in the event of a domestic economic downturn.

Of course, there are risks to purchasing international stocks, such as currency risk.

Still, income investors looking for quality dividend stocks should not always ignore international stocks. Indeed, there are many quality international stocks that have compiled impressive dividend growth histories.

Income investors are likely familiar with the Dividend Aristocrats, which are some of the highest-quality stocks to buy and hold for the long term.

You can download the full Dividend Aristocrats list, along with important metrics like dividend yields and price-to-earnings ratios, by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

The list of Dividend Aristocrats is diversified across multiple sectors, including consumer goods, financials, industrials, and healthcare.

But it is not diversified geographically to include international stocks.

With this in mind, this article will discuss 10 international dividend growth stocks that have raised their dividends for over 25 consecutive years, in their home currencies.

Table of Contents

The table of contents below allows for easy navigation. The stocks are listed by 5-year annual expected returns, in ascending order.

International Dividend Aristocrat #10: Unilever plc (UL)

Consecutive Years Of Dividend Increases: 43

Annual Expected Returns: 10.2%

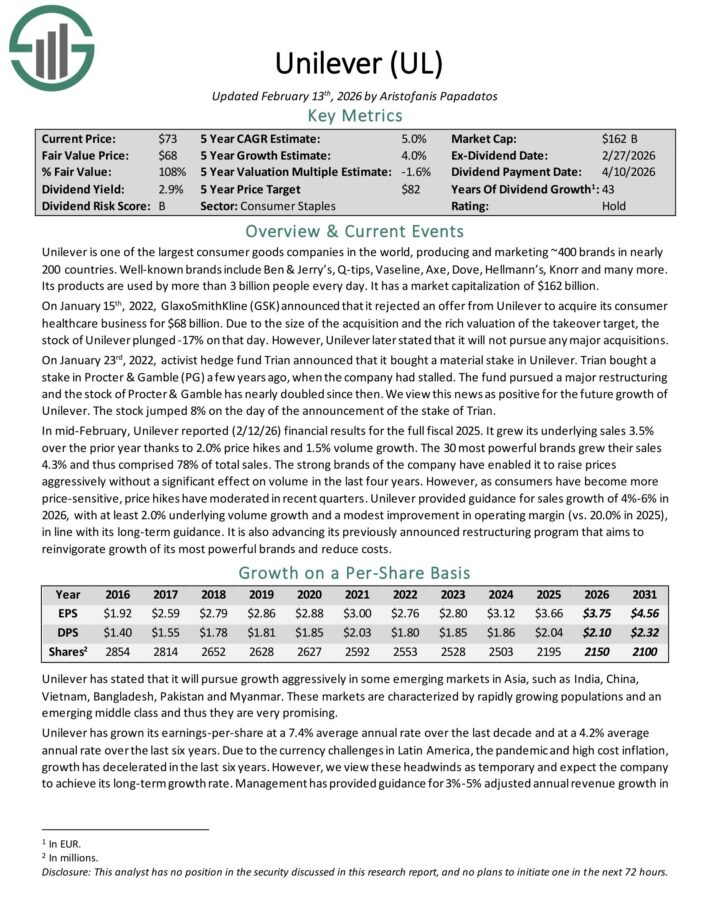

Unilever is one of the largest consumer goods companies in the world, producing and marketing ~400 brands in nearly 200 countries.

Well-known brands include Ben & Jerry’s, Q-tips, Vaseline, Axe, Dove, Hellmann’s, Knorr and many more. Its products are used by more than 3 billion people every day.

In mid-February, Unilever reported (2/12/26) financial results for the full fiscal 2025. It grew its underlying sales 3.5% over the prior year thanks to 2.0% price hikes and 1.5% volume growth.

The 30 most powerful brands grew their sales 4.3% and comprised 78% of total sales. The strong brands of the company have enabled it to raise prices aggressively without a significant effect on volume in the last four years.

However, as consumers have become more price-sensitive, price hikes have moderated in recent quarters.

Unilever provided guidance for sales growth of 4%-6% in 2026, with at least 2.0% underlying volume growth and a modest improvement in operating margin (vs. 20.0% in 2025), in line with its long-term guidance.

Unilever has a significant competitive advantage, namely the strength of its brands. The company generates ~80% of its sales from the #1 or #2 position in its markets.

As a result, Unilever has been able to raise its dividend for 43 consecutive years in Euros.

