Note: The following is the written testimony of Cristina Enache, Economist, submitted to the Committee on Budgets and European Parliament on 23 June, 2026.

Dear Chair Van Overtveldt and Distinguished Members of the Committee on Budgets and European Parliament, thank you for the opportunity to discuss the taxation of digital activities in Europe and whether a digital levy could be a solution for the EU budget. I am Cristina Enache, Economist at TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Foundation Europe.

Starting with the assumption that the EU requires additional own resources, the key question becomes whether a digital services tax (DST) is a principled option for funding the EU budget—and, if not, which paths should be considered.

First, I will begin by reviewing the existing national DSTs, international negotiations to remove them, and the EU-wide proposal for a DST.

Second, I will evaluate the revenue generated by DSTs and their economic incidence.

Third, I will analyze the design issues of DSTs and the economic distortions they create, as well as their implications for competitiveness, innovation, compliance costs, and Single Market cohesion.

Fourth, I will examine the international responses and trade-related consequences that countries and the EU may face when enforcing a DST.

Finally, I will explore alternative instruments, such as value-added tax (VAT)-based resources, as this is where Europe’s fiscal strength truly lies.

The Context and Emergence of Digital Services Taxes

Under current international tax rules, multinationals generally pay corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. where production occurs rather than where consumers—or, in the digital sector, users—are located. However, proponents of new digital taxes argue that firms can derive income from users abroad but, without a physical presence, avoid corporate income taxation in those countries.

To address these concerns, in 2013, the Organisation for Economic Co-operation and Development (OECD) started international discussions on how to tax digital activities. In 2019, the OECD launched negotiations involving over 140 countries to reform international tax rules. This process culminated in 2021 in the proposal known as Pillar One, which aims to reallocate taxing rights so that some profits are taxed where consumers are located.

Despite these ongoing multilateral negotiations, several countries have decided to unilaterally move ahead with a different form of digital taxation—namely, DSTs. However, the first proposed DST came from the European Commission, in the form of an EU-wide DST.

In March 2018, the European Commission proposed rules to tax companies with a significant digital presence, alongside a temporary DST as an interim measure.

The proposed DST would levy a 3 percent tax on revenues from digital advertising, online marketplaces, and user data sales within the EU. It would apply to firms with global revenues that exceed €750 million and EU revenues that exceed €50 million. The measure was expected to raise between €1.3 billion and €5 billion annually—around 0.07 percent of total EU tax revenues and about 2.6 percent of the EU budget.

However, the proposal failed to gain unanimous support.

As a result, individual countries moved forward on their own. Right now, roughly half of the European OECD countries have announced, proposed, or already implemented a DST.

In fact, 10 countries—Austria, Denmark, France, Hungary, Italy, Poland, Portugal, Spain, Turkey, and the UK—have implemented a DST.

That said, these taxes look very different from one country to another. For example, Austria and Hungary focus solely on online advertising revenue, with the stated goal of aligning the tax treatment of online and offline ads. Denmark has also taken a much narrower approach by only applying its DST to streaming services.

France, on the other hand, has opted for a much broader tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates., covering revenues from digital platforms, targeted advertising, and even the sale of user data collected for advertising purposes.

Tax rates also vary quite a bit—ranging from 1.5 percent in Poland to 7.5 percent in Hungary and Turkey. However, Hungary has reduced its rate to zero, and Turkey lowered its rate to 5 percent starting 1 January 2026.

At the same time, six countries—Belgium, the Czech Republic, Latvia, Norway, Slovakia, and Slovenia—have either formally announced or explored the introduction of a DST. However, none of these initiatives has become law.

More recently, Germany examined the possibility of introducing a DST, while Poland considered a new, broader version of such a tax. Neither of these proposals is expected to move forward.

This lack of harmonization has created complexity and fragmentation across the Single Market.

In theory, Pillar One would replace unilateral measures like DSTs, as reflected in the agreement with the US in 2021. But in practice, the negotiations have stalled, and countries continue to act independently.

At the same time, the UN introduced provisions for taxing income from automated digital services (Article 12B of the UN Model Tax Convention), applicable to countries that adopt them. In November 2024, it also launched negotiations for a new treaty on tax cooperation, with a target of concluding talks by 2027.

Digital Services Taxes Generate Very Limited Revenue

Let’s now turn to the first key issue: revenue. Despite the political attention they receive, DSTs generate very limited income. In countries that have implemented them, revenues range from about €137 million in Austria to around €1 billion in the UK. As a share of total government revenue, they are typically below 0.1 percent, and even in the highest case—Turkey—they reach only about 0.24 percent.

At the EU level, the European Commission has estimated that a DST could raise up to €5 billion annually. To put this into perspective, this represents roughly 0.07 percent of total EU tax revenues and about 2.6 percent of the EU budget—a negligible contribution relative to the EU’s overall financing needs. In short, if the objective is to fund the EU budget in a meaningful way, DSTs simply do not deliver.

