Published on May 12th, 2026 by Bob Ciura

Sure Dividend advocates a long-term buy-and-hold approach to generate rising dividends.

While this approach doesn’t require much in the way of day-to-day activity, it does require consistency.

Being consistent means not:

Getting swept up in market fads and periods of overoptimistic “animal spirits.”

Pouring your attention and wealth into speculative investments that may one day be able to pay dividends years down the line.

Instead, we recommend investing in quality businesses that have proven and continue to prove they can pay more in dividends year after year.

Therefore, we recommend investors buy-and-hold quality dividend stocks such as the Dividend Aristocrats, which are S&P 500 companies that have raised their dividends for at least 25 consecutive years.

You can download the full list of Dividend Aristocrats by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Holding through downturns is another important factor that investors should keep in mind.

The U.S. has been through multiple recessions in the past several decades, such as the Great Recession of 2007-2009 and the coronavirus pandemic of 2020.

But investors who sold during these periods missed out on significant gains when the markets subsequently recovered.

Holding (and preferably buying) through market draw-downs tends to be the most difficult part of maintaining consistency with your investing practice.

This article will list 10 consistent Dividend Aristocrats for long-term dividend compounding for the next 25 years and beyond.

Table of Contents

The table of contents below allows for easy navigation.

These 10 Dividend Aristocrats have Dividend Risk Scores of ‘A’, our highest ranking. They also have dividend payout ratios below 70%.

The stocks are listed by current dividend yield, from lowest to highest.

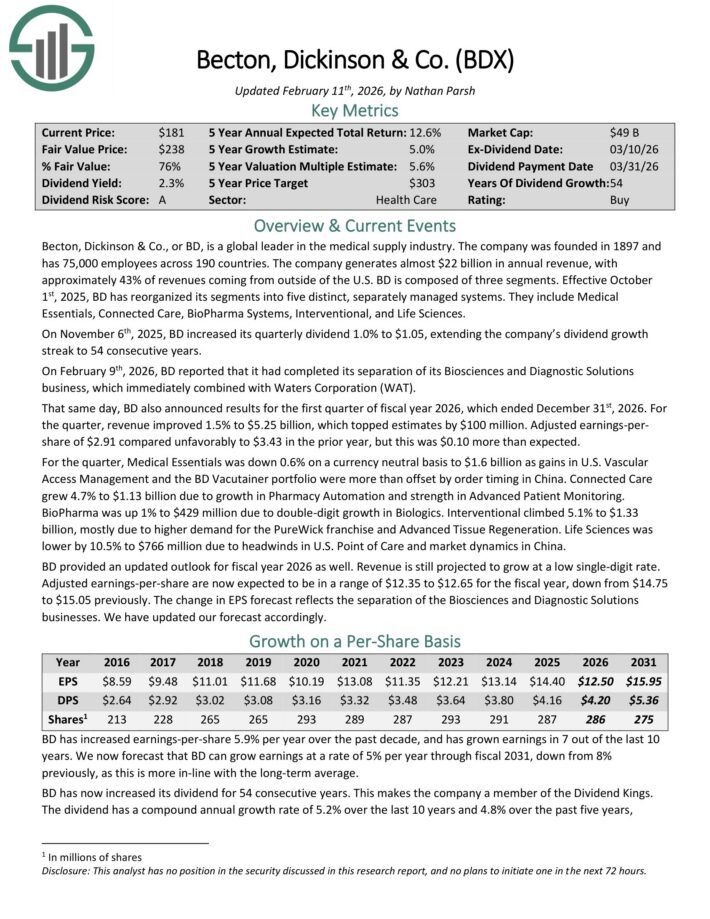

Consistent Dividend Aristocrat #10: Becton, Dickinson & Co. (BDX)

Becton, Dickinson & Co. is a global leader in the medical supply industry. The company was founded in 1897 and has 75,000 employees across 190 countries.

The company generates about $20 billion in annual revenue, with approximately 43% of revenues coming from outside of the U.S.

On November 6th, 2025, BD increased its quarterly dividend 1.0% to $1.05, extending the company’s dividend growth streak to 54 consecutive years.

BD also announced results for the first quarter of fiscal year 2026, which ended December 31st, 2026. For the quarter, revenue improved 1.5% to $5.25 billion, which topped estimates by $100 million.

Adjusted earnings-per-share of $2.91 compared unfavorably to $3.43 in the prior year, but this was $0.10 more than expected.

For the quarter, Medical Essentials was down 0.6% on a currency neutral basis to $1.6 billion as gains in U.S. Vascular Access Management and the BD Vacutainer portfolio were more than offset by order timing in China.