Click here to download our most recent Sure Analysis report on UL (preview of page 1 of 3 shown below):

International Dividend Aristocrat #9: RenaissanceRe Holdings Ltd. (RNR)

Consecutive Years Of Dividend Increases: 31

Annual Expected Returns: 10.3%

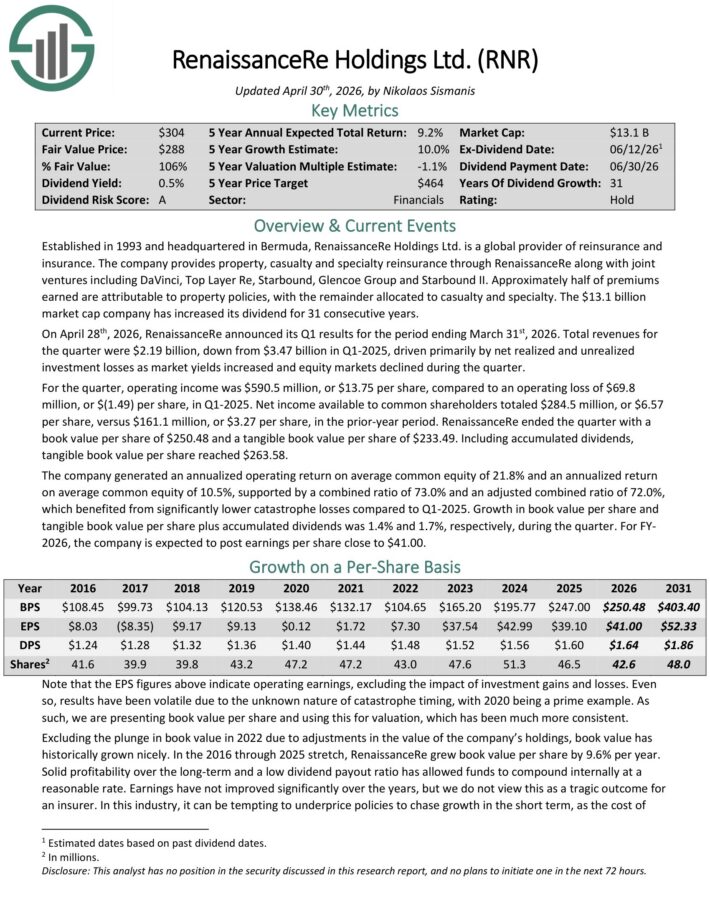

RenaissanceRe Holdings Ltd. is a global provider of reinsurance and insurance.

The company provides property, casualty and specialty reinsurance through RenaissanceRe along with joint ventures including DaVinci, Top Layer Re, Starbound, Glencoe Group and Starbound II.

Approximately half of premiums earned are attributable to property policies, with the remainder allocated to casualty and specialty.

On April 28th, 2026, RenaissanceRe announced its Q1 results for the period ending March 31st, 2026. Total revenue for the quarter was $2.19 billion, down from $3.47 billion in Q1-2025, driven primarily by net realized and unrealized investment losses as market yields increased and equity markets declined during the quarter.

For the quarter, operating income was $590.5 million, or $13.75 per share, compared to an operating loss of $69.8 million, or $(1.49) per share, in Q1-2025.

Net income available to common shareholders totaled $284.5 million, or $6.57 per share, versus $161.1 million, or $3.27 per share, in the prior-year period.

RenaissanceRe ended the quarter with a book value per share of $250.48 and a tangible book value per share of $233.49. Including accumulated dividends, tangible book value per share reached $263.58.

The company generated an annualized operating return on average common equity of 21.8% and an annualized return on average common equity of 10.5%.

Click here to download our most recent Sure Analysis report on RNR (preview of page 1 of 3 shown below):

International Dividend Aristocrat #8: RELX plc (RELX)

