Introduction

Over the last few years, concerns have been raised that the existing international taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. system does not properly capture the digitalization of the economy. Under current international tax rules, multinationals generally pay corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. where production occurs rather than where consumers—or, specifically for the digital sector, users—are located. However, proponents of new taxes on digital multinationals argue that through the digital economy, businesses (implicitly) derive income from users abroad but, without a physical presence, are not subject to corporate income tax in that foreign country.

To address these concerns, the Organisation for Economic Co-operation and Development (OECD) has been hosting negotiations with more than 140 countries to adapt the international tax system.[1] The proposal,[2] referred to as Pillar One,[3] would require some of the world’s largest multinational businesses to pay some of their income taxes where their consumers are located.

Pillar One would replace some existing norms for taxing multinationals and create a multilateral standard to replace the patchwork of unilateral policies that countries have put in place to tax digital companies in recent years. The most common form is a digital services tax (DST), which is a tax on selected gross revenue streams of large digital companies.

Because Pillar One is focused on changing where profits are taxed, including for many large digital companies, DSTs are expected to be repealed. While the OECD hasn’t completely dropped Pillar One,[4] the negotiations have failed to result in an agreement that would eliminate DSTs.

Digital Services Taxes Around the World

Over the last eight years, jurisdictions around the world have announced, proposed, and implemented DSTs. First proposed as an EU-wide tax, DSTs are now unilateral measures found on every continent.

EU Proposal for a DST

In March 2018, the European Commission put forth a proposal to establish rules that allow for corporate taxation of businesses with a significant digital presence.[5] While this was the long-term objective of the proposal, it also proposed a DST that would have been implemented as an interim measure until the significant digital presence rules were put in place.[6]

The EU’s DST would be a 3 percent tax on revenues from digital advertising, online marketplaces, and sales of user data generated in the EU. Businesses are in scope if their annual global revenues exceed €750 million and EU revenues exceed €50 million. The tax was estimated to generate between €1.3 billion[7] and €5 billion[8] annually for EU Member States, translating to 0.07 percent of total tax revenues collected in the EU in 2024.[9]

The European Commission was unable to find the necessary unanimous support for the proposal to be adopted.

UN Model Convention

At the same time, the United Nations has added special provisions for income from automated digital services to the UN Model Tax Convention (see Article 12B),[10] which would apply to treaty parties that agree to its inclusion. Additionally, the terms of reference approved in November 2024 commit the UN to begin talks on a treaty to enhance tax cooperation and wrap up negotiations by 2027.[11]

Unilateral DSTs

Since the EU was unable to find the necessary unanimous support to reach an agreement on an EU-wide DST, several European countries have decided to move forward with DSTs unilaterally. While each country’s DST is unique in its design, most have adopted several elements from the EU’s DST proposal.

Currently, about half of all European OECD countries have either announced, proposed, or implemented a DST.

Austria, Denmark, France, Hungary, Italy, Poland, Portugal, Spain, Turkey, and the United Kingdom have implemented a DST. Belgium, the Czech Republic, Germany, Latvia, Norway, Slovakia, and Slovenia have either officially announced or considered implementing such a tax.[12]

The proposed and implemented DSTs differ significantly in their structure. For example, while Austria and Hungary only tax revenues from online advertising (to similarly tax online and offline advertising) and Denmark’s DST applies only to streaming services, France’s tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. is much broader, including revenues from the provision of a digital interface, targeted advertising, and the transmission of data collected about users for advertising purposes. The tax rates range from 1.5 percent in Poland to 7.5 percent in both Hungary and Turkey (although Hungary’s tax rate has been permanently reduced to 0 percent, and Turkey reduced it to 5 percent starting January 1, 2026).

Economic Incidence of DSTs

The economic incidence of a DST is closer in nature to an excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. than to a corporate income tax.[13] While the economic literature shows that the corporate income tax is largely borne by shareholders—with shareholder income disproportionately concentrated among higher-income households—excise taxes are usually borne by consumers through higher prices. As lower-income individuals consume a larger share of their income, excise taxes tend to be rather regressive.

