Updated on June 30th, 2026 by Bob Ciura

Mortgage Real Estate Investment Trusts (i.e., “REITs”) – often referred to as “mREITs” – can provide a very attractive source of income for investors.

This is because they invest in mortgages that are typically backed by hard assets (commercial and/or residential real estate) with fairly conservative loan-to-value ratios.

Mortgage REITs finance these portfolios with a mixture of equity (that they raise by selling shares to investors) and debt that they generally raise at an interest cost that is meaningfully lower than the interest rates they can command on their real estate mortgage investments.

The result is significant and stable cash flow for the mREIT.

You can download your free 200+ REIT list (along with important financial metrics like dividend yields and payout ratios) by clicking on the link below:

Moreover, as REITs they are exempt from having to pay corporate taxes on their net interest income and are required to pay out at least 90% of their taxable income to shareholders via dividends.

This generally means that mREIT shareholders earn very high dividend yields, making mREIT shares an exceptional source of passive income.

Of course, due to their significant amount of leverage, mortgage REITs come with risks that occasionally lead to dividend cuts.

As a result, investors need to be prudent when selecting which mREITs to invest in.

This article will list the 6 highest yielding mortgage REITs in the Sure Analysis Research Database.

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

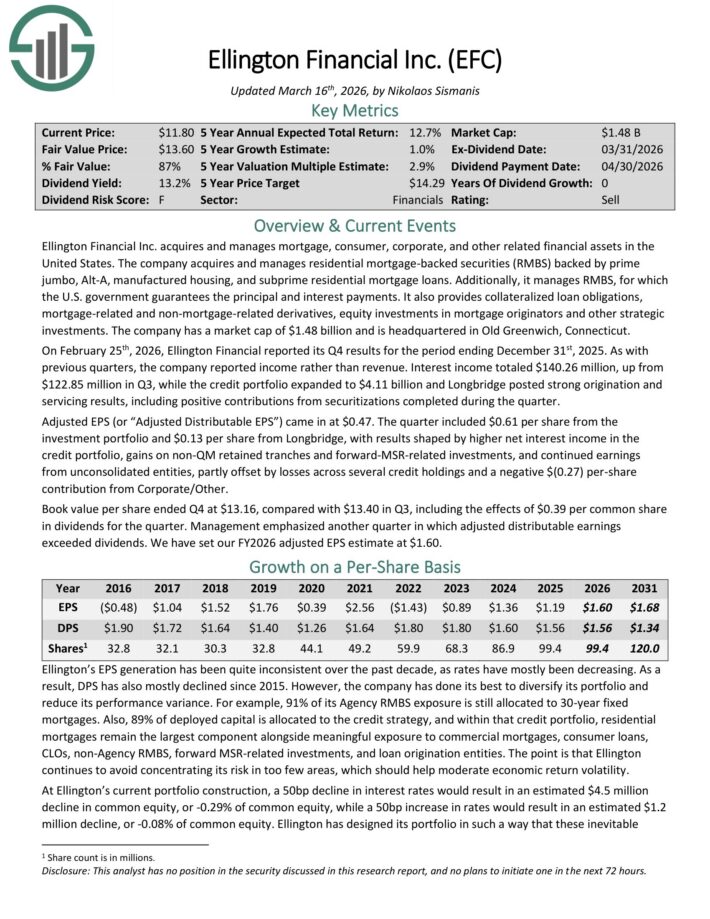

#6: Ellington Financial (EFC)

Ellington Financial Inc. acquires and manages mortgage, consumer, corporate, and other related financial assets in the United States.

The company acquires and manages residential mortgage–backed securities (RMBS) backed by prime jumbo, Alt–A, manufactured housing, and subprime residential mortgage loans.

Additionally, it manages RMBS, for which the U.S. government guarantees the principal and interest payments. It also provides collateralized loan obligations, mortgage–related and non–mortgage–related derivatives, equity investments in mortgage originators and other strategic investments.

On February 25th, 2026, Ellington Financial reported its Q4 results. Interest income totaled $140.26 million, up from$122.85 million in Q3, while the credit portfolio expanded to $4.11 billion and Longbridge posted strong origination and servicing results, including positive contributions from securitizations completed during the quarter.

Adjusted EPS came in at $0.47. The quarter included $0.61 per share from the investment portfolio and $0.13 per share from Longbridge, with results shaped by higher net interest income in the credit portfolio, gains on non-QM retained tranches and forward-MSR-related investments, and continued earnings from unconsolidated entities.