Consecutive Years Of Dividend Increases: 27

Annual Expected Returns: 13.4%

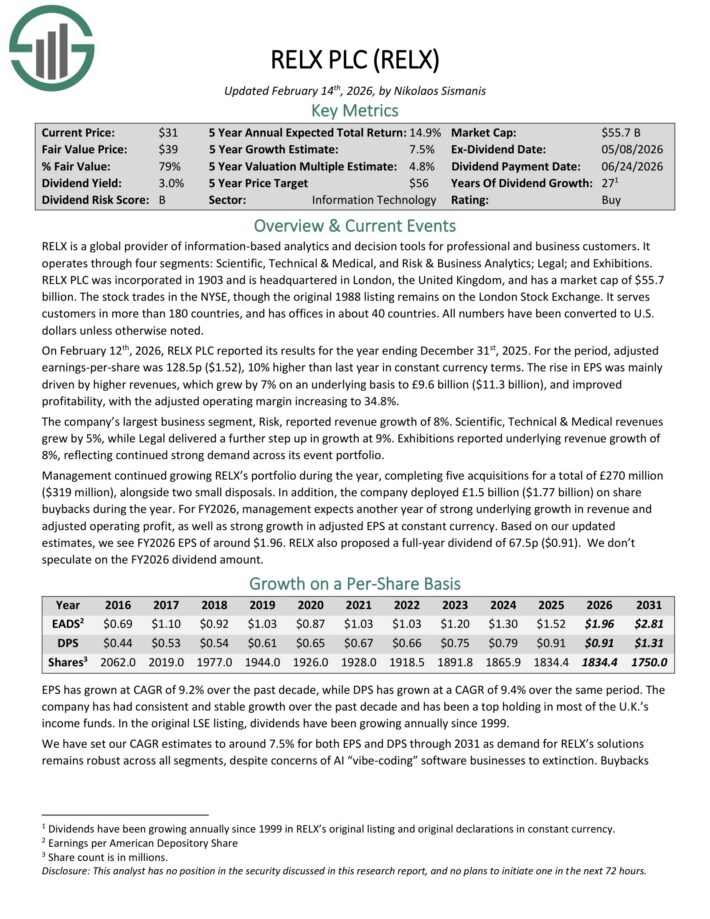

RELX is a global provider of information-based analytics and decision tools for professional and business customers.

It operates through four segments: Scientific, Technical & Medical, and Risk & Business Analytics; Legal; and Exhibitions.

RELX PLC was incorporated in 1903 and is headquartered in London, the United Kingdom. It serves customers in more than 180 countries, and has offices in about 40 countries.

On February 12th, 2026, RELX PLC reported its results for the year ending December 31st, 2025. For the period, adjusted earnings-per-share was 128.5p ($1.52), 10% higher than last year in constant currency terms.

The rise in EPS was mainly driven by higher revenues, which grew by 7% on an underlying basis to £9.6 billion ($11.3 billion), and improved profitability, with the adjusted operating margin increasing to 34.8%.

The company’s largest business segment, Risk, reported revenue growth of 8%. Scientific, Technical & Medical revenue grew by 5%, while Legal delivered a further step up in growth at 9%.

Exhibitions reported underlying revenue growth of 8%, reflecting continued strong demand across its event portfolio.

Click here to download our most recent Sure Analysis report on RELX (preview of page 1 of 3 shown below):

International Dividend Aristocrat #7: Medtronic plc (MDT)

Consecutive Years Of Dividend Increases: 47

Annual Expected Returns: 13.7%

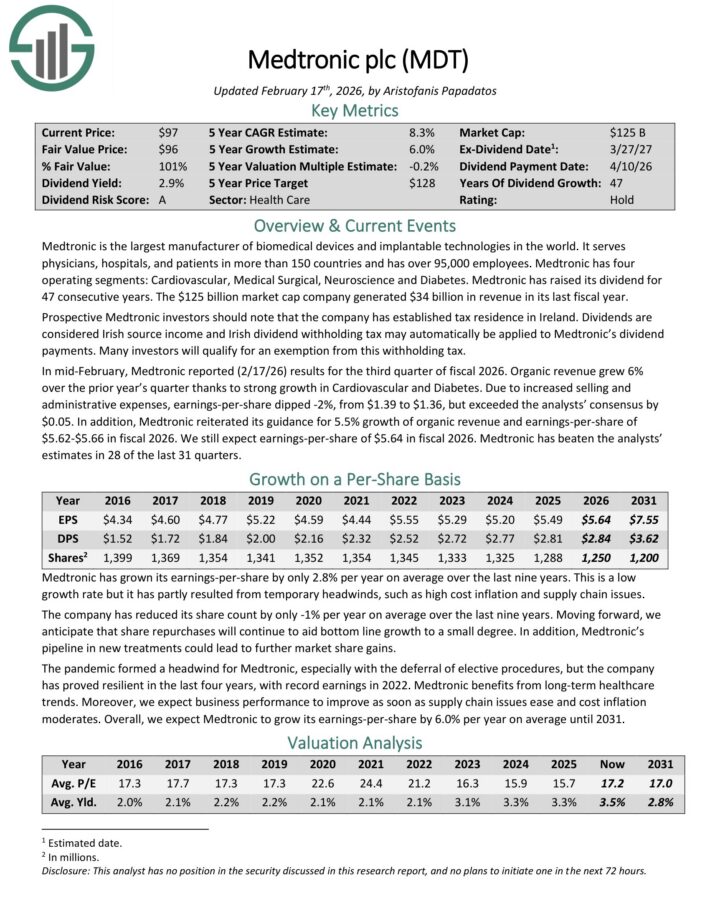

Medtronic is the largest manufacturer of biomedical devices and implantable technologies in the world.

