Published on May 14th, 2026 by Felix Martinez

Tamarack Valley Energy (TNEYF) has two appealing investment characteristics:

#1: It is offering an above-average dividend yield of 1.3%, which is roughly the average dividend yield of the S&P 500.#2: It pays dividends monthly instead of quarterly.Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

Tamarack Valley Energy’s combination of an above-average dividend yield and a monthly dividend makes it an attractive option for individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about Tamarack Valley Energy.

Business Overview

Tamarack Valley Energy engages in the acquisition, exploration, development, and production of oil, natural gas, and natural gas liquids in the Western Canadian Sedimentary Basin. Its oil and natural gas properties are the Cardium, Clearwater, Charlie Lake, and Enhanced Oil Recovery assets located in the province of Alberta, Canada.

The company was formerly known as Tango Energy and changed its name to Tamarack Valley Energy in June 2010. Tamarack Valley Energy was formed in 2002 and is headquartered in Calgary, Canada.

As an oil and gas producer, Tamarack Valley Energy is highly cyclical due to the dramatic fluctuations in oil and gas prices. The company produces liquids and gases in an approximate 85/15 ratio and is highly sensitive to fluctuations in oil prices. It has reported losses in 6 of the last 10 years and initiated a dividend only at the beginning of 2022.

On the other hand, Tamarack Valley Energy has several advantages compared to well-known oil and gas producers. Most oil and gas producers have been struggling to replenish their reserves due to the natural decline of their producing wells.

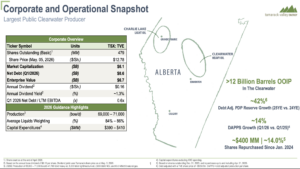

Source: Investor Presentation

Tamarack reported strong first-quarter 2026 results, supported by continued growth in its Clearwater operations. Average production increased 5% year over year to 71,329 barrels of oil equivalent per day, while Clearwater production rose 19% to 53,016 barrels per day.

The company generated $443.9 million in oil and gas sales, $221.8 million in adjusted funds flow, and $128.1 million in free funds flow, highlighting the strength of its low-cost asset base.

Tamarack invested $93.5 million during the quarter, primarily to drill 24 Clearwater wells and four Charlie Lake wells and to expand its waterflood program. These investments continue to improve recovery rates and support future production growth.

The company also strengthened its balance sheet, reducing net debt to $622.7 million, down 19% from the prior year.

Tamarack returned $66.3 million to shareholders through dividends and share repurchases, including the buyback of 4.6 million shares. Since January 2024, the company has reduced its share count by 13.4%.

Management reaffirmed its 2026 production guidance of 69,000 to 71,000 barrels of oil equivalent per day and capital spending of $390 million to $410 million. Overall, Tamarack remains well-positioned to generate strong free cash flow and continue delivering meaningful shareholder returns.

Growth Prospects

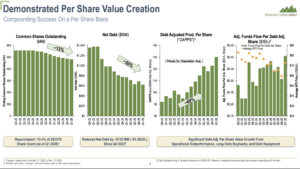

Tamarack Valley Energy has posted one of the highest reserve growth rates among its peers in recent years. Even better, the company has ample room for future growth.

Source: Investor Presentation

Exceptionally high returns characterize the reserves in this area. It is thus evident that Tamarack Valley Energy has a significant competitive advantage over its peers.

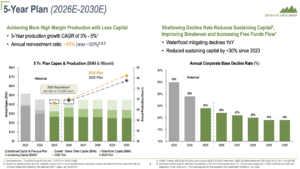

Moreover, the company has a promising 5-year growth plan:

Source: Investor Presentation

It expects to grow its production at an average annual rate of 3%-5% and approximately double its free funds flow per share over the next five years, partly thanks to material share repurchases. None of the well-known oil majors has such an ambitious growth plan.

On the other hand, as an oil and gas producer, Tamarack Valley Energy is highly sensitive to the fluctuations in oil and gas prices.

Given the promising growth plan of Tamarack Valley Energy, as well as the highly cyclical nature of the oil and gas industry, we expect the earnings per share of Tamarack Valley Energy to increase significantly this year to $0.45 per share from a negative $0.06 per share in 2026

Dividend & Valuation Analysis

Tamarack Valley Energy is currently offering an above-average dividend yield of 1.3%, about the same as the S&P 500’s yield. The stock is an interesting candidate, but they should be aware that the dividend is far from safe given the dramatic price cycles in oil and gas.

Tamarack Valley Energy has a reasonable payout ratio of 27%. Additionally, the company maintains a solid financial position.

Moreover, it is critical to note that Tamarack Valley Energy initiated a dividend only in 2022, amid multi-year high commodity prices. It failed to pay dividends in the preceding years because it incurred material losses in most of those years. Therefore, it is evident that the company’s dividend is far from safe.

In reference to the valuation, Tamarack Valley Energy is currently trading for 20 times its expected earnings per share this year. Given the company’s high cyclicality, we assume a fair price-to-earnings ratio of 11, which is typical for mid-cycle valuations of oil and gas producers.

Therefore, the current earnings multiple is much higher than our assumed fair price-to-earnings ratio. If the stock trades at its fair value in five years, it will compress a -10% annualized return.

Taking into account the 0% annual growth of earnings per share, the 1.3% current dividend yield, and a 10% annualized headwind of valuation level, Tamarack Valley Energy could offer a -8.7% average annual negative total return over the next five years.

The expected return signals that the stock is a bad long-term investment.

Final Thoughts

Tamarack Valley Energy has been thriving since early 2022, thanks to an ideal environment of above-average oil prices. The stock offers an above-average dividend yield of 1.3% and a decent payout ratio of 27%.

However, the company has proven highly vulnerable to fluctuations in oil prices. As this price appears to have passed its peak for good, the stock is currently highly risky.

Moreover, Tamarack Valley Energy is characterized by low trading volume. This means that it is hard to establish or sell a large position in this stock.

Additional Reading

Don’t miss the resources below for more monthly dividend stock investing research:

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}