Table 1. Recent Revenue Raised from Selected Digital Services Taxes

Note: These countries have been selected because they report digital services tax revenue separately as a line item.Source: Tax Foundation Europe analysis of national budget documents and announcements.

Who Really Pays the Digital Services Taxes?

The second issue is even more important: who ultimately bears the burden of these taxes? Although DSTs are often presented as targeting large digital companies, the economic reality is different. DSTs are levied on gross revenues, not profits, making them similar to excise taxes—and, like excise taxes, they are largely passed on to consumers. In this sense, DSTs are to imported services what tariffs are to imported goods, and the economic incidence ultimately falls on consumers.[1]

There is clear evidence of this. Companies such as Google, Amazon, and Apple have introduced surcharges in response to DSTs, passing the costs on through higher advertising fees, increased marketplace charges, and ultimately higher consumer prices.

Academic research confirms that most of the burden falls on European users and businesses, rather than on the shareholders of large tech firms. This has two key implications. First, DSTs are regressive, disproportionately affecting lower-income consumers. Second, they place an added burden on European businesses, particularly small firms that rely on digital platforms. As a result, instead of effectively targeting foreign tech giants, DSTs often end up harming domestic economies.

Digital Services Taxes Have Design Problems and Create Economic Distortions

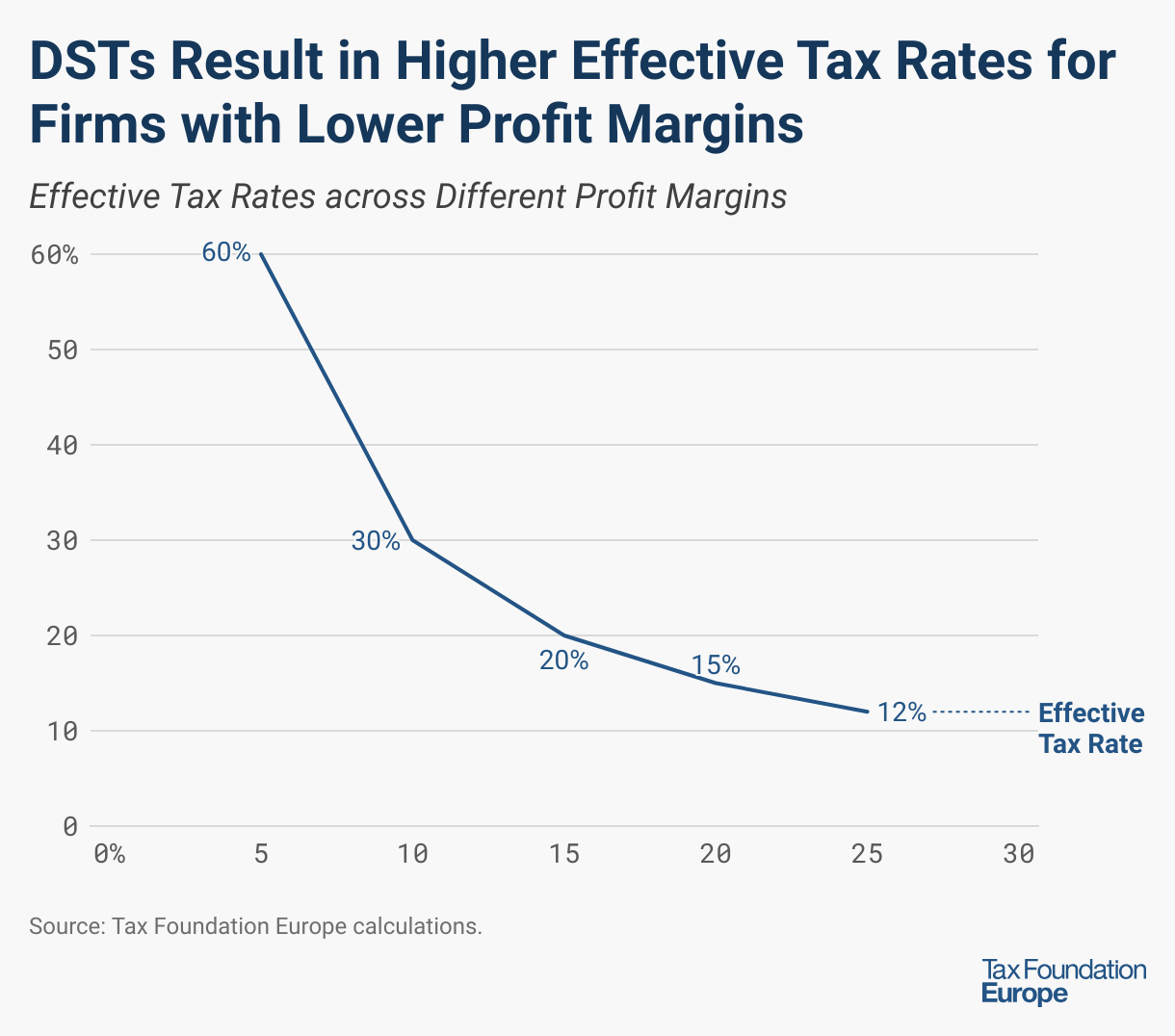

DSTs also face significant design flaws. Because they are levied on revenue rather than profit, they apply even when companies are not profitable and can result in very high effective tax rates—especially for low-margin businesses.