It serves physicians, hospitals, and patients in more than 150 countries and has over 95,000 employees. Medtronic has four operating segments: Cardiovascular, Medical Surgical, Neuroscience and Diabetes.

The company generated $34 billion in revenue in its last fiscal year.

In mid-February, Medtronic reported (2/17/26) results for the third quarter of fiscal 2026. Organic revenue grew 6% over the prior year’s quarter thanks to strong growth in Cardiovascular and Diabetes.

Due to increased selling and administrative expenses, earnings-per-share dipped -2%, from $1.39 to $1.36, but exceeded the analysts’ consensus by $0.05.

In addition, Medtronic reiterated its guidance for 5.5% growth of organic revenue and earnings-per-share of $5.62-$5.66 in fiscal 2026.

Medtronic has raised its dividend for 47 consecutive years. It has grown its dividend by 9.7% per year on average over the last decade and by 5.6% per year on average over the last 5 years.

Click here to download our most recent Sure Analysis report on MDT (preview of page 1 of 3 shown below):

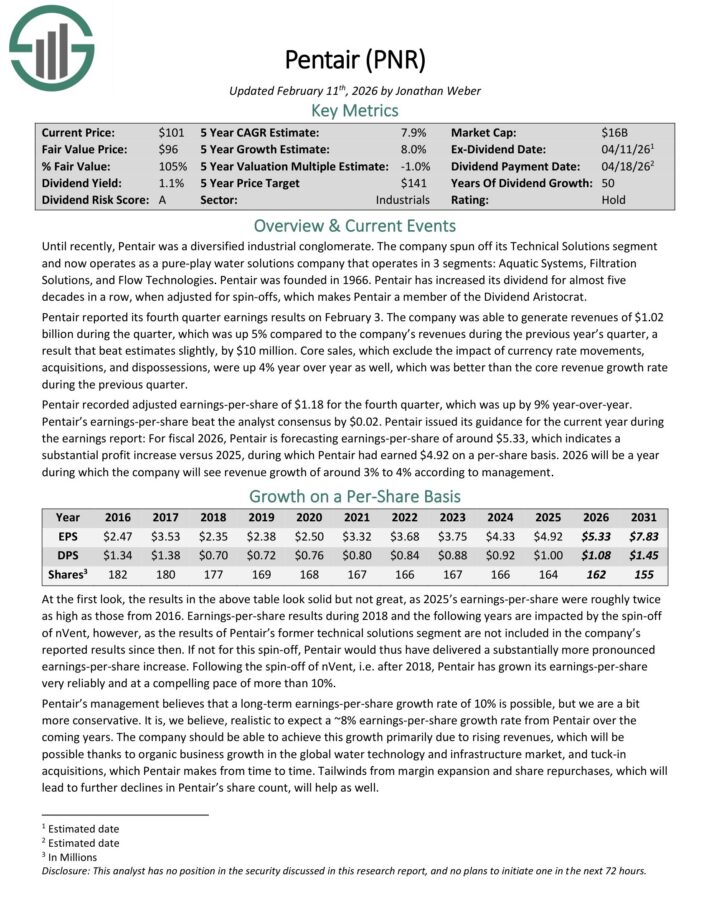

International Dividend Aristocrat #6: Pentair plc (PNR)

Consecutive Years Of Dividend Increases: 50

Annual Expected Returns: 14.3%

Pentair plc is a pure-play water solutions company that operates in 3 segments: Aquatic Systems, Filtration Solutions, and Flow Technologies.

Pentair was founded in 1966. Pentair has increased its dividend for almost five decades in a row, when adjusted for spin-offs, which makes Pentair a member of the Dividend Aristocrat.

Pentair reported its fourth quarter earnings results on February 3. The company generated revenues of $1.02 billion during the quarter, which was up 5% compared to the company’s revenues during the previous year’s quarter, a result that beat estimates slightly, by $10 million.

Core sales, which exclude the impact of currency rate movements, acquisitions, and dispossessions, were up 4% year over year as well, which was better than the core revenue growth rate during the previous quarter.

Pentair recorded adjusted earnings-per-share of $1.18 for the fourth quarter, which was up by 9% year-over-year. Pentair’s earnings-per-share beat the analyst consensus by $0.02.

For fiscal 2026, Pentair is forecasting earnings-per-share of around $5.33, which indicates a substantial profit increase versus 2025, during which Pentair had earned $4.92 on a per-share basis.

