– Is there a doctor in the house?")

MPW has been under fire by short-sellers. Is it sick? We don’t think so.

It is critical for an investor in hospital real estate (MPW is a basically a hospital REIT) to understand the value that a specific facility has to the healthcare needs of the community it serves. Said differently, if people need medical services, they usually don’t shop but go to the local health care facility regardless of who runs it. At the same time, it doesn’t mean you should not invest in a hospital REIT just because the goals and periodic performance of one particular operator are not met in a certain location. For us, MPW is about location and the value of real estate that is zone and built up for medical uses. If you buy MPW low and sell high, we believe a real estate investor can enjoy attractive, well underwritten returns.

MPW has made some mistakes. It has had poor communication related to a hospital operator (a customer) who filed Chapter 11. They have some other troubled customers as well. MPW has had some Board turnover. MPW has even had legal issues (that were fully resolved 100% in the company’s favor). And just because short sellers have started a campaign against the management team accusing them of malfeasance, it does not at all mean that when a CEO invests in a partnership that does business with a customer or company he runs, it always should make investors run-away.

Let us stick with facts. MPW has a tremendous history of growth and generating cash flows. It has built up a somewhat diversified global platform with 438 properties in the U.S, Australia, Germany and the UK, among other countries.

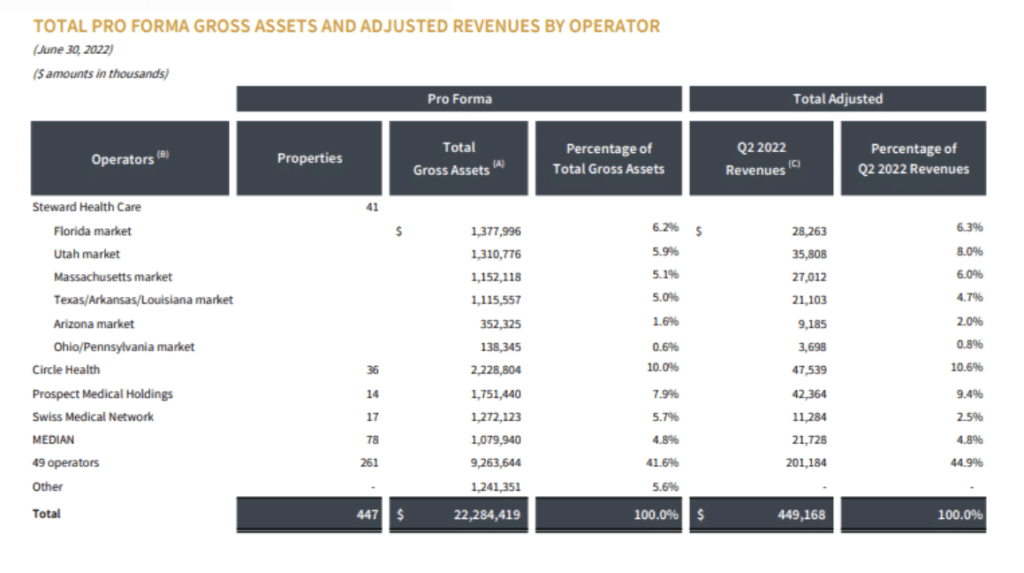

They do have a large customer in Steward Health Care – but that customer has multiple markets.

Steward Health Care is undergoing some financial stress as it recovers from various issues including the strain on expenses due to the Coronavirus.

Here is our view:

MPT currently has a $2 billion revolving credit facility with extension options to June 2026. It has various short-term debt due —400 million pound sterling in December 2023 and then in 2024 – a $750 million term loan due (that was used to acquire a portfolio in Australia). It seems to us that refinancing hospital secured debt should not be a problem. Albeit -there maybe some higher interest rates as compared to historical levels. Debt to leverage ratio is higher —somewhere around 7 to 9x EBITDA depending on how you calculate. We think about leverage here like buying a house. If an individual home owner purchases a single family home and puts 20% down, 80% of it is funded by debt. On a single property, that is high – but that is where diversification comes into play.

Although Steward Capital is a large customer – roughly 25% of total assets – those assets are held in multiple markets – the largest of which is in Florida at 6.5%.

MPT continues to generate cash. Cash funds from operations (FFO) for this year is expected to be around $1.80. With the stock around $11 (at the time we write this research brief) that is a double-digit or 15% FFO ratio.

But clearly, MPT is not in a growth mode now due to high interest rates.

We believe it has a long-standing, consistent and successful business model has always been to invest in hospital real estate that regardless of the operator is underwritten to generate sustainable, long-term cash rental revenue. The key investment criteria for this success is acquisition of real estate that is critical to the delivery of hospital services in any particular community. We believe it is a mistake for real estate investors or analysts to assess hospital value based primarily on periodically volatile operating results instead of the important characteristics of the underlying real estate.

Hospitals will pay rent through economic volatility, Obamacare, the Affordable Care Act, and continuing disruptions, uncertainties and the aftereffects, three years of an unprecedented global pandemic that included virtually closing many hospitals for months. With higher interest rates on the horizon, new investments will be scarce – and the dividend yield payout may have to be reduced.

Are there some issues? Sure. However, with the stock down almost 50% in the past year and trading down 17% over the past 5 years, we believe such risk is priced in.

________________

About Us

The Independent Adviser Corporation is a 100% Independent and 100% Objective Financial Advisory Firm that provides buy-side investment research. We do not underwrite corporate securities, nor do we sell any proprietary products. Our network of independent Fee-Only advisers serves individuals, families and businesses. They can provide financial planning services, professionally managed asset accounts, tax and legal services.

What are you waiting for? To find out more or get a FREE consultation Ask TheAdviser.com or visit 1800ADVISER.com and get connected to a Fee-Only adviser in your local area.

{kind=link}