The exact equity effects of a DST, however, depend on the ability to pass the tax on to consumers, the type of goods and services sold, and consumers’ responsiveness to the tax.[14] Evidence shows that some companies targeted by DSTs have passed the tax on to users.[15] Apple, Amazon, and Google (now Alphabet) passed on the UK’s 2 percent DST tax.[16] Google has a page explaining that a charge for the DST is added on in countries where ads are accessed.[17] Additionally, a recent research paper by economists Dominika Langenmayr and Rohit Reddy Muddasani shows that the attempt to target big digital platforms misses the mark, as the cost mostly falls on European consumers.[18]

Retaliatory Measures

DSTs, which function like tariffs on certain services, are designed to be discriminatory; they target specific industries dominated by US companies. The US government has voiced opposition to DSTs over the last decade, with President Trump using Section 301 investigations in his first term, and, more recently, the US Congress threatening the Section 899 retaliatory tax. While section 899 was removed from the One Big Beautiful Bill Act, the issue of DSTs remains contentious.[19] Until a true consensus is found on how to handle the taxation of the digital economy, escalating retaliatory measures will harm all parties involved.

DSTs and Their Design Issues

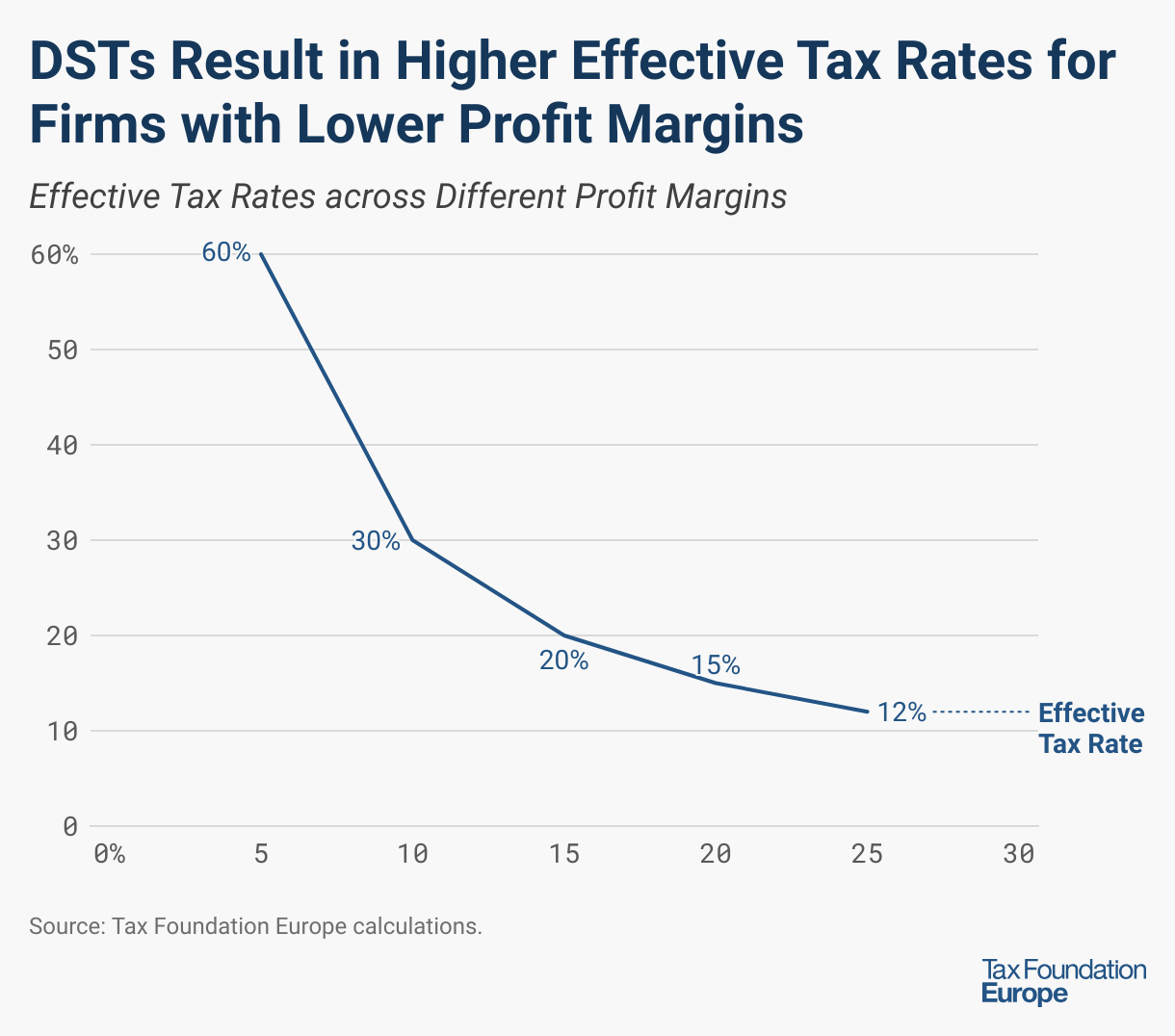

Unlike corporate income taxes, DSTs are levied on revenues rather than profits. This means that the tax will be owed regardless of whether a particular digital service is profitable in the jurisdiction levying the tax. Historically, European countries have turned away from these types of turnover taxes because even low tax rates can translate into high effective tax burdens.[20] For example, if a company has €100 in revenue and €85 in costs, it will earn €15 in profit. If a 3 percent DST is applied to that revenue, the company would owe €3 in tax (3 percent of €100 in revenue). For this company, a 3 percent tax on revenue equals a 20 percent tax on profits (3 percent of €15). Figure 2 shows how different profit margins for that same company earning €100 in revenue relate to different effective tax rates. If that company only earned a 5 percent profit margin, the effective tax rate with a 3 percent DST would be 60 percent. With a 25 percent profit margin, the effective tax rate falls to 12 percent.

This leads to a disproportionate tax burden being placed on companies with lower profit margins—the less profitable a company is, the higher its effective tax rate becomes. DST tax bases relate poorly to profits, cash flow, or ability to pay.

Turnover taxes, like DSTs, can apply multiple times over the supply chain as there is no built-in credit system for already paid taxes, unlike in the case of value-added taxes (VATs). Such tax pyramiding can distort economic activity and magnify effective tax rates.[21] Unlike VATs, turnover taxes also do not exempt business inputs. DSTs may tax business inputs, such as advertising and cloud computing.

In addition, DSTs, as proposed by the European Commission and adopted by certain Member States, are discriminatory with respect to company size. The revenue thresholds result in the tax only being applied to large multinationals. While this can ease the overall administrative burden, it also provides a relative advantage for businesses below the threshold and creates an incentive for businesses operating near the threshold to alter their behavior. Because these thresholds aren’t adjusted for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin, more firms will likely fall within their scope over time. Likewise, digital businesses are at a relative disadvantage compared to non-digital businesses operating in a similar field.