Connected Care grew 4.7% to $1.13 billion due to growth in Pharmacy Automation and strength in Advanced Patient Monitoring.

BioPharma was up 1% to $429 million due to double-digit growth in Biologics. Interventional climbed 5.1% to $1.33 billion, mostly due to higher demand for the PureWick franchise and Advanced Tissue Regeneration.

Click here to download our most recent Sure Analysis report on BDX (preview of page 1 of 3 shown below):

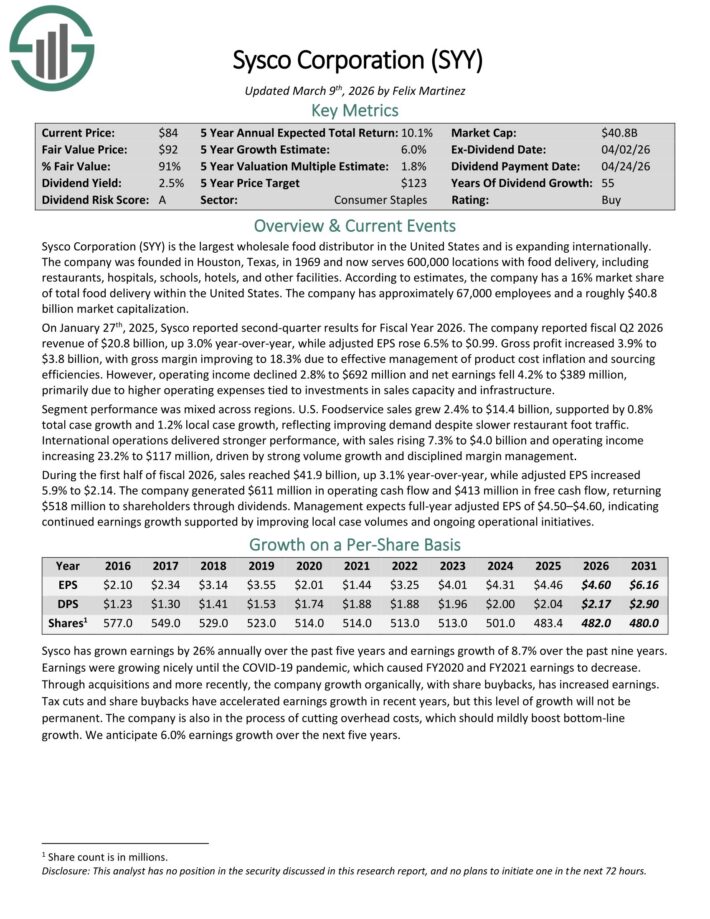

Consistent Dividend Aristocrat #9: Sysco Corp. (SYY)

Sysco Corporation is the largest wholesale food distributor in the United States and is expanding internationally.

The company was founded in Houston, Texas, in 1969 and now serves 600,000 locations with food delivery, including restaurants, hospitals, schools, hotels, and other facilities.

On January 27th, 2026, Sysco reported second-quarter results for Fiscal Year 2026. The company reported fiscal Q2 2026 revenue of $20.8 billion, up 3.0% year-over-year, while adjusted EPS rose 6.5% to $0.99.

Gross profit increased 3.9% to $3.8 billion, with gross margin improving to 18.3% due to effective management of product cost inflation and sourcing efficiencies.

However, operating income declined 2.8% to $692 million and net earnings fell 4.2% to $389 million, primarily due to higher operating expenses tied to investments in sales capacity and infrastructure.

Segment performance was mixed across regions. U.S. Foodservice sales grew 2.4% to $14.4 billion, supported by 0.8% total case growth and 1.2% local case growth, reflecting improving demand despite slower restaurant foot traffic.

International operations delivered stronger performance, with sales rising 7.3% to $4.0 billion and operating income increasing 23.2% to $117 million, driven by strong volume growth and disciplined margin management.

Management expects full-year adjusted EPS of $4.50–$4.60.