Click here to download our most recent Sure Analysis report on PNR (preview of page 1 of 3 shown below):

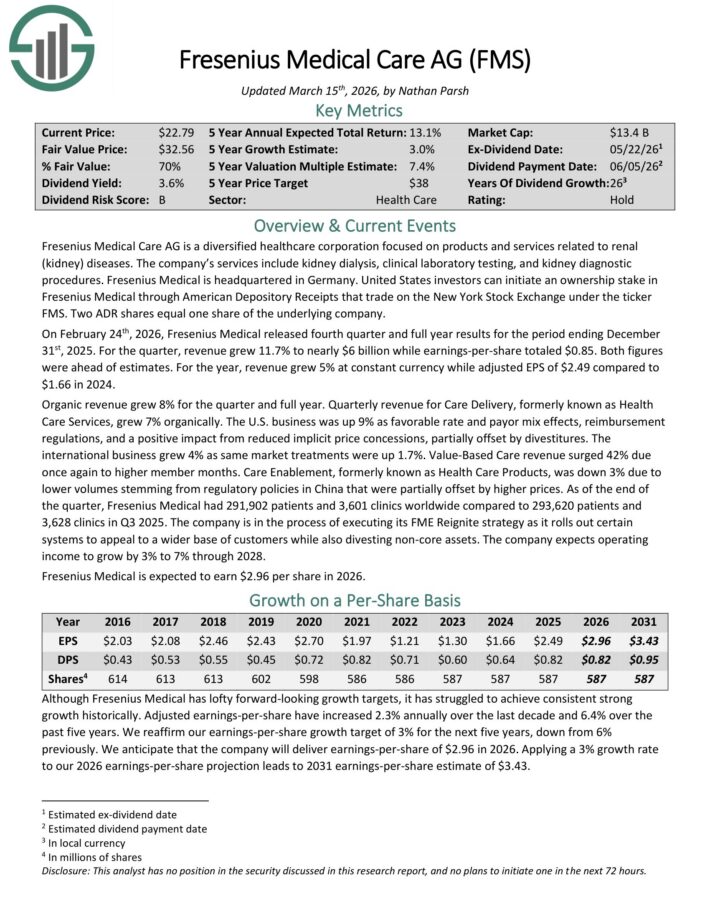

International Dividend Aristocrat #5: Fresenius Medical Care AG (FMS)

Consecutive Years Of Dividend Increases: 26

Annual Expected Returns: 14.4%

Fresenius Medical Care AG is a diversified healthcare corporation focused on products and services related to renal diseases.

The company’s services include kidney dialysis, clinical laboratory testing, and kidney diagnostic procedures. Fresenius Medical is headquartered in Germany.

On February 24th, 2026, Fresenius Medical released fourth quarter and full year results. For the quarter, revenue grew 11.7% to nearly $6 billion while earnings-per-share totaled $0.85. Both figures were ahead of estimates.

For the year, revenue grew 5% at constant currency while adjusted EPS of $2.49 compared to $1.66 in 2024. Organic revenue grew 8% for the quarter and full year.

Quarterly revenue for Care Delivery, formerly known as Health Care Services, grew 7% organically. The U.S. business was up 9% as favorable rate and payor mix effects, reimbursement regulations, and a positive impact from reduced implicit price concessions, partially offset by divestitures.

The international business grew 4% as same market treatments were up 1.7%. Value-Based Care revenue surged 42% due once again to higher member months.

As of the end of the quarter, Fresenius Medical had 291,902 patients and 3,601 clinics worldwide compared to 293,620 patients and 3,628 clinics in Q3 2025.

The company expects operating income to grow by 3% to 7% through 2028. Fresenius Medical is expected to earn $2.96 per share in 2026.

Click here to download our most recent Sure Analysis report on FMS (preview of page 1 of 3 shown below):

