Published on June 8th, 2026 by Bob Ciura

Benjamin Graham is widely considered to be the father of value investing.

He graduated 2nd in his class from the University of Columbia at the age of 20. He was offered instructing jobs in English, philosophy, and mathematics immediately after graduating.

Graham declined the offers and built one of the most successful and famous investing careers of all time.

Graham was both a successful investor and an excellent teacher of investing ideas. One of his more important quotes is below:

In the short run, the market is a voting machine, but in the long run, it is a weighing machine.

Graham’s above quote explains the sharp contrast between perception and reality in one eloquent sentence.

In the short run, perception matters.

Stock prices are guided by perception on a daily, monthly, and even yearly time frame.

But in the long run, performance matters.

Over periods of multiple years what drives stock prices is the underlying performance of the business (on a per share basis).

When you invest in businesses with long histories of growing dividends you are investing in businesses that are really making money, and really rewarding shareholders with that money.

The Dividend Champions are a group of quality dividend stocks that have raised their dividends for at least 25 consecutive years.

You can download your free copy of the Dividend Champions list, along with relevant financial metrics like price-to-earnings ratios, dividend yields, and payout ratios, by clicking on the link below:

The combination of low valuations and growing dividends could produce strong returns.

With that in mind, this article will rank 10 Benjamin Graham stocks that are the most undervalued stocks in the Sure Analysis Research Database, with over 25 consecutive years of dividend increases.

Table of Contents

You can skip to analysis of any individual Dividend Champion below:

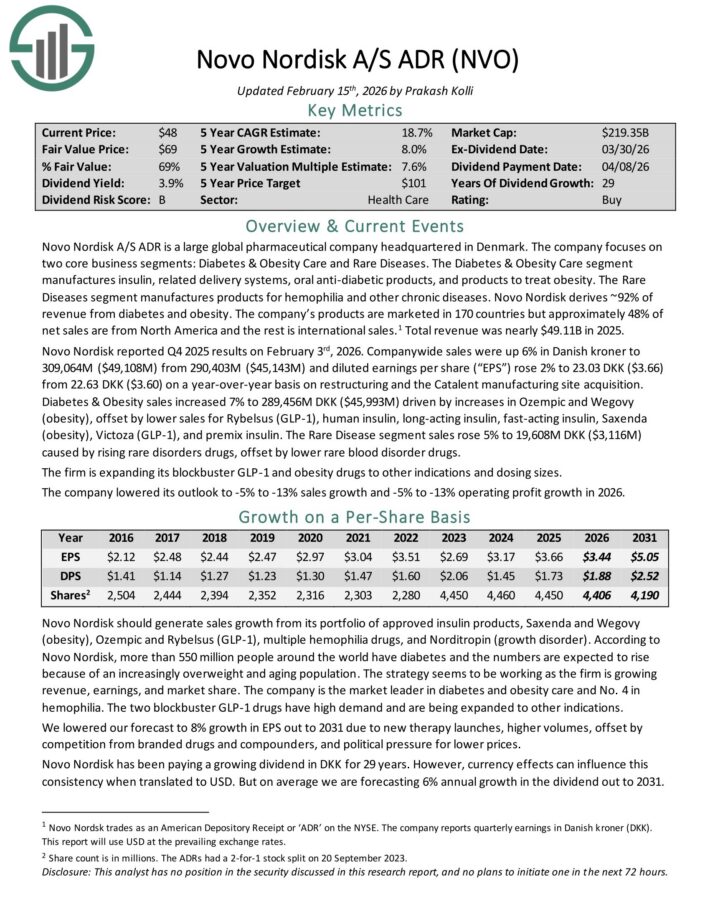

Benjamin Graham Stock #10: Novo Nordisk (NVO)

Annual Return From Valuation Multiple Expansion: 7.7%

Novo Nordisk A/S ADR is a large global pharmaceutical company headquartered in Denmark. The company focuses on two core business segments: Diabetes & Obesity Care and Rare Diseases.

The Diabetes & Obesity Care segment manufactures insulin, related delivery systems, oral anti-diabetic products, and products to treat obesity.

The Rare Diseases segment manufactures products for hemophilia and other chronic diseases. Novo Nordisk derives ~92% of revenue from diabetes and obesity.

The company’s products are marketed in 170 countries but approximately 48% of net sales are from North America and the rest is international sales.1 Total revenue was nearly $49.11B in 2025.

Novo Nordisk reported Q4 2025 results on February 3rd, 2026. Company-wide sales were up 6% in Danish kroner and diluted earnings per share rose 2% to 23.03 DKK ($3.66) from 22.63 DKK ($3.60) on a year-over-year basis.