Click here to download our most recent Sure Analysis report on SYY (preview of page 1 of 3 shown below):

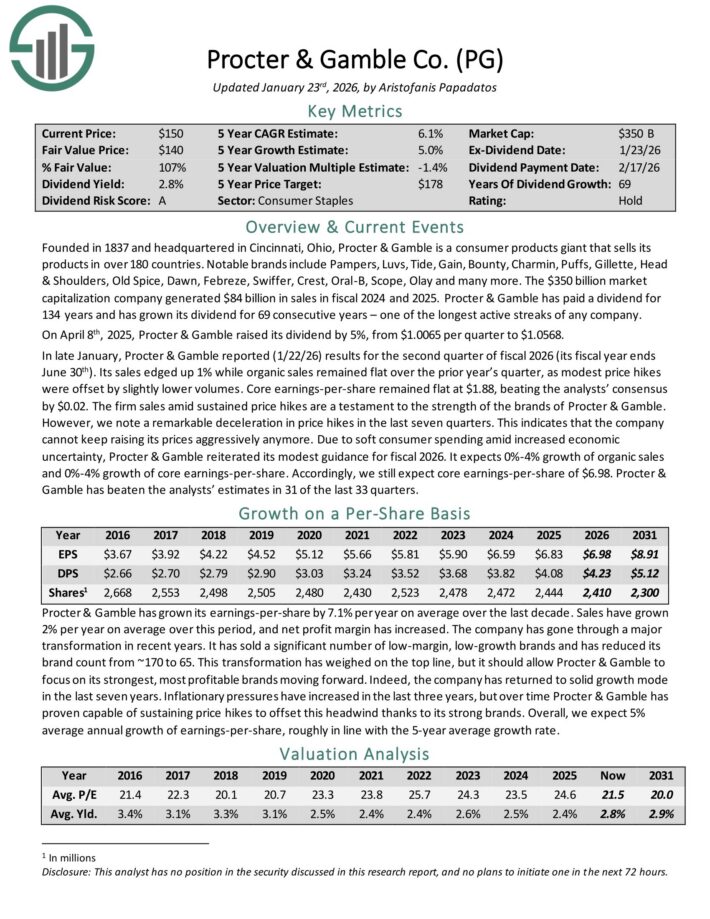

Consistent Dividend Aristocrat #8: Procter & Gamble (PG)

Procter & Gamble is a consumer products giant that sells its products in over 180 countries.

Notable brands include Pampers, Luvs, Tide, Gain, Bounty, Charmin, Puffs, Gillette, Head & Shoulders, Old Spice, Dawn, Febreze, Swiffer, Crest, Oral-B, Scope, Olay and many more.

The company generated $84 billion in sales in fiscal 2024 and 2025. Procter & Gamble has paid a dividend for 134 years and has grown its dividend for 69 consecutive years – one of the longest active streaks of any company.

In late January, Procter & Gamble reported (1/22/26) results for the second quarter of fiscal 2026. Its sales edged up 1% while organic sales remained flat over the prior year’s quarter, as modest price hikes were offset by slightly lower volumes.

Core earnings-per-share remained flat at $1.88, beating the analysts’ consensus by $0.02. The firm sales amid sustained price hikes are a testament to the strength of the brands of Procter & Gamble.

However, we note a remarkable deceleration in price hikes in the last seven quarters. This indicates that the company cannot keep raising its prices aggressively anymore.

Due to soft consumer spending amid increased economic uncertainty, Procter & Gamble reiterated its modest guidance for fiscal 2026. It expects 0%-4% growth of organic sales and 0%-4% growth of core earnings-per-share.

Click here to download our most recent Sure Analysis report on PG (preview of page 1 of 3 shown below):