Click here to download our most recent Sure Analysis report on Ellington Financial (EFC) (preview of page 1 of 3 shown below):

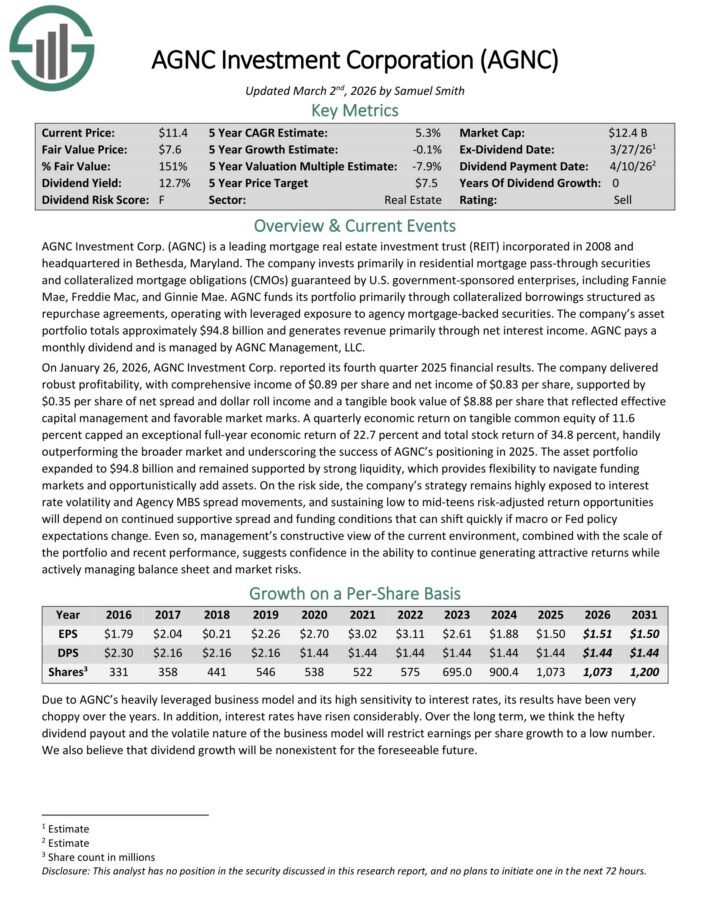

#5: AGNC Investment Corporation (AGNC)

American Capital Agency Corp is a mortgage real estate investment trust that invests primarily in agency mortgage–backed securities (or MBS) on a leveraged basis.

The firm’s asset portfolio is comprised of residential mortgage pass–through securities, collateralized mortgage obligations (or CMO), and non–agency MBS. Many of these are guaranteed by government–sponsored enterprises.

On January 26, 2026, AGNC Investment Corp. reported its fourth quarter 2025 financial results. The company delivered robust profitability, with comprehensive income of $0.89 per share and net income of $0.83 per share.

Results were supported by $0.35 per share of net spread and dollar roll income and a tangible book value of $8.88 per share that reflected effective capital management and favorable market marks.

A quarterly economic return on tangible common equity of 11.6 percent capped an exceptional full-year economic return of 22.7 percent and total stock return of 34.8 percent, handily outperforming the broader market and underscoring the success of AGNC’s positioning in 2025.

The asset portfolio expanded to $94.8 billion and remained supported by strong liquidity, which provides flexibility to navigate funding markets and opportunistically add assets.

Click here to download our most recent Sure Analysis report on AGNC Investment Corp (AGNC) (preview of page 1 of 3 shown below):