The introduction of a DST also creates new administrative and compliance costs. Governments must provide detailed guidelines on how the tax is calculated and remitted, and then administer and enforce it. At the same time, businesses are required to identify the location of users and determine their taxable base. Since not all DSTs are equally designed and administered, businesses have even higher compliance costs due to challenges of dealing with those differences. Because of the issues outlined above and to enhance the functioning of the European cross-border market, Europe replaced its turnover taxes with VATs in the 1960s.[22] The emergence of DSTs reintroduces the negative economic consequences of turnover taxes—a step back in terms of sound tax policy.

Back in 2018, the European Economic and Social Committee (EESC) raised concerns about the DSTs’ risk of reallocating resources in favor of larger Member States while disadvantaging smaller ones, potentially weakening cohesion within the Single Market.[23] DSTs also faced opposition from several Member States, including Finland, Sweden, and Denmark, which expressed concerns about potential negative impacts on innovation and competitiveness.[24]

Revenue Impact

Regardless of their economic incidence, design issues, and retaliatory measures, many European governments are seeking to increase revenue. DST revenue in Austria, France, Italy, Spain, Turkey, and the UK ranged from €137 million (Austria) to €1.04 billion (the UK) in the most recent year revenue was reported. Austria’s DST is much narrower than the others in the sample because it applies only to digital advertising. In all cases, the amounts raised are less than one percent of the country’s general revenue. Turkey’s DST brings in the most at 0.24 percent of total government revenues. The UK is around 0.1 percent, and in countries like Italy, France, Austria, and Spain, it’s even smaller—between 0.05 and 0.07 percent.

Table 1. Recent Revenue Raised from Selected Digital Services Taxes

Note: These countries have been selected because they report digital services tax revenue separately as a line item.Source: Tax Foundation Europe analysis of national budget documents and announcements.

Policy Alternatives and Conclusions

If the objective is to raise more money from digital services, then the EU should incentivize Member States to continue reforming the value-added tax to effectively tax these services at the point of consumption. Digital services are often implicitly included in the VAT base. Additionally, VAT has already been modified in recent years to account for the digitalization of the economy. The reforms require non-EU businesses to register and remit VAT in the Member State of the consumer, effectively taxing digital services at the point of consumption. The EU VAT revenues collected from these measures increased tenfold, from €3 billion in 2015, €4.5 billion in 2018, and €20 billion in 2022,[25] to more than €33 billion in 2024.[26] This latest figure is about seven times higher than the upper-end revenue estimate for an EU-wide DST. Expanding VAT to include all digital services would allow Member States to eliminate their DSTs.