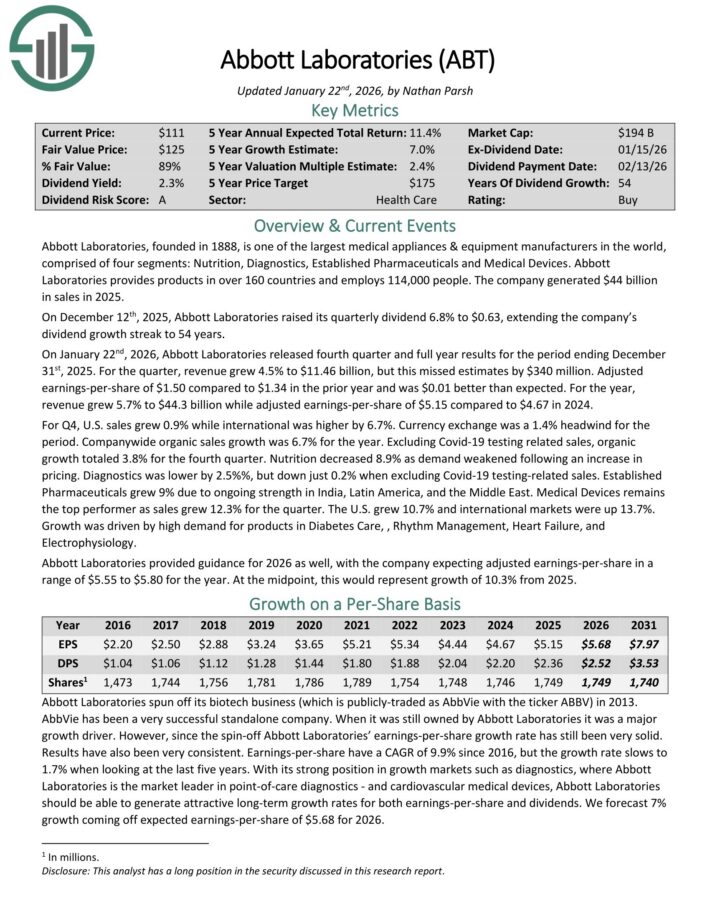

Consistent Dividend Aristocrat #7: Abbott Laboratories (ABT)

Abbott Laboratories, founded in 1888, is one of the largest medical appliances & equipment manufacturers in the world, comprised of four segments: Nutrition, Diagnostics, Established Pharmaceuticals and Medical Devices.

Abbott Laboratories provides products in over 160 countries and employs 114,000 people. The company generated $44 billion in sales in 2025.

On December 12th, 2025, Abbott Laboratories raised its quarterly dividend 6.8% to $0.63, extending the company’s dividend growth streak to 54 years.

On January 22nd, 2026, Abbott Laboratories released fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue grew 4.5% to $11.46 billion, but this missed estimates by $340 million.

Adjusted earnings-per-share of $1.50 compared to $1.34 in the prior year and was $0.01 better than expected. For the year, revenue grew 5.7% to $44.3 billion while adjusted earnings-per-share of $5.15 compared to $4.67 in 2024.

For Q4, U.S. sales grew 0.9% while international was higher by 6.7%. Currency exchange was a 1.4% headwind for the period.

Abbott Laboratories provided guidance for 2026 as well, with the company expecting adjusted earnings-per-share in a range of $5.55 to $5.80 for the year. At the midpoint, this would represent growth of 10.3% from 2025.

Click here to download our most recent Sure Analysis report on ABT (preview of page 1 of 3 shown below):

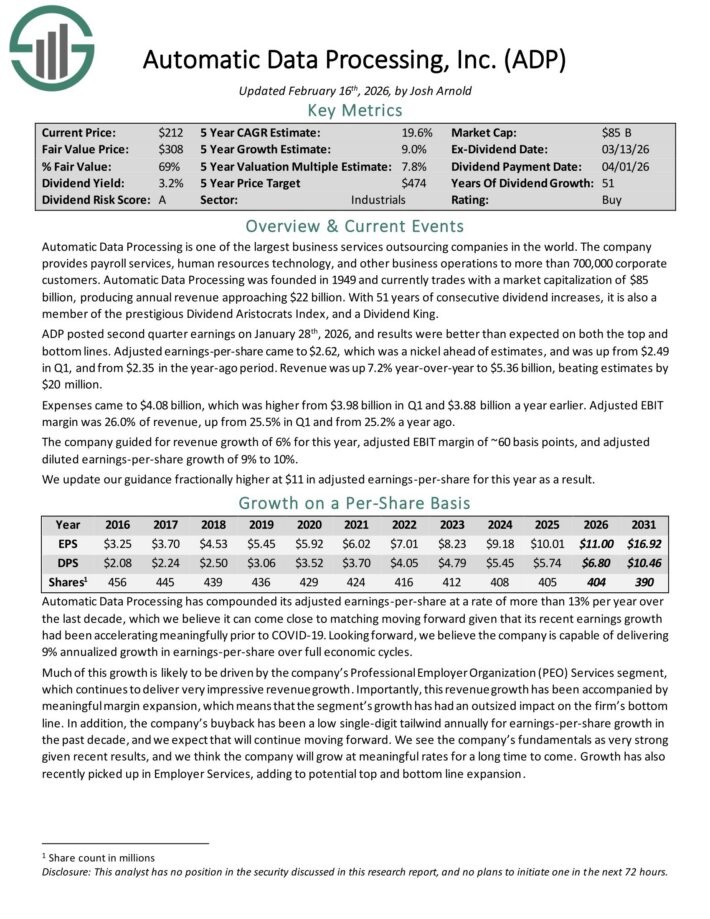

Undervalued Dividend Aristocrat #6: Automatic Data Processing (ADP)

Automatic Data Processing is one of the largest business services outsourcing companies in the world.

The company provides payroll services, human resources technology, and other business operations to more than 700,000 corporate customers.

ADP posted second quarter earnings on January 28th, 2026, and results were better than expected on both the top and bottom lines.