Diabetes & Obesity sales increased 7% to 289,456M DKK ($45,993M) driven by increases in Ozempic and Wegovy (obesity), offset by lower sales for Rybelsus (GLP-1), human insulin, long-acting insulin, fast-acting insulin, Saxenda (obesity), Victoza (GLP-1), and premix insulin.

The Rare Disease segment sales rose 5% to 19,608M DKK ($3,116M) caused by rising rare disorders drugs, offset by lower rare blood disorder drugs.

Click here to download our most recent Sure Analysis report on NVO (preview of page 1 of 3 shown below):

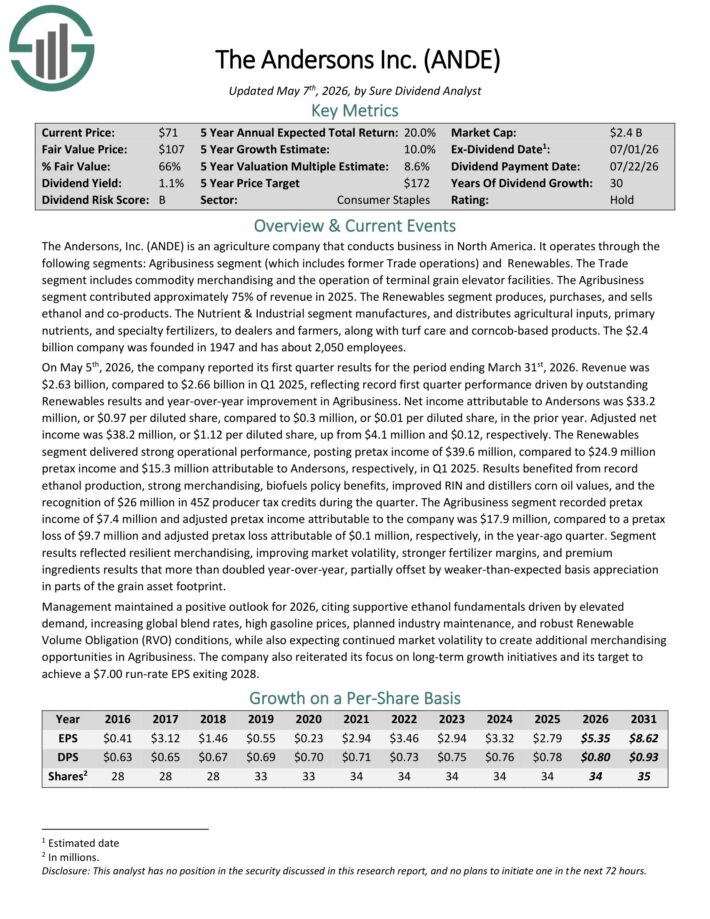

Benjamin Graham Stock #9: Andersons Inc. (ANDE)

Annual Return From Valuation Multiple Expansion: 8.0%

The Andersons is an agriculture company that conducts business in North America. It operates through the following segments: Agribusiness segment (which includes former Trade operations) and Renewables.

The Trade segment includes commodity merchandising and the operation of terminal grain elevator facilities. The Agribusiness segment contributed approximately 75% of revenue in 2025.

The Renewables segment produces, purchases, and sells ethanol and co-products. The Nutrient & Industrial segment manufactures, and distributes agricultural inputs, primary nutrients, and specialty fertilizers, to dealers and farmers, along with turf care and corncob-based products.

On May 5th, 2026, the company reported its first quarter results for the period ending March 31st, 2026. Revenue was $2.63 billion, compared to $2.66 billion in Q1 2025, reflecting record first quarter performance driven by outstanding Renewables results and year-over-year improvement in Agribusiness.

Net income attributable to Andersons was $33.2 million, or $0.97 per diluted share, compared to $0.3 million, or $0.01 per diluted share, in the prior year.

Adjusted net income was $38.2 million, or $1.12 per diluted share, up from $4.1 million and $0.12, respectively. The Renewables segment delivered strong operational performance, posting pretax income of $39.6 million, compared to $24.9 million pretax income and $15.3 million attributable to Andersons, respectively, in Q1 2025.