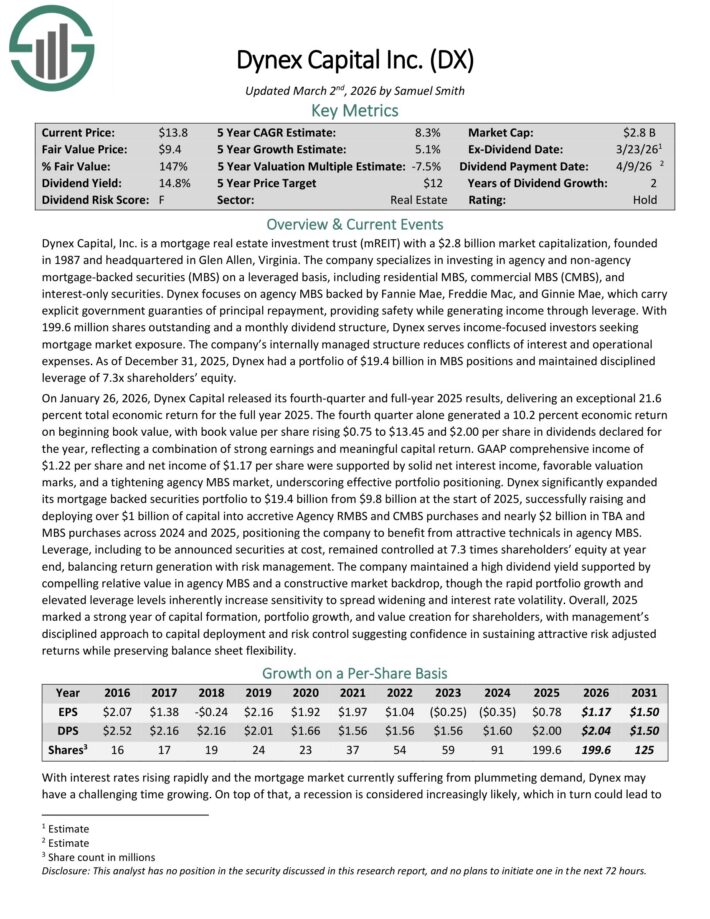

#4: Dynex Capital (DX)

Dynex Capital invests in mortgage–backed securities (MBS) on a leveraged basis in the United States. It invests in agency and non–agency MBS consisting of residential MBS, commercial MBS (CMBS), and CMBS interest–only securities.

On January 26, 2026, Dynex Capital released its fourth-quarter and full-year 2025 results, delivering an exceptional 21.6% total economic return for the full year 2025.

The fourth quarter alone generated a 10.2% economic return on beginning book value, with book value per share rising $0.75 to $13.45 and $2.00 per share in dividends declared for the year, reflecting a combination of strong earnings and meaningful capital return.

GAAP comprehensive income of $1.22 per share and net income of $1.17 per share were supported by solid net interest income, favorable valuation marks, and a tightening agency MBS market, underscoring effective portfolio positioning.

Click here to download our most recent Sure Analysis report on DX (preview of page 1 of 3 shown below):

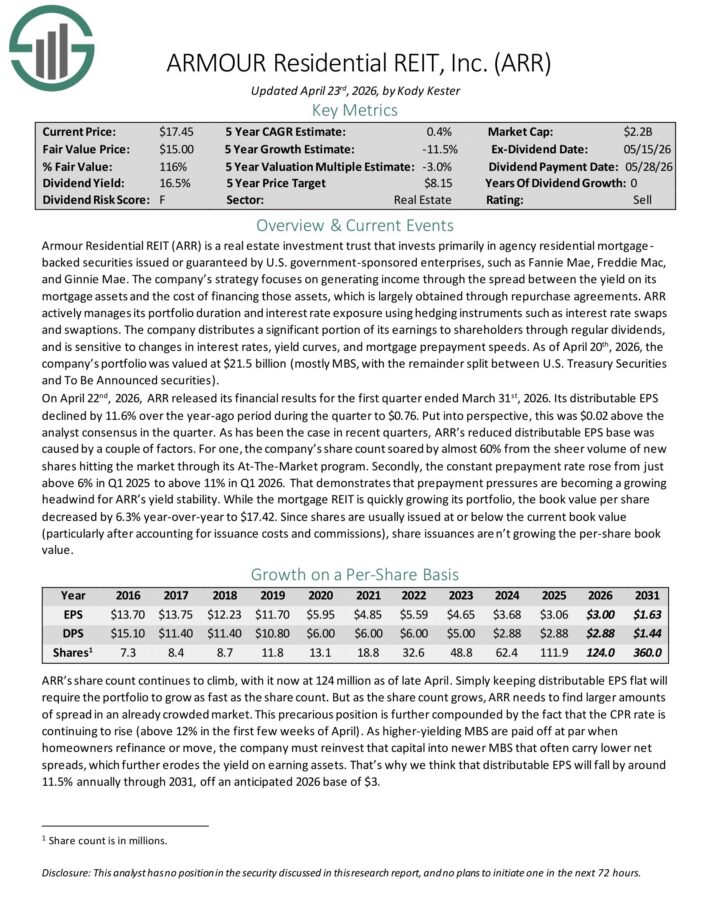

#3: ARMOUR Residential REIT (ARR)

ARMOUR Residential invests in residential mortgage-backed securities that include U.S. Government-sponsored entities (GSE) such as Fannie Mae and Freddie Mac.

It also includes Ginnie Mae, the Government National Mortgage Administration’s issued or guaranteed securities backed by fixed-rate, hybrid adjustable-rate, and adjustable-rate home loans.

Unsecured notes and bonds issued by the GSE and the US Treasury, money market instruments, and non-GSE or government agency-backed securities are examples of other types of investments.