Adjusted earnings-per-share came to $2.62, which was a nickel ahead of estimates, and was up from $2.49 in Q1, and from $2.35 in the year-ago period. Revenue was up 7.2% year-over-year to $5.36 billion, beating estimates by $20 million.

Expenses came to $4.08 billion, which was higher from $3.98 billion in Q1 and $3.88 billion a year earlier. Adjusted EBIT margin was 26.0% of revenue, up from 25.5% in Q1 and from 25.2% a year ago.

The company guided for revenue growth of 6% for this year, adjusted EBIT margin of ~60 basis points, and adjusted diluted earnings-per-share growth of 9% to 10%.

Click here to download our most recent Sure Analysis report on ADP (preview of page 1 of 3 shown below):

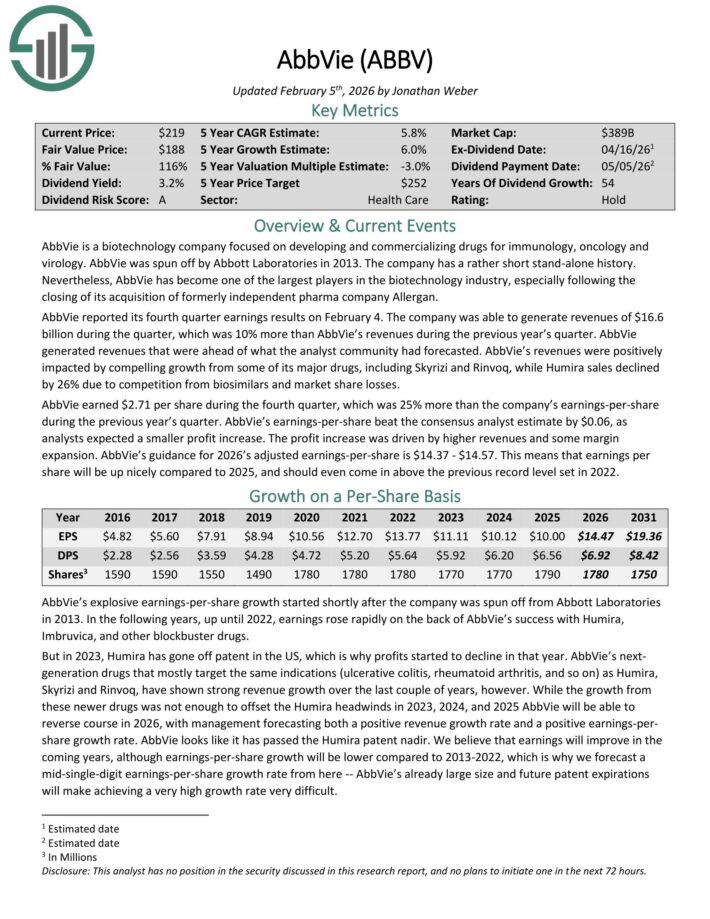

Consistent Dividend Aristocrat #5: AbbVie Inc. (ABBV)

AbbVie is a biotechnology company focused on developing and commercializing drugs for immunology, oncology and virology. It was spun off by Abbott Laboratories in 2013.

Since then, AbbVie has become one of the largest players in the biotechnology industry.

AbbVie reported its fourth quarter earnings results on February 4. The company generated revenue of $16.6 billion during the quarter, up 10% year-over-year.

Revenue was positively impacted by compelling growth from some of its major drugs, including Skyrizi and Rinvoq, while Humira sales declined by 26% due to competition from biosimilars and market share losses.

AbbVie earned $2.71 per share during the fourth quarter, which was 25% more than the company’s earnings-per-share during the previous year’s quarter.

AbbVie’s earnings-per-share beat the consensus analyst estimate by $0.06, as analysts expected a smaller profit increase.

The profit increase was driven by higher revenues and some margin expansion. AbbVie’s guidance for 2026’s adjusted earnings-per-share is $14.37 – $14.57.

Click here to download our most recent Sure Analysis report on ABBV (preview of page 1 of 3 shown below):