Click here to download our most recent Sure Analysis report on ANDE (preview of page 1 of 3 shown below):

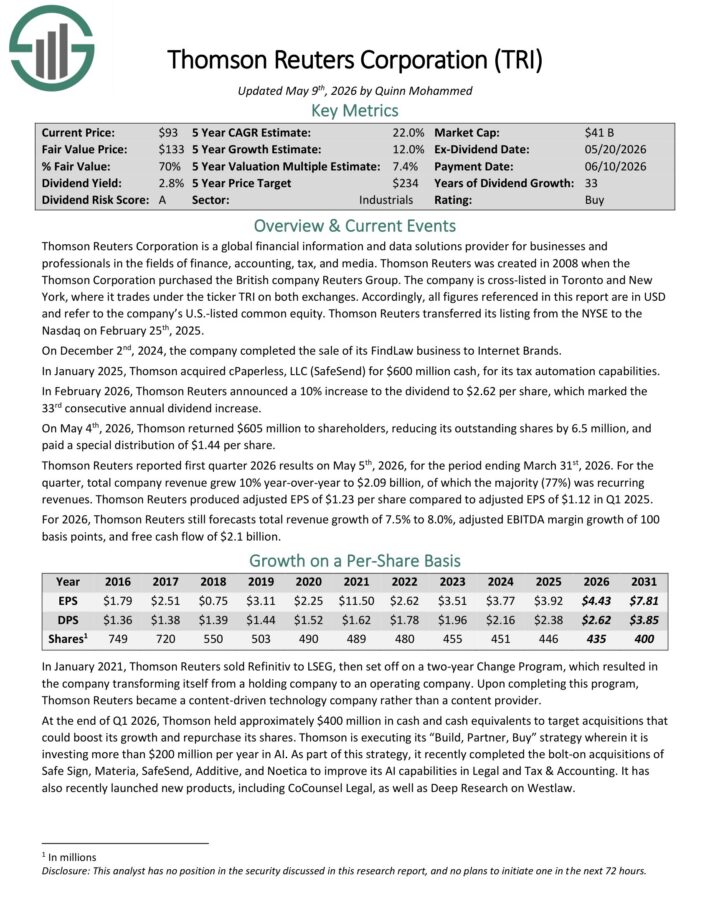

Benjamin Graham Stock #8: Thomson-Reuters (TRI)

Annual Return From Valuation Multiple Expansion: 9.2%

Thomson Reuters Corporation is a global financial information and data solutions provider for businesses and professionals in the fields of finance, accounting, tax, and media.

In February 2026, Thomson Reuters announced a 10% increase to the dividend to $2.62 per share, which marked the 33rd consecutive annual dividend increase.

Thomson Reuters reported first quarter 2026 results on May 5th, 2026. For the quarter, total company revenue grew 10% year-over-year to $2.09 billion, of which the majority (77%) was recurring revenue.

Thomson Reuters produced adjusted EPS of $1.23 per share compared to adjusted EPS of $1.12 in Q1 2025.

For 2026, Thomson Reuters still forecasts total revenue growth of 7.5% to 8.0%, adjusted EBITDA margin growth of 100 basis points, and free cash flow of $2.1 billion.

Click here to download our most recent Sure Analysis report on TRI (preview of page 1 of 3 shown below):