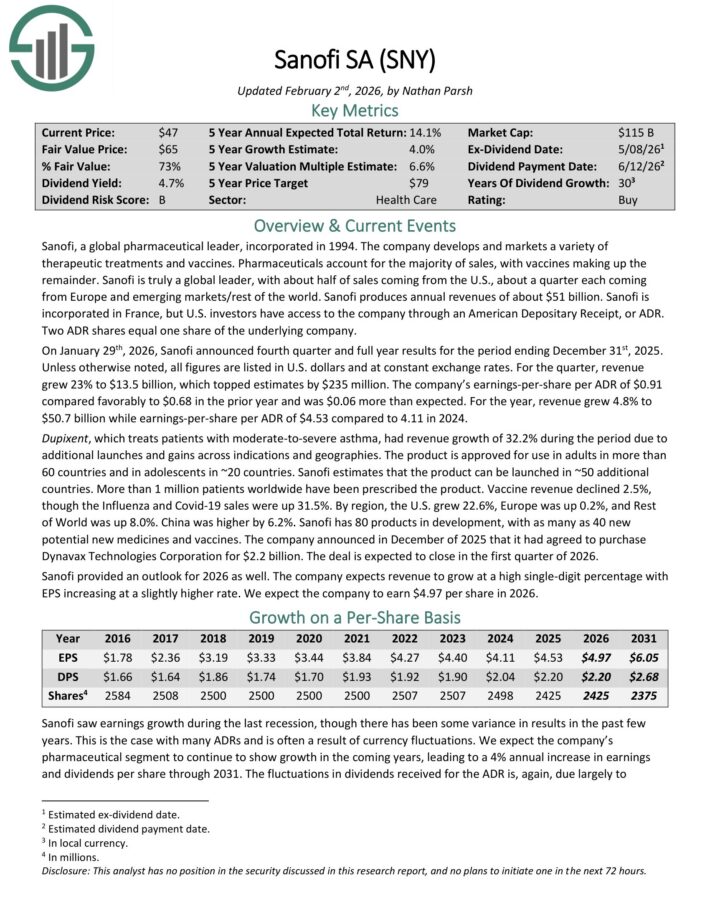

International Dividend Aristocrat #4: Sanofi (SNY)

Consecutive Years Of Dividend Increases: 31

Annual Expected Returns: 15.9%

Sanofi is a global pharmaceutical leader that develops a variety of therapeutic treatments and vaccines.

Pharmaceuticals account for the majority of sales, with vaccines making up the remainder. Sanofi produces annual revenues of about $51 billion.

Sanofi is incorporated in France, but U.S. investors have access to the company through an American Depositary Receipt, or ADR. Two ADR shares equal one share of the underlying company.

On January 29th, 2026, Sanofi announced fourth quarter and full year results. Unless otherwise noted, all figures are listed in U.S. dollars and at constant exchange rates.

For the quarter, revenue grew 23% to $13.5 billion, which topped estimates by $235 million. The company’s earnings-per-share per ADR of $0.91 compared favorably to $0.68 in the prior year and was $0.06 more than expected.

For the year, revenue grew 4.8% to $50.7 billion while earnings-per-share per ADR of $4.53 compared to 4.11 in 2024.

Dupixent, which treats patients with moderate-to-severe asthma, had revenue growth of 32.2% during the period due to additional launches and gains across indications and geographies.

Sanofi has 80 products in development, with as many as 40 new potential new medicines and vaccines.

Sanofi provided an outlook for 2026 as well. The company expects revenue to grow at a high single-digit percentage with EPS increasing at a slightly higher rate.

Click here to download our most recent Sure Analysis report on SNY (preview of page 1 of 3 shown below):

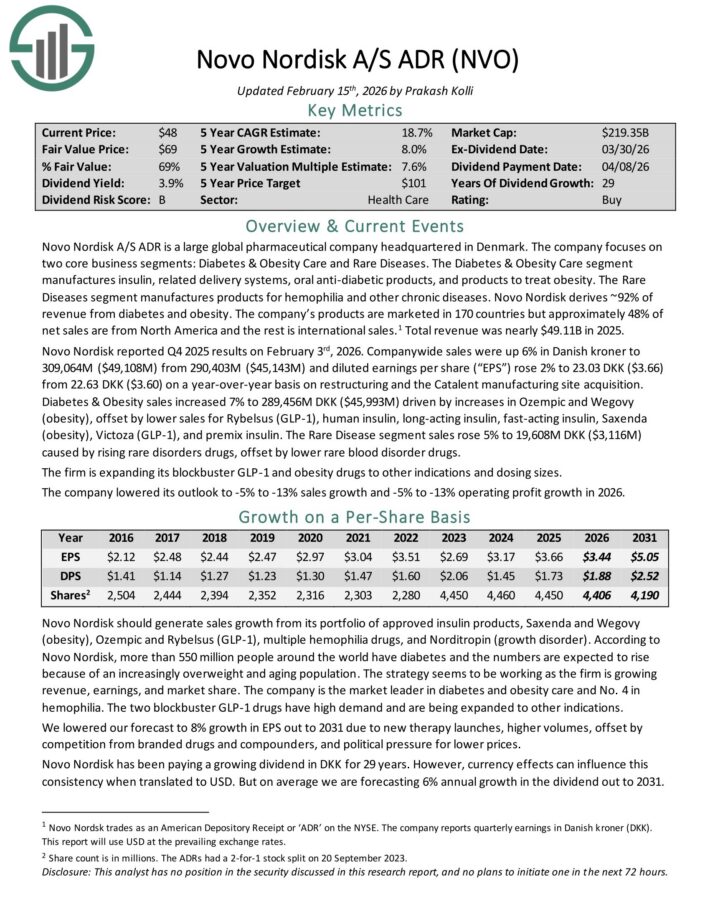

International Dividend Aristocrat #3: Novo Nordisk (NVO)