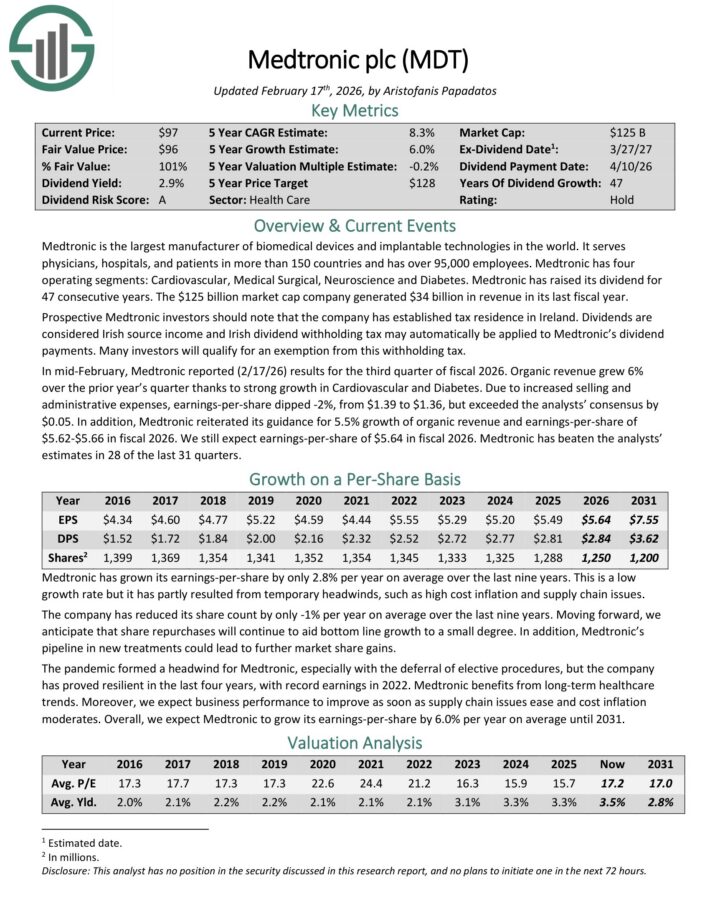

Consistent Dividend Aristocrat #4: Medtronic plc (MDT)

Medtronic is the largest manufacturer of biomedical devices and implantable technologies in the world.

It serves physicians, hospitals, and patients in more than 150 countries and has over 95,000 employees. Medtronic has four operating segments: Cardiovascular, Medical Surgical, Neuroscience and Diabetes.

The company generated $34 billion in revenue in its last fiscal year.

In mid-February, Medtronic reported (2/17/26) results for the third quarter of fiscal 2026. Organic revenue grew 6% over the prior year’s quarter thanks to strong growth in Cardiovascular and Diabetes.

Due to increased selling and administrative expenses, earnings-per-share dipped -2%, from $1.39 to $1.36, but exceeded the analysts’ consensus by $0.05.

In addition, Medtronic reiterated its guidance for 5.5% growth of organic revenue and earnings-per-share of $5.62-$5.66 in fiscal 2026.

Medtronic has raised its dividend for 47 consecutive years. It has grown its dividend by 9.7% per year on average over the last decade and by 5.6% per year on average over the last 5 years.

Click here to download our most recent Sure Analysis report on MDT (preview of page 1 of 3 shown below):

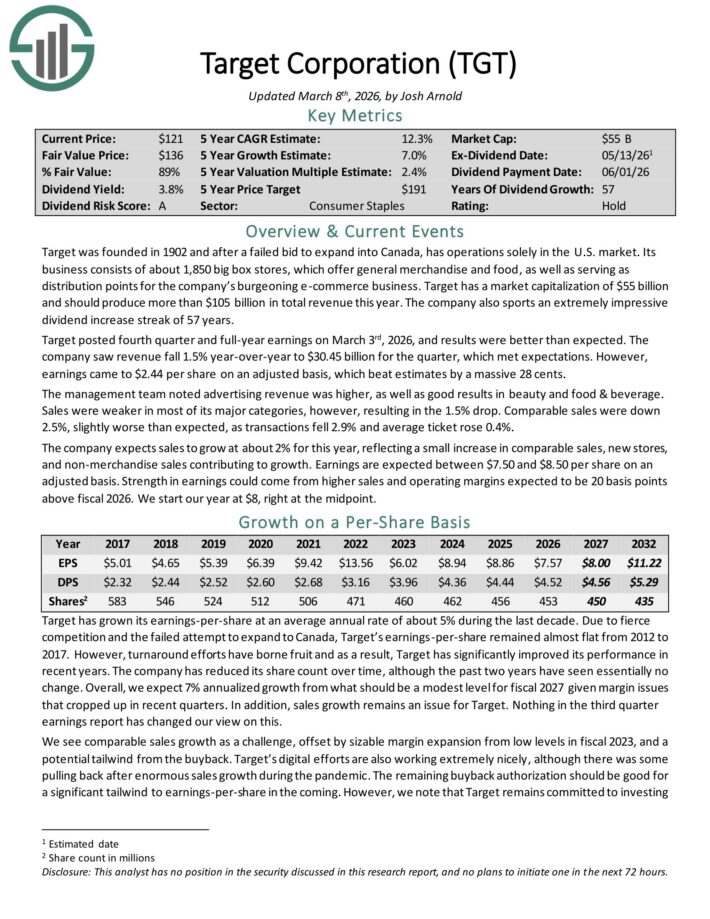

Consistent Dividend Aristocrat #3: Target Corporation (TGT)

Target was founded in 1902 and has operations solely in the U.S. market.