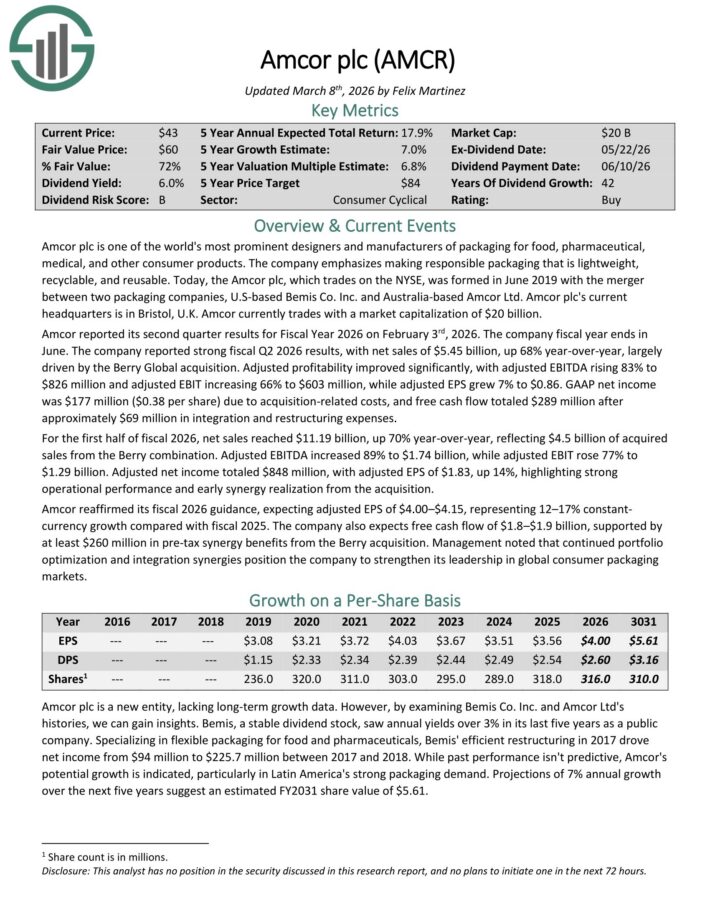

Benjamin Graham Stock #7: Amcor plc (AMCR)

Annual Return From Valuation Multiple Expansion: 9.6%

Amcor plc is one of the world’s most prominent designers and manufacturers of packaging for food, pharmaceutical, medical, and other consumer products.

Amcor reported its second quarter results for Fiscal Year 2026 on February 3rd, 2026. The company reported strong fiscal Q2 2026 results, with net sales of $5.45 billion, up 68% year-over-year, largely driven by the Berry Global acquisition.

Adjusted profitability improved significantly, with adjusted EBITDA rising 83% to $826 million and adjusted EBIT increasing 66% to $603 million, while adjusted EPS grew 7% to $0.86.

GAAP net income was $177 million ($0.38 per share) due to acquisition-related costs, and free cash flow totaled $289 million after approximately $69 million in integration and restructuring expenses.

For the first half of fiscal 2026, net sales reached $11.19 billion, up 70% year-over-year, reflecting $4.5 billion of acquired sales from the Berry combination.

Amcor reaffirmed its fiscal 2026 guidance, expecting adjusted EPS of $4.00–$4.15, representing 12–17% constant currency growth compared with fiscal 2025.

The company also expects free cash flow of $1.8–$1.9 billion, supported by at least $260 million in pre-tax synergy benefits from the Berry acquisition.

Click here to download our most recent Sure Analysis report on AMCR (preview of page 1 of 3 shown below):

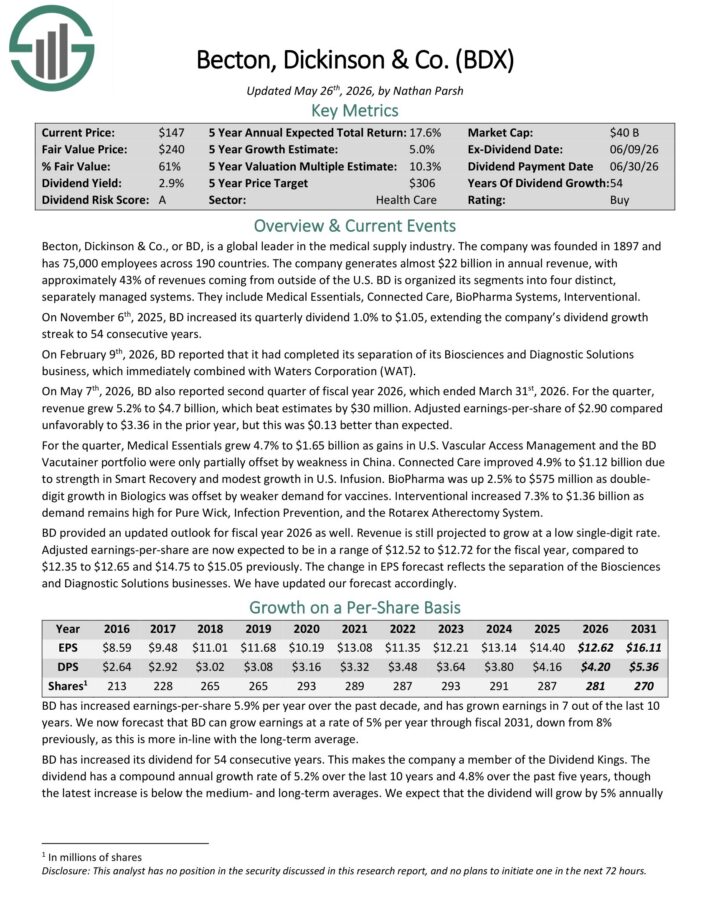

Benjamin Graham Stock #6: Becton, Dickinson & Co. (BDX)

Annual Return From Valuation Multiple Expansion: 9.7%

Becton, Dickinson & Co. is a global leader in the medical supply industry. The company was founded in 1897 and has 75,000 employees across 190 countries.