On April 22nd, 2026, ARR released its financial results for the first quarter ended March 31st, 2026. Its distributable EPS declined by 11.6% over the year-ago period during the quarter to $0.76. This was $0.02 above the analyst consensus in the quarter.

The reduced distributable EPS base was caused by a couple of factors. For one, the company’s share count soared by almost 60% from the sheer volume of new shares hitting the market through its At-The-Market program.

Secondly, the constant prepayment rate rose from just above 6% in Q1 2025 to above 11% in Q1 2026.

Book value per share decreased by 6.3% year-over-year to $17.42.

Click here to download our most recent Sure Analysis report on ARMOUR Residential REIT Inc (ARR) (preview of page 1 of 3 shown below):

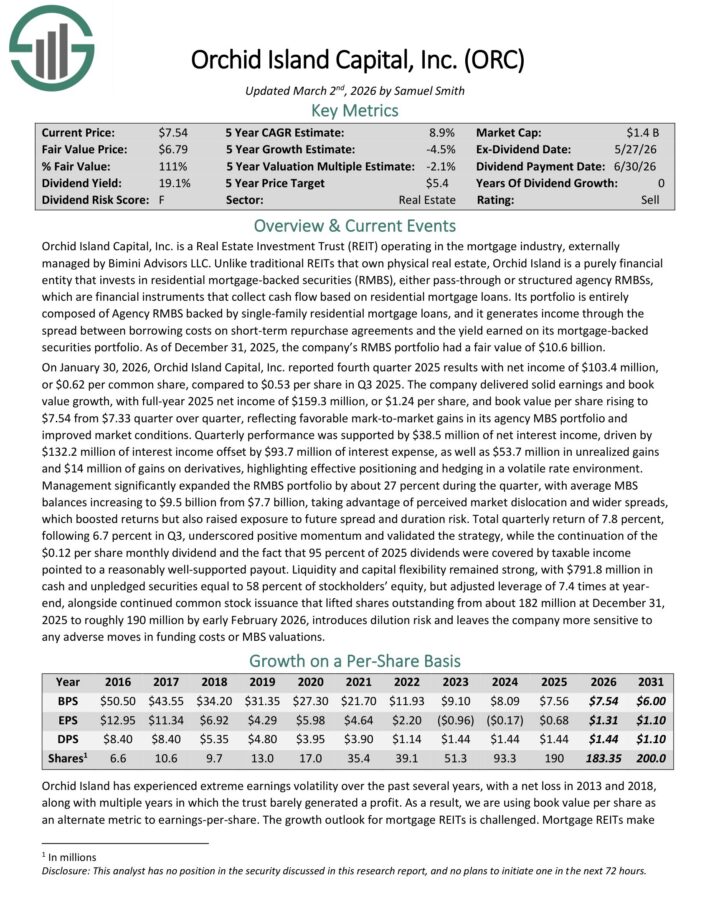

#2: Orchid Island Capital, Inc. (ORC)

Orchid Island Capital, Inc. is a Real Estate Investment Trust (REIT) operating in the mortgage industry, externally managed by Bimini Advisors LLC.

Orchid Island is a purely financial entity that invests in residential mortgage-backed securities (RMBS), either pass-through or structured agency RMBSs, which are financial instruments that collect cash flow based on residential mortgage loans.

Its portfolio is entirely composed of Agency RMBS backed by single-family residential mortgage loans.

On January 30, 2026, Orchid Island Capital, Inc. reported fourth quarter 2025 results with net income of $103.4 million, or $0.62 per common share, compared to $0.53 per share in Q3 2025.

The company delivered solid earnings and book value growth, with full-year 2025 net income of $159.3 million, or $1.24 per share, and book value per share rising to $7.54 from $7.33 quarter over quarter, reflecting favorable mark-to-market gains in its agency MBS portfolio and improved market conditions.

Quarterly performance was supported by $38.5 million of net interest income, driven by $132.2 million of interest income offset by $93.7 million of interest expense, as well as $53.7 million in unrealized gains and $14 million of gains on derivatives, highlighting effective positioning and hedging in a volatile rate environment.

Management significantly expanded the RMBS portfolio by about 27 percent during the quarter, with average MBS balances increasing to $9.5 billion from $7.7 billion, taking advantage of perceived market dislocation and wider spreads, which boosted returns but also raised exposure to future spread and duration risk.