Its business consists of about 1,850 big box stores, which offer general merchandise and food, as well as serving as distribution points for the company’s burgeoning e-commerce business.

Target should produce more than $105 billion in total revenue this year. The company also sports an extremely impressive dividend increase streak of 57 years.

Target posted fourth quarter and full-year earnings on March 3rd, 2026, and results were better than expected. The company saw revenue fall 1.5% year-over-year to $30.45 billion for the quarter, which met expectations.

However, earnings came to $2.44 per share on an adjusted basis, which beat estimates by a massive 28 cents. The management team noted advertising revenue was higher, as well as good results in beauty and food & beverage.

Sales were weaker in most of its major categories, however, resulting in the 1.5% drop. Comparable sales were down 2.5%, slightly worse than expected, as transactions fell 2.9% and average ticket rose 0.4%.

The company expects sales to grow at about 2% for this year, reflecting a small increase in comparable sales, new stores, and non-merchandise sales contributing to growth.

Earnings are expected between $7.50 and $8.50 per share on an adjusted basis. Strength in earnings could come from higher sales and operating margins expected to be 20 basis points above fiscal 2026.

Click here to download our most recent Sure Analysis report on TGT (preview of page 1 of 3 shown below):

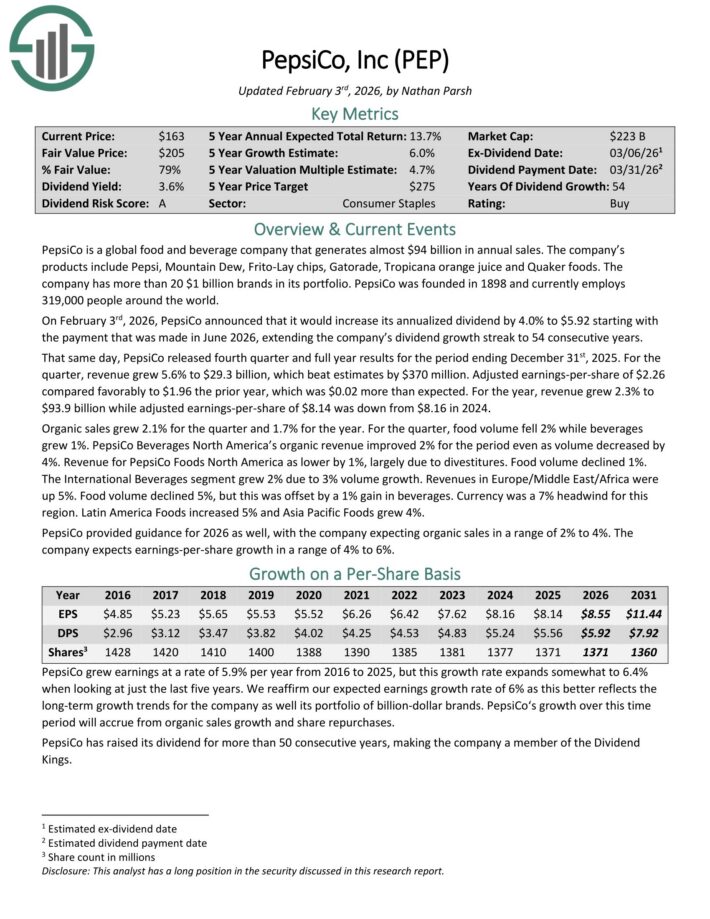

Consistent Dividend Aristocrat #2: PepsiCo Inc. (PEP)

PepsiCo is a global food and beverage company that generates almost $94 billion in annual sales. The company’s products include Pepsi, Mountain Dew, Frito-Lay chips, Gatorade, Tropicana orange juice and Quaker foods.

The company has more than 20 $1 billion brands in its portfolio.

On February 3rd, 2026, PepsiCo announced that it would increase its annualized dividend by 4.0% to $5.92 starting with the payment for June 2026, extending the company’s dividend growth streak to 54 consecutive years.

That same day, PepsiCo released fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue grew 5.6% to $29.3 billion, which beat estimates by $370 million.

Adjusted earnings-per-share of $2.26 compared favorably to $1.96 the prior year, which was $0.02 more than expected.