The company generates about $20 billion in annual revenue, with approximately 43% of revenues coming from outside of the U.S.

On November 6th, 2025, BD increased its quarterly dividend 1.0% to $1.05, extending the company’s dividend growth streak to 54 consecutive years.

On May 7th, 2026, BDX also reported second quarter of fiscal year 2026, which ended March 31st, 2026. For the quarter, revenue grew 5.2% to $4.7 billion, which beat estimates by $30 million.

Adjusted earnings-per-share of $2.90 compared unfavorably to $3.36 in the prior year, but this was $0.13 better than expected.

Click here to download our most recent Sure Analysis report on BDX (preview of page 1 of 3 shown below):

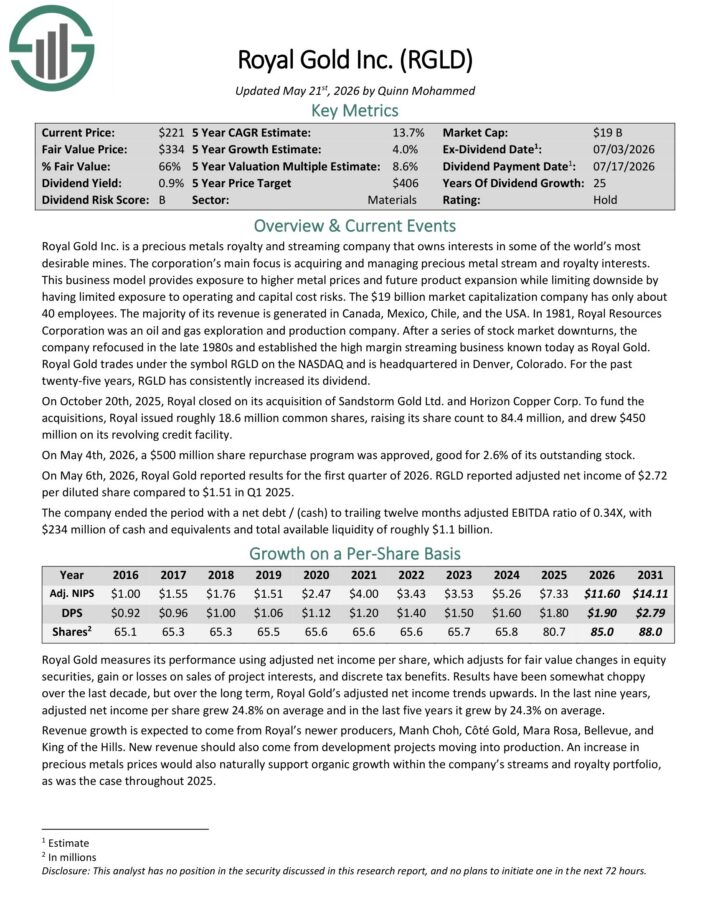

Benjamin Graham Stock #5: Royal Gold (RGLD)

Annual Return From Valuation Multiple Expansion: 9.8%

Royal Gold Inc. is a precious metals royalty and streaming company that owns interests in some of the world’s most desirable mines.

The corporation’s main focus is acquiring and managing precious metal stream and royalty interests.

This business model provides exposure to higher metal prices and future product expansion while limiting downside by having limited exposure to operating and capital cost risks.

The majority of its revenue is generated in Canada, Mexico, Chile, and the USA.

On May 4th, 2026, a $500 million share repurchase program was approved, good for 2.6% of its outstanding stock.

On May 6th, 2026, Royal Gold reported results for the first quarter of 2026. RGLD reported adjusted net income of $2.72 per diluted share compared to $1.51 in Q1 2025.

The company ended the period with a net debt / (cash) to trailing twelve months adjusted EBITDA ratio of 0.34X, with $234 million of cash and equivalents and total available liquidity of roughly $1.1 billion.

Click here to download our most recent Sure Analysis report on RGLD (preview of page 1 of 3 shown below):