Click here to download our most recent Sure Analysis report on ORC (preview of page 1 of 3 shown below):

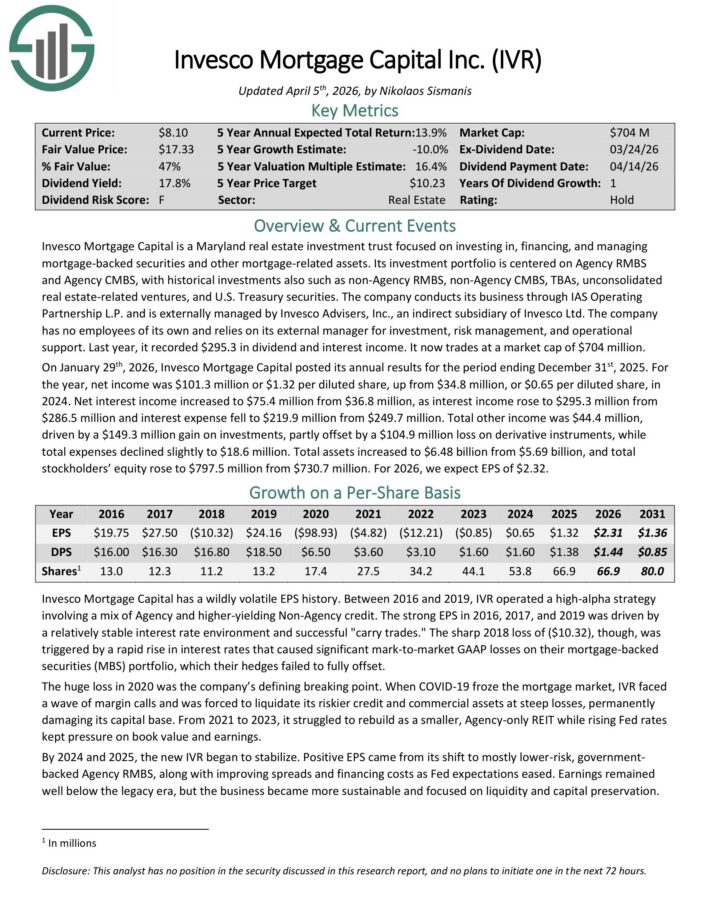

#1: Invesco Mortgage Capital (IVR)

Annual expected returns: 18.3%

Invesco Mortgage Capital is a Maryland real estate investment trust focused on investing in, financing, and managing mortgage-backed securities and other mortgage-related assets.

Its investment portfolio is centered on Agency RMBS and Agency CMBS, with historical investments also such as non-Agency RMBS, non-Agency CMBS, TBAs, unconsolidated real estate-related ventures, and U.S. Treasury securities.

The company conducts its business through IAS Operating Partnership L.P. and is externally managed by Invesco Advisers, Inc., an indirect subsidiary of Invesco Ltd.

The company has no employees of its own and relies on its external manager for investment, risk management, and operational support. Last year, it recorded $295.3 in dividend and interest income.

On January 29th, 2026, Invesco Mortgage Capital posted its annual results for the period ending December 31st, 2025. For the year, net income was $101.3 million or $1.32 per diluted share, up from $34.8 million, or $0.65 per diluted share, in 2024.

Net interest income increased to $75.4 million from $36.8 million, as interest income rose to $295.3 million from $286.5 million and interest expense fell to $219.9 million from $249.7 million.

Total other income was $44.4 million, driven by a $149.3 million gain on investments, partly offset by a $104.9 million loss on derivative instruments, while total expenses declined slightly to $18.6 million.

Total assets increased to $6.48 billion from $5.69 billion, and total stockholders’ equity rose to $797.5 million from $730.7 million.

For 2026, we expect EPS of $2.32.

Click here to download our most recent Sure Analysis report on IVR (preview of page 1 of 3 shown below):

Conclusion

As you can see from the dividend yields offered by the ten stocks discussed in this article, mREITs can be powerful passive income generators.

However, investors need to be careful before investing in this sector, given that dividend cuts can be common during periods of economic stress. As a result, diversification and a focus on quality are essential.

Additional Reading

You can see more high-quality dividend stocks in the following Sure Dividend databases, each based on long streaks of steadily rising dividend payments:

Alternatively, another great place to look for high-quality business is inside the portfolios of highly successful investors.

By analyzing the portfolios of legendary investors running multi-billion dollar investment portfolios, we are able to indirectly benefit from their million-dollar research budgets and personal investing expertise.

To that end, Sure Dividend has created the following two articles:

You might also be looking to create a highly customized dividend income stream to pay for life’s expenses.

The following lists provide useful information on high dividend stocks and stocks that pay monthly dividends:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

")

")

Remains One Of Warren Buffett’s Oldest Stock Picks")

")

{kind=link}