Updated on April 23rd, 2026 by Josh Arnold

Real Estate Investment Trusts, or REITs, are divided into different sub-sectors depending on the operations of the underlying businesses.

Industrial REITs stand out because of their focus on single-tenant properties. While this poses a higher vacancy risk than multi-tenant properties, it can also lead to mispriced assets and attractive buying opportunities.

Dream Industrial REIT (DREUF) is an industrial REIT that may not be well-known to investors because it operates primarily in Canada.

However, Dream Industrial REIT has a high dividend yield of more than 5%, which is about four times the average dividend yield in the S&P 500. The stock pays its dividends monthly.

You can download our full list of all 119 monthly dividend stocks (along with relevant financial metrics like dividend yields and payout ratios), which you can access below:

For retirees and other investors who rely on dividend payments, monthly dividends are far superior to the traditional quarterly payment schedule.

Dream Industrial REIT’s high dividend yield and monthly dividend payments are characteristics that appeal to income investors.

This article will analyze the investment prospects of Dream Industrial in detail.

Business Overview

Dream Industrial is a Canadian-based, industrial-focused Real Estate Investment Trust that operates in two broad divisions:

Multi-Tenant Properties

Single-Tenant Properties

This diversification is outstanding among industrial REITs and many other types of REITs with single-tenant properties.

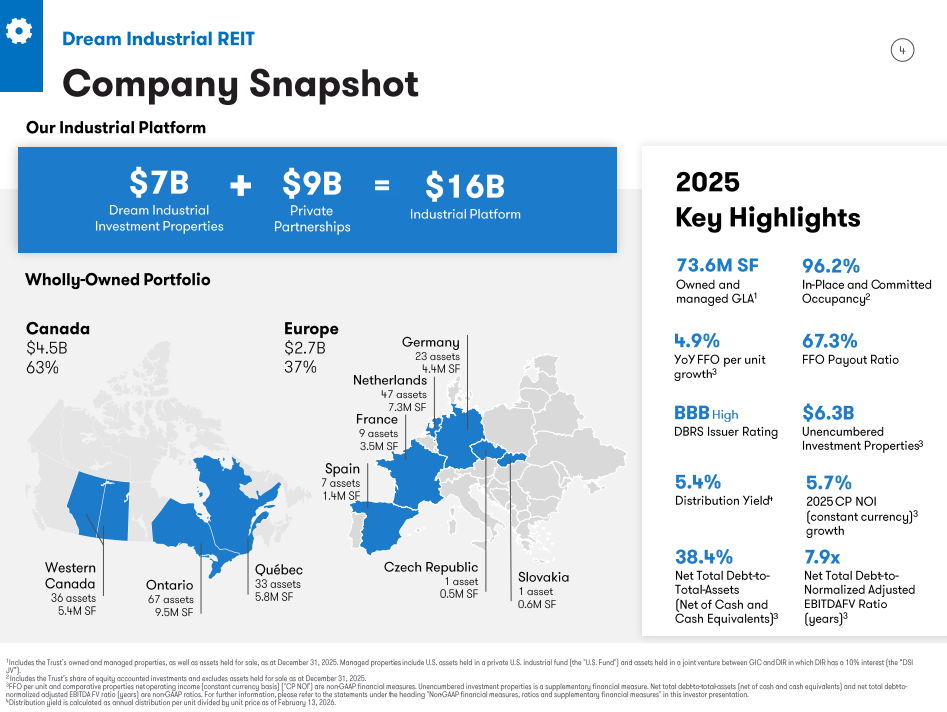

The trust owns and operates a portfolio of more than 400 geographically diversified light industrial properties, which make up ~74 million square feet of gross leasable area predominantly across Canada, with some operations in the United States.

Most of the portfolio’s gross leasable area is in multi-tenant buildings, with the remaining in single-tenant buildings.

Source: Investor Presentation

Dream Industrial is in the process of diversifying its asset mix, but it remains focused on Canada and on industrial properties, with the heaviest concentration still in Ontario.

Dream Industrial posted fourth quarter and full-year earnings on February 17th, 2026, and results were better than 2024. Net rental income was up 8.3% year-over-year to $281.1 million, which was attributable to higher comparative properties growth, and contributions from completed development projects. Comparable property net operating income on a constant currency basis was up nearly 6% to $296 million, which was supported by strong leasing momentum and higher rental rates in both Canada and Europe.