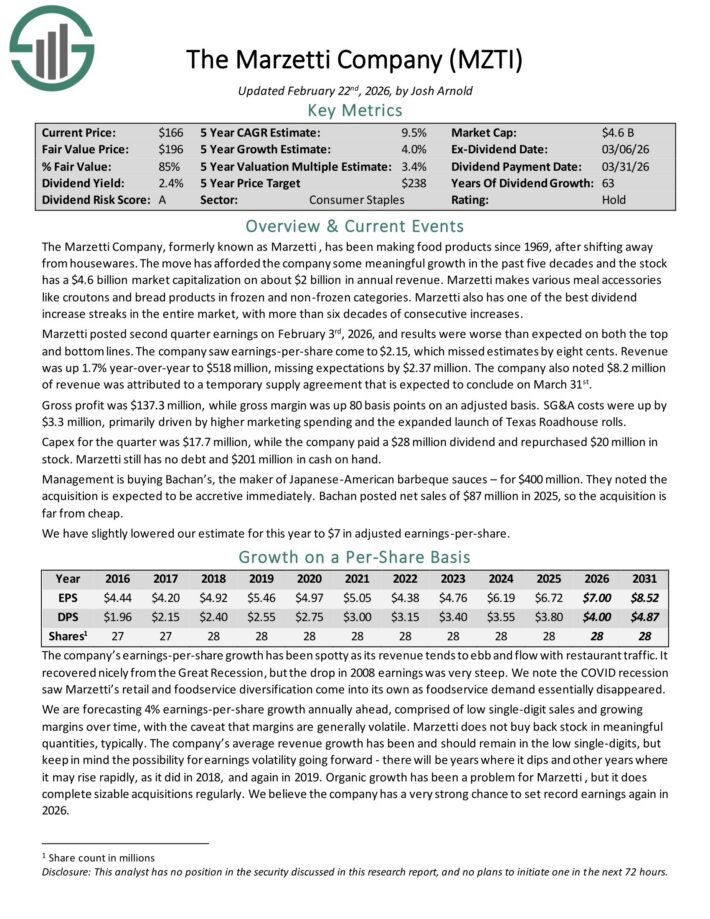

Benjamin Graham Stock #4: The Marzetti Company (MZTI)

Annual Return From Valuation Multiple Expansion: 12.0%

The Marzetti Company has been making food products since 1969. Marzetti makes various meal accessories like croutons and bread products in frozen and non-frozen categories.

Marzetti also has one of the best dividend increase streaks in the entire market, with more than six decades of consecutive increases.

Marzetti posted second quarter earnings on February 3rd, 2026, and results were worse than expected on both the top and bottom lines. The company saw earnings-per-share come to $2.15, which missed estimates by eight cents.

Revenue was up 1.7% year-over-year to $518 million, missing expectations by $2.37 million. The company also noted $8.2 million of revenue was attributed to a temporary supply agreement that is expected to conclude on March 31st.

Gross profit was $137.3 million, while gross margin was up 80 basis points on an adjusted basis. SG&A costs were up by $3.3 million, primarily driven by higher marketing spending and the expanded launch of Texas Roadhouse rolls.

Capex for the quarter was $17.7 million, while the company paid a $28 million dividend and repurchased $20 million in stock. Marzetti still has no debt and $201 million in cash on hand.

Management is buying Bachan’s, the maker of Japanese-American barbeque sauces – for $400 million. They noted the acquisition is expected to be accretive immediately.

Click here to download our most recent Sure Analysis report on MZTI (preview of page 1 of 3 shown below):

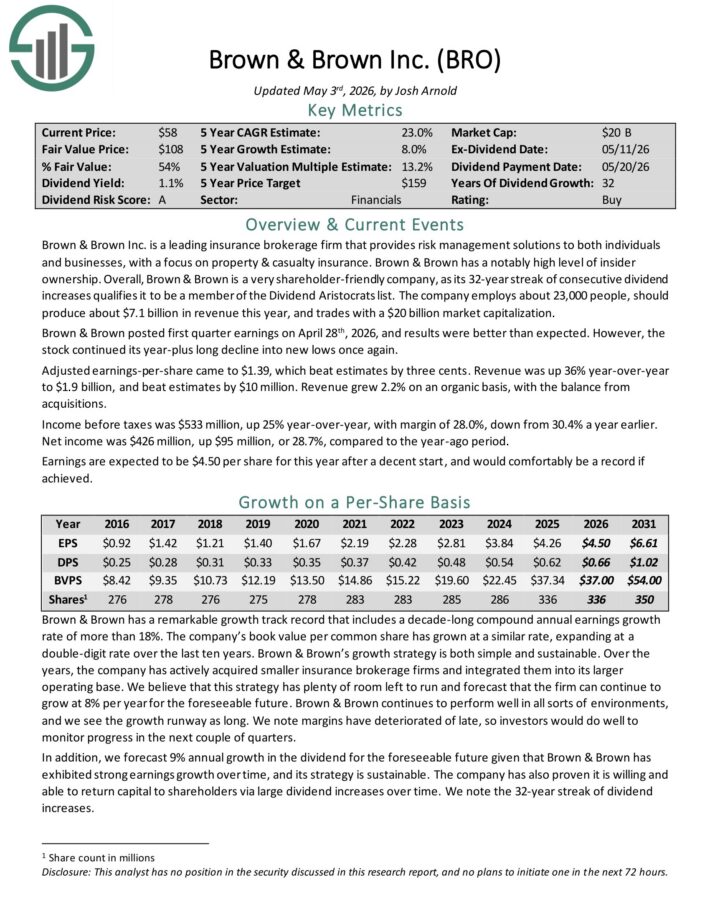

Benjamin Graham Stock #3: Brown & Brown (BRO)

