AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $11.74 (+4.9%)

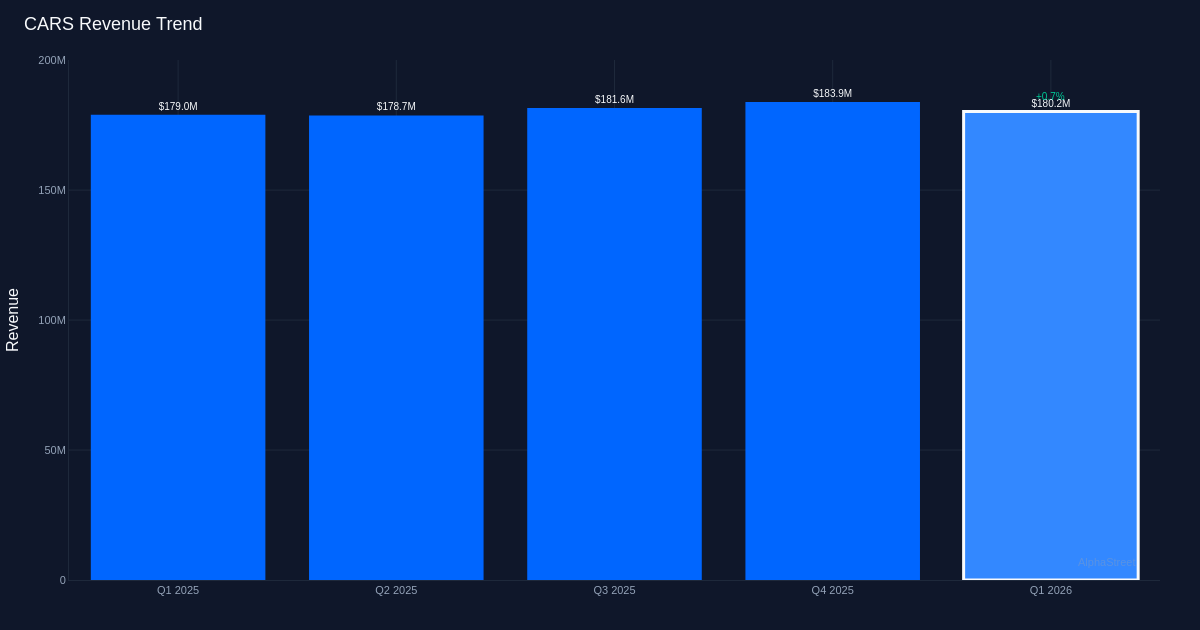

Strong beat. Cars.com Inc. (NYSE: CARS) delivered a standout performance in Q1 2026, with adjusted earnings of $0.45 per share crushing the consensus estimate of $0.13 by 246.2%. The digital automotive marketplace generated $180.2M in revenue for the quarter, representing a 1.0% increase from the $179.0M recorded in Q1 2025, while adjusted profit came in at $26.7M. The remarkable earnings beat signals strong operational leverage as the company extracted significantly more profit from modest top-line growth.

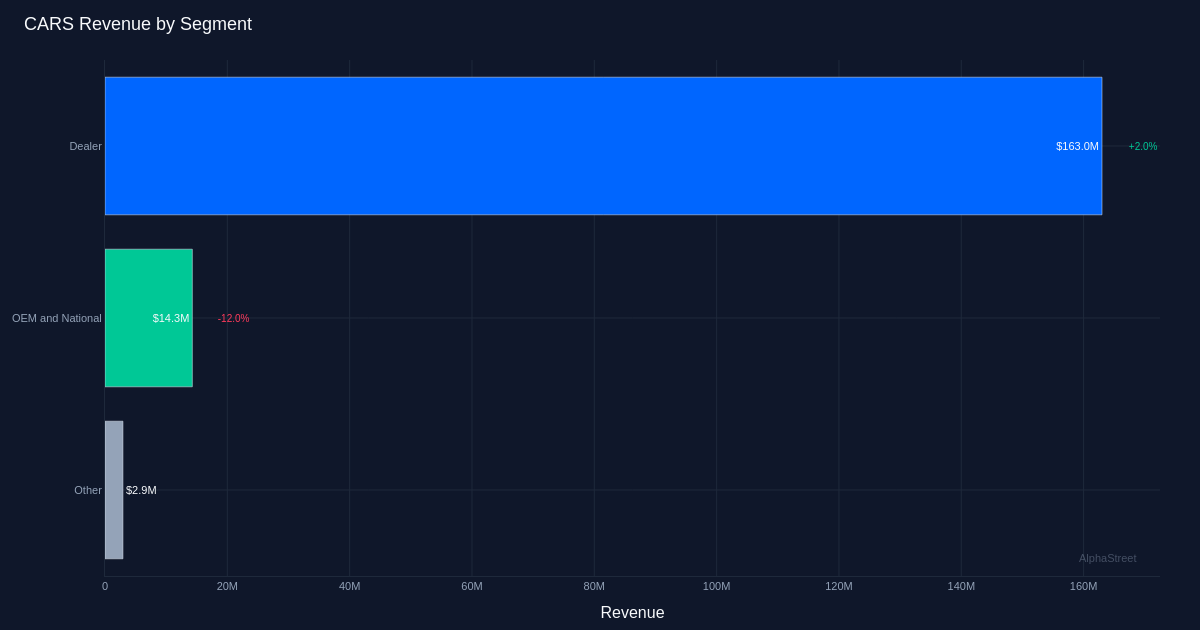

Dealer strength continues. The company’s core Dealer segment led performance with $163.0M in revenue, up 2.0% year-over-year, demonstrating resilient demand despite challenging automotive market conditions. Cars.com maintained 19,390 Dealer Customers at quarter end, providing a stable foundation for recurring revenue. Average Monthly Unique Visitors reached 25.8 million for the quarter, reflecting sustained engagement on the platform as consumers continue to rely on digital channels for vehicle research and purchasing decisions.

Quality of beat. The massive earnings upside appears driven by margin expansion rather than purely revenue outperformance, given that revenue grew just 1.0% while earnings exceeded expectations by more than double. This suggests the company successfully controlled costs and improved operational efficiency, though investors typically favor revenue-driven beats that signal stronger demand dynamics. The ability to generate $26.7M in adjusted net income on relatively flat revenue growth does demonstrate management’s execution on profitability initiatives, but sustained earnings power will require accelerating top-line momentum in an industry facing inventory constraints and shifting consumer preferences.

Market reaction positive. Shares of CARS jumped 4.9% to $11.74 following the results, as the market rewarded the significant earnings surprise despite the modest revenue growth. The stock’s advance reflects investor confidence in management’s ability to drive profitability improvements and navigate the evolving digital automotive landscape. Wall Street consensus currently stands at 5 buy, 3 hold, and 1 sell ratings, suggesting a constructive but not unanimously bullish view on the name.

Positioning in flux. As an Internet Content & Information provider serving the automotive vertical, Cars.com faces both opportunities and challenges from the industry’s digital transformation. The company’s ability to maintain dealer relationships while adapting to changing consumer behavior and competitive pressures from both traditional players and emerging platforms will determine its trajectory through 2026.

What to Watch: Management’s ability to convert margin expansion into sustainable earnings growth while reaccelerating revenue will be critical. Investors should monitor dealer customer retention trends and whether traffic metrics can translate into improved monetization as automotive inventory conditions normalize.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}