For example, a company with €100 in revenue and €15 in profit faces a 3 percent DST (€3 in tax), which translates into a 20 percent tax on profits. If the profit margin is lower, the effective tax rate rises dramatically—up to 60 percent or more.

This creates significant distortions: it penalizes low-margin firms, discourages investment and growth, and distorts business decisions.

In addition, DSTs can lead to tax pyramidingTax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action., as the same activity may be taxed multiple times along the supply chain due to the absence of a credit mechanism like that used in VAT. They may also apply to business inputs such as advertising and cloud services. Due to this tax pyramiding, DSTs also penalize the specialization needed to make the economy more productive.

DSTs can be discriminatory as well, targeting larger firms through revenue thresholds and treating digital businesses less favorably than traditional ones.

Finally, they impose substantial administrative burdens. Governments must design and enforce complex rules, while companies are required to track user locations and comply with multiple national systems.

Because DSTs vary widely in design and administration, businesses face high compliance costs when navigating these differences. Historically, Europe replaced turnover taxes with a VAT in the 1960s to improve the functioning of the Single Market. By reintroducing similar features, DSTs risk bringing back the economic inefficiencies of turnover taxes—a step backward in sound tax policy.[2] All of this makes DSTs inefficient, complex, and economically harmful.

International Tensions and Trade Risks

Another major issue is international conflict. DSTs are widely seen as targeting US-based technology companies, which has led to tensions with the United States. In recent years, the US has launched investigations under Section 301 and threatened retaliatory tariffs. This raises the risk of escalating trade disputes. An EU-wide DST would likely trigger stronger trade tensions than the current system of national DSTs. In a global economy, unilateral tax measures can easily lead to tit-for-tat responses, ultimately harming all sides.

A Better Alternative to Digital Services Taxes: VAT-Based Own Resources

So, if DSTs are not the answer, what is? The most promising alternative is already in place: VAT. If the goal is to raise more revenue from digital services, the EU should build on VAT by continuing to tax these services at the point of consumption. VAT has already been adapted to the digital economy, requiring non-EU firms to register and pay where consumers are located.

This approach has proven highly effective: revenues grew from €3 billion in 2015 to over €33 billion in 2024—around seven times the estimated yield of an EU-wide DST. Expanding VAT to fully cover digital services could therefore replace the need for DSTs altogether.

In other words, the EU already has a tool that works and performs far better than DSTs.

If the aim is to increase EU budget resources, the focus should not be on creating new own resources, but on encouraging Member States to improve VAT collection by broadening the tax base—specifically, by eliminating exemptions and reduced rates.

Currently, VAT-based resources account for only about 9.5 percent of the EU’s total revenue, down from 60 percent in 1988. This decline reflects reforms to the own resources system that reduced both the VAT base and the applicable rate.

There is significant untapped potential. Estimates suggest that broadening the VAT base—by eliminating reduced rates and exemptions—could generate up to €773 billion in additional national revenue. Even a small share of this would exceed what DSTs could deliver. Since each Member State’s VAT revenue determines the base for the EU’s own resources, this €773 billion could translate into roughly €2.3 billion for the EU budget—slightly above the lower-end estimate of €1.3 billion from an EU-wide DST.

Additionally, if the VAT base cap is non-binding (and the new own resources framework plans to increase the current cap), raising the call rate from 0.3 percent to its previous level of 1 percent could generate an additional €7.7 billion in stable funding, without the economic distortions and trade tensions associated with DSTs.

Conclusion

DSTs address a real concern—the need to adapt taxation to the digital economy—but they are not the right solution. They raise limited revenue, are often passed on to consumers rather than large digital firms, create economic distortions, increase complexity and compliance costs, negatively impact innovation and competitiveness, and risk international retaliation.

By contrast, VAT is already suited to the digital age, generates significantly more revenue, and is more efficient, neutral, and stable.

Rather than expanding DSTs or introducing an EU-wide version, policymakers should focus on strengthening and modernizing VAT. As in all public policy, tax design should aim to raise revenue efficiently, fairly, and with minimal economic harm—and DSTs fall short on all three counts.

See Related Research

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

References

[1] Alan Cole, “Tariffs by Another Name: How Discriminatory Taxes on Cross-Border Services Threaten America’s Export Edge,” Tax Foundation, Apr. 15, 2026, https://taxfoundation.org/research/all/global/tariffs-discriminatory-cross-border-services-taxes/.

[2] Back in 2018, the European Economic and Social Committee (EESC) already warned that an EU-wide DST could shift resources toward larger Member States, weakening Single Market cohesion. The EESC also stressed the need to account for the significantly higher taxation of US digital firms operating in the EU following changes to the US tax code. Several countries, including Finland, Sweden, and Denmark, also opposed them due to concerns about their impact on innovation and competitiveness.

")

{kind=link}