Annual Return From Valuation Multiple Expansion: 12.9%

Brown & Brown Inc. is a leading insurance brokerage firm. It provides risk management solutions to both individuals and businesses, with a focus on property & casualty insurance.

Brown & Brown is a very shareholder-friendly company, as its 32-year streak of consecutive dividend increases qualifies it to be a member of the Dividend Aristocrats list.

The company employs about 23,000 people, should produce about $7.1 billion in revenue this year.

Brown & Brown posted first quarter earnings on April 28th, 2026, and results were better than expected.

Adjusted earnings-per-share came to $1.39, which beat estimates by three cents. Revenue was up 36% year-over-year to $1.9 billion, and beat estimates by $10 million. Revenue grew 2.2% on an organic basis, with the balance from acquisitions.

Income before taxes was $533 million, up 25% year-over-year, with margin of 28.0%, down from 30.4% a year earlier. Net income was $426 million, up $95 million, or 28.7%, compared to the year-ago period.

Click here to download our most recent Sure Analysis report on BRO (preview of page 1 of 3 shown below):

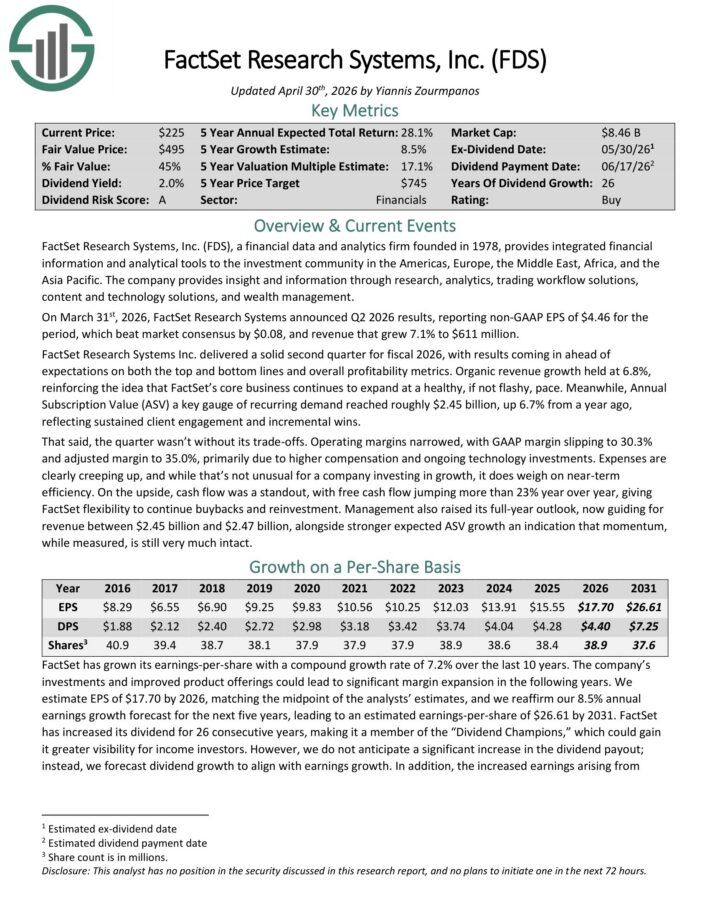

Benjamin Graham Stock #2: Factset Research Systems (FDS)

Annual Return From Valuation Multiple Expansion: 14.1%

FactSet Research Systems provides integrated financial information and analytical tools to the investment community in the Americas, Europe, the Middle East, Africa, and Asia-Pacific.

The company provides insight and information through research, analytics, trading workflow solutions, content and technology solutions, and wealth management.

On March 31st, 2026, FactSet Research Systems announced Q2 2026 results, reporting non-GAAP EPS of $4.46 for the period, which beat market consensus by $0.08.

Revenue grew 7.1% to $611 million. Organic revenue growth held at 6.8%, while Annual Subscription Value (ASV) a key gauge of recurring demand reached roughly $2.45 billion, up 6.7% from a year ago.