For the year, revenue grew 2.3% to $93.9 billion while adjusted earnings-per-share of $8.14 was down from $8.16 in 2024. Organic sales grew 2.1% for the quarter and 1.7% for the year.

For the quarter, food volume fell 2% while beverages grew 1%. PepsiCo Beverages North America’s organic revenue improved 2% for the period even as volume decreased by 4%.

Revenue for PepsiCo Foods North America as lower by 1%, largely due to divestitures. Food volume declined 1%.

The International Beverages segment grew 2% due to 3% volume growth. Revenues in Europe/Middle East/Africa were up 5%. Food volume declined 5%, but this was offset by a 1% gain in beverages.

Currency was a 7% headwind for this region. Latin America Foods increased 5% and Asia Pacific Foods grew 4%.

PepsiCo provided guidance for 2026 as well, with the company expecting organic sales in a range of 2% to 4%. The company expects earnings-per-share growth in a range of 4% to 6%.

Click here to download our most recent Sure Analysis report on PEP (preview of page 1 of 3 shown below):

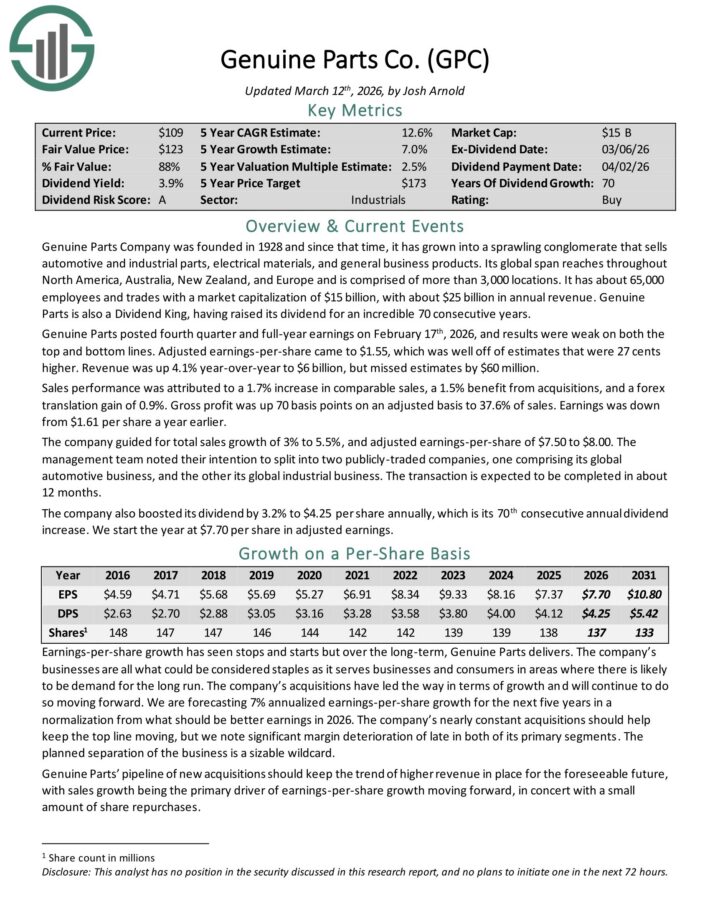

Consistent Dividend Aristocrat #1: Genuine Parts Co. (GPC)

Genuine Parts Company was founded in 1928 and since that time, it has grown into a sprawling conglomerate that sells automotive and industrial parts, electrical materials, and general business products.

Its global span reaches throughout North America, Australia, New Zealand, and Europe and is comprised of more than 3,000 locations. It has about 63,000 employees with about $24 billion in annual revenue.

Genuine Parts has raised its dividend for an incredible 69 consecutive years.

Genuine Parts posted fourth quarter and full-year earnings on February 17th, 2026, and results were weak on both the top and bottom lines.

Adjusted earnings-per-share came to $1.55, which was well off of estimates that were 27 cents higher. Revenue was up 4.1% year-over-year to $6 billion, but missed estimates by $60 million.

Sales performance was attributed to a 1.7% increase in comparable sales, a 1.5% benefit from acquisitions, and a forex translation gain of 0.9%.

Gross profit was up 70 basis points on an adjusted basis to 37.6% of sales. Earnings was down from $1.61 per share a year earlier.

The company guided for total sales growth of 3% to 5.5%, and adjusted earnings-per-share of $7.50 to $8.00.

Click here to download our most recent Sure Analysis report on GPC (preview of page 1 of 3 shown below):

Additional Reading

The following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases.

The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings.

The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}