Consecutive Years Of Dividend Increases: 29

Annual Expected Returns: 18.0%

Novo Nordisk A/S ADR is a large global pharmaceutical company headquartered in Denmark. The company focuses on two core business segments: Diabetes & Obesity Care and Rare Diseases.

The Diabetes & Obesity Care segment manufactures insulin, related delivery systems, oral anti-diabetic products, and products to treat obesity.

The Rare Diseases segment manufactures products for hemophilia and other chronic diseases. Novo Nordisk derives ~92% of revenue from diabetes and obesity.

The company’s products are marketed in 170 countries but approximately 48% of net sales are from North America and the rest is international sales.1 Total revenue was nearly $49.11B in 2025.

Novo Nordisk reported Q4 2025 results on February 3rd, 2026. Company-wide sales were up 6% in Danish kroner and diluted earnings per share rose 2% to 23.03 DKK ($3.66) from 22.63 DKK ($3.60) on a year-over-year basis.

Diabetes & Obesity sales increased 7% to 289,456M DKK ($45,993M) driven by increases in Ozempic and Wegovy (obesity), offset by lower sales for Rybelsus (GLP-1), human insulin, long-acting insulin, fast-acting insulin, Saxenda (obesity), Victoza (GLP-1), and premix insulin.

The Rare Disease segment sales rose 5% to 19,608M DKK ($3,116M) caused by rising rare disorders drugs, offset by lower rare blood disorder drugs.

Click here to download our most recent Sure Analysis report on NVO (preview of page 1 of 3 shown below):

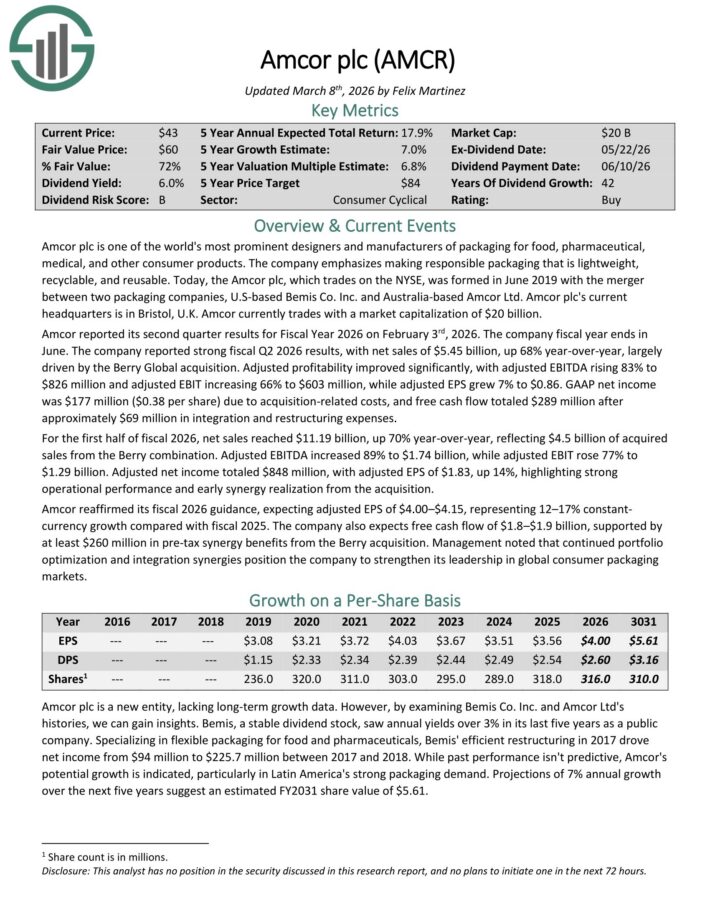

International Dividend Aristocrat #2: Amcor plc (AMCR)

Consecutive Years Of Dividend Increases: 42

Annual Expected Returns: 20.0%

Amcor plc is one of the world’s most prominent designers and manufacturers of packaging for food, pharmaceutical, medical, and other consumer products.