The trust ended the year with occupancy of 96.2%, and transacted 7.4 million square feet of leases during the year. During the year, Dream Industrial agreed to sell 3.6 million square feet for $588 million, as well as some new acquisitions in Germany. Funds-from-operations were $224 million, or 76 cents per share on the US-traded units. For this year, we’re expecting FFO-per-share of 80 cents, noting there is currency fluctuation risk for US investors.

Growth Prospects

Dream Industrial REIT’s growth depends on the ability to issue new units or issue debt and invest the proceeds of these capital markets transactions into high-quality industrial real estate assets. The trust is also highly dependent on its ability to source new tenants and renew existing leases in its property portfolio at favorable rates.

With that in mind, investors should note that the trust has had a very strong level of occupancy since its initial public offering.

Its occupancy rate has improved in recent years as the trust continues to take advantage of strong fundamentals in industrial properties. Dream Industrial is focusing on its four long-term growth drivers, in addition to future acquisitions that will build and improve its total portfolio. This includes moving swiftly into Western Europe to diversify away from Canada somewhat.

Going forward, we expect 1.0% annual FFO-per-share growth each year. For its part, Dream Industrial sees a positive growth outlook for itself.

Source: Investor Presentation

The trust is heavily concentrated in Ontario and Quebec, areas where it has experienced great success in renewal spreads in recent years. It also has contractual rent increases, a natural tailwind to rental growth.

Occupancy remains high and is still increasing, and Dream Industrial is constantly managing its renewals to capture higher rents as quickly as possible. The trust sees powerful, long-term tailwinds in that space, so Dream Industrial is focusing on e-commerce properties.

The trust is positioning itself to be a premier provider of space its tenants need to do business in the coming years. Acquisitions are a major component of the company’s growth plan.

Overall, we see Dream Industrial’s growth outlook as favorable and supportive of long-term funds-from-operations growth. Finally, Dream Industrial has begun to expand in Europe, with an initial portfolio concentrated primarily in the Netherlands, and also in Germany.

Europe is responsible for about 20% of world GDP and holds more than 740 million people. With Dream Industrial just beginning to scratch the surface of possibilities in Europe, the trust has the potential to see a long runway for growth in this region.

Dividend Analysis

Dream pays a current monthly distribution of $0.0583 per share in Canadian dollars. That works out to $0.70 per share annually in Canadian currency. In U.S. dollars, Dream has an annualized dividend payout of $0.51 per share, which represents a current yield of 5.1%.

Note: As a Canadian stock, a 15% dividend tax will be imposed on US investors investing in the company outside of a retirement account. See our guide on Canadian taxes for US investors here.

In fact, the distribution has never been cut in the trust’s relatively short operating history, but it has also not been increased for nine years. The stagnant payout may be discouraging for investors looking for dividend growth.

The dividend payout is covered, as 2025 saw FFO-per-share of $0.76. From a dividend coverage perspective, Dream Industrial is in pretty good shape. For 2026, we are currently estimating a dividend payout ratio of roughly 64%.

Its strong balance sheet is another factor helping to secure Dream Industrial’s dividend payout. Dream Industrial has an investment-grade credit rating of BBB and a manageable level of debt.

Finally, income investors should consider the payout ratio when assessing a dividend’s sustainability. Payout ratios for REITs are always very high because they are required to distribute nearly all of their earnings.

At 64% expected for 2026, Dream Industrial’s payout ratio appears healthy, and we view the dividend payout as safe. Distribution growth may prove to be elusive, but we do not see a cut anytime soon, particularly as earnings have grown with a flat distribution.

Final Thoughts

Dream Industrial REIT’s high dividend yield and monthly dividend payments are two reasons why the company will stand out to income investors.

The stock yields 5.1%, which is relatively appealing. Investors may find the high yield an attractive income possibility.

The REIT has strong fundamentals and a very high occupancy rate. The trust also has the potential for future growth, especially in Europe. Dream Industrial could interest those investors looking for high income and growth potential. We note growth in earnings, and therefore the potential for dividend increases, is quite modest.

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}