Operating margins narrowed, with GAAP margin slipping to 30.3% and adjusted margin to 35.0%, primarily due to higher compensation and ongoing technology investments.

Free cash flow jumped 23% year over year, giving FactSet flexibility to continue buybacks and reinvestment.

Management also raised its full-year outlook, now guiding for revenue between $2.45 billion and $2.47 billion.

Click here to download our most recent Sure Analysis report on FDS (preview of page 1 of 3 shown below):

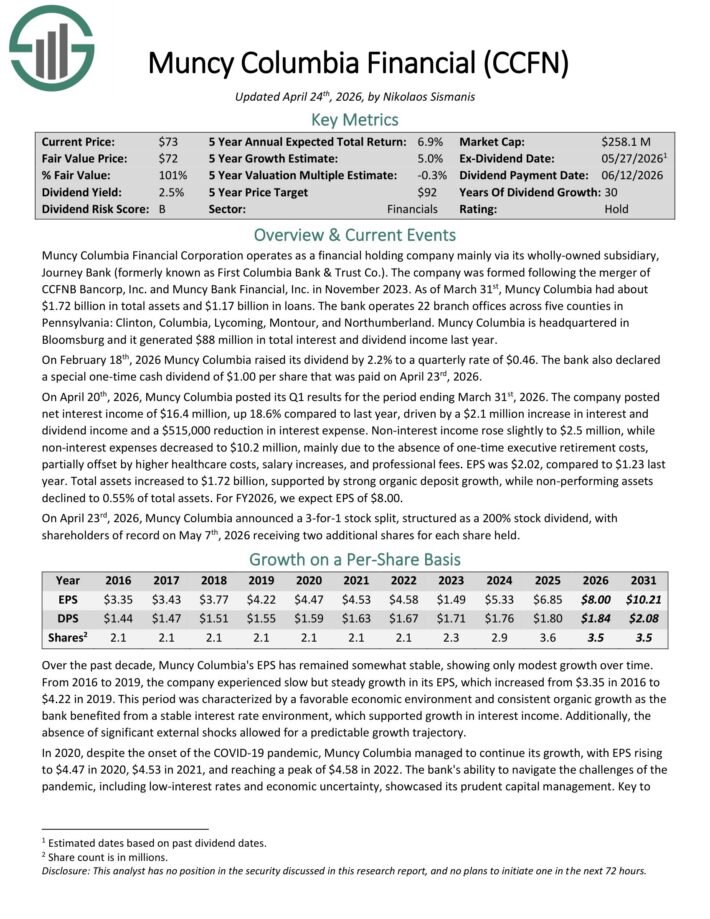

Benjamin Graham Stock #1: Muncy Columbia Financial (CCFN)

Annual Return From Valuation Multiple Expansion: 21.7%

Muncy Columbia Financial Corporation operates as a financial holding company mainly via its wholly-owned subsidiary, Journey Bank (formerly known as First Columbia Bank & Trust Co.).

As of March 31st, Muncy Columbia had about $1.72 billion in total assets and $1.17 billion in loans. The bank operates 22 branch offices across five counties in Pennsylvania: Clinton, Columbia, Lycoming, Montour, and Northumberland.

On February 18th, 2026 Muncy Columbia raised its dividend by 2.2% to a quarterly rate of $0.46. The bank also declared a special one-time cash dividend of $1.00 per share that was paid on April 23rd, 2026.

On April 20th, 2026, Muncy Columbia posted its Q1 results for the period ending March 31st, 2026. The company posted net interest income of $16.4 million, up 18.6% compared to last year, driven by a $2.1 million increase in interest and dividend income and a $515,000 reduction in interest expense.

Non-interest income rose slightly to $2.5 million, while non-interest expenses decreased to $10.2 million, mainly due to the absence of one-time executive retirement costs, partially offset by higher healthcare costs, salary increases, and professional fees.

EPS was $2.02, compared to $1.23 last year. Total assets increased to $1.72 billion, supported by strong organic deposit growth, while non-performing assets declined to 0.55% of total assets. For FY2026, we expect EPS of $8.00.

Click here to download our most recent Sure Analysis report on CCFN (preview of page 1 of 3 shown below):

Additional Resources

At Sure Dividend, we often advocate for investing in companies with a high probability of increasing their dividends each and every year.

If that strategy appeals to you, it may be useful to browse through the following databases of dividend growth stocks:

The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 58 stocks with 50+ years of consecutive dividend increases.

The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}