Amcor reported its second quarter results for Fiscal Year 2026 on February 3rd, 2026. The company reported strong fiscal Q2 2026 results, with net sales of $5.45 billion, up 68% year-over-year, largely driven by the Berry Global acquisition.

Adjusted profitability improved significantly, with adjusted EBITDA rising 83% to $826 million and adjusted EBIT increasing 66% to $603 million, while adjusted EPS grew 7% to $0.86.

GAAP net income was $177 million ($0.38 per share) due to acquisition-related costs, and free cash flow totaled $289 million after approximately $69 million in integration and restructuring expenses.

For the first half of fiscal 2026, net sales reached $11.19 billion, up 70% year-over-year, reflecting $4.5 billion of acquired sales from the Berry combination.

Amcor reaffirmed its fiscal 2026 guidance, expecting adjusted EPS of $4.00–$4.15, representing 12–17% constant currency growth compared with fiscal 2025.

The company also expects free cash flow of $1.8–$1.9 billion, supported by at least $260 million in pre-tax synergy benefits from the Berry acquisition.

Click here to download our most recent Sure Analysis report on AMCR (preview of page 1 of 3 shown below):

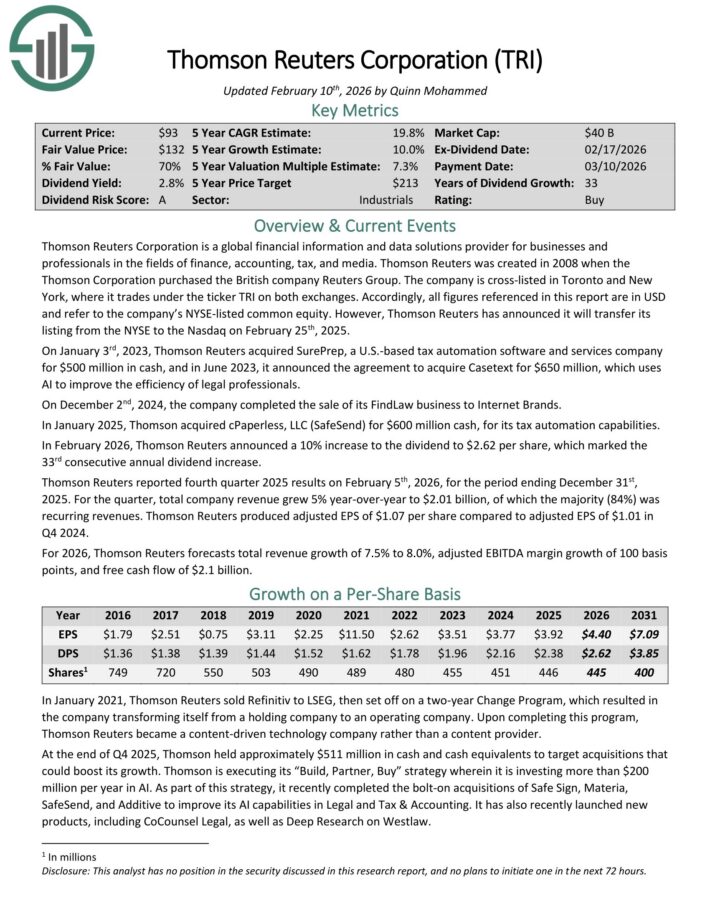

International Dividend Aristocrat #1: Thomson-Reuters (TRI)

Consecutive Years Of Dividend Increases: 33

Annual Expected Returns: 25.0%

Thomson Reuters Corporation is a global financial information and data solutions provider for businesses and professionals in the fields of finance, accounting, tax, and media.

In January 2025, Thomson acquired cPaperless, LLC (SafeSend) for $600 million cash, for its tax automation capabilities.

In February 2026, Thomson Reuters announced a 10% increase to the dividend to $2.62 per share, which marked the 33rd consecutive annual dividend increase.

Thomson Reuters reported fourth quarter 2025 results on February 5th, 2026. For the quarter, total company revenue grew 5% year-over-year to $2.01 billion, of which the majority (84%) was recurring revenues.

Thomson Reuters produced adjusted EPS of $1.07 per share compared to adjusted EPS of $1.01 in Q4 2024.

For 2026, Thomson Reuters forecasts total revenue growth of 7.5% to 8.0%, adjusted EBITDA margin growth of 100 basis points, and free cash flow of $2.1 billion.

Click here to download our most recent Sure Analysis report on TRI (preview of page 1 of 3 shown below):

Additional Reading

The following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

Dividend Champions: 25+ years of rising dividends

Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

")

")

{kind=link}