If the goal is to increase funding for the EU budget, the focus should not be on creating new own resources but on encouraging Member States to strengthen VAT collection. In addition to being an important source of revenue for EU countries, VAT revenue is also one of the EU’s own resources. However, the share of VAT-based resources accounted for only 9.5 percent of the EU’s total revenue in 2024, down from 60 percent in 1988.[27] This decline is due to own resources policy reforms that reduced both the VAT base and the VAT rate.[28] Since the VAT revenue collected by each Member State determines the VAT base for own resources, broadening the VAT tax base by eliminating reduced rates and exemptions would not only positively impact EU countries’ VAT revenues but could also contribute to the EU’s sources of revenue.[29] Closing the VAT system’s gaps would reinforce VAT as an important and stable revenue source for the EU budget. Broadening the VAT tax base would bring in additional revenue for Member States of up to €773 billion, four times the EU 2026 Budget. Even without changing the current rules for VAT-based contributions from Member States, the €773 billion in additional national revenue would translate into roughly €2.3 billion for the EU budget, slightly above the lower-end estimate of €1.3 billion for an EU-wide DST.[30] Finally, VAT causes fewer distortions in the economy, is trade-neutral, and does not discriminate between firms.[31]

Since DSTs generate little revenue, place the cost on European consumers and not on large digital companies as intended, and risk escalating trade disputes, policymakers should rethink their strategy. Instead of expanding DSTs or pursuing an EU-wide version, they ought to abolish them entirely. Tax policy should be grounded in sound principles—simplicity, transparency, neutrality, and stability—to ensure it can withstand the challenges posed by the rapidly evolving economic and technological landscape of the 21st century. The primary aim of tax policy is to raise revenue efficiently, and there are more effective ways to do so.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

Appendix

Table 1. Announced, Proposed, and Implemented Digital Services Taxes, as of May 2026

CountryTax RateScopeGlobal Revenue ThresholdDomestic Revenue ThresholdStatus

Austria (AT)5%Online advertisingEUR 750 millionEUR 25 millionImplemented (Effective from January 1, 2020); joined statement on October 21, 2021, that repeal of the DST would be contingent on Pillar One implementation.

Belgium (BE)3%· Selling of user dataEUR 750 millionEUR 5 millionProposed (A DST was first introduced in January 2019 but was rejected in March 2019; an adjusted DST proposal was reintroduced in June 2020. On January 31, 2025, five Belgian political parties agreed on a coalition program outlining their position on a DST. On April 17, 2026, the Chamber of Representatives accepted for consideration a bill proposing the introduction of a DST). Expected to enter into force on Jan 1, 2027.

· Selling advertising space on a digital platform

· Digital intermediation services facilitating the exchange of supplies of goods or services

Czech Republic (CZ)5%· Online advertisingEUR 750 millionCZK 100 million (EUR 4.13 million)Proposed/Stalled (There was a proposed amendment to reduce the tax rate from 7% to 5%. However, the discussion on the bill has stalled and there is support for a DST solution at the OECD level).

· Transmission of user data

· Digital interface to facilitate the provision of supplies of goods and services among users

Denmark (DK)2% (3% surcharge)On-demand, audio-visual media service providersDKK 15 million (EUR 2.01 million) or audience constituting more than 1% of the total number of users of streaming services in Denmark.Implemented (Effective from January 1, 2024. There is an additional 3% surcharge for companies that invest less than 5% of their Danish revenues in Danish content. On May 20, 2024, Denmark introduced a revised version of its DST).

Finland (FI)The Finance Ministers of Denmark, Finland, and Sweden released a joint statement on digital tax, indicating that the digital and traditional economy should be taxed where value is created, and any solution reached should be a consensus-based OECD solution.

France (FR)3%· Provision of a digital interfaceEUR 750 millionEUR 25 millionImplemented (Retroactively applicable as of January 1, 2019. The 2020 DST collection was delayed to the end of 2020. On September 12, 2025, the French Constitutional Council upheld France’s DST as constitutional. On November 24, 2025, the National Assembly voted against the 2026 Finance Bill that would have increased the DST rate from 3% to 6%); joined statement on October 21, 2021, that repeal of the DST would be contingent on Pillar One implementation.

· Advertising services based on users’ data

1.2%Paid and free access to recorded music and online music videosEUR 20 millionImplemented (January 1, 2024. Due on amounts exceeding EUR 20 million).

Germany10%Advertising revenueAnnounced/Considered (On June 3, 2025, Germany considered a 10% digital advertising tax).

Hungary (HU)7.5% (effective rate 0%)Advertising revenueHUF 100 million (EUR 281,300)Implemented (Effective from July 1, 2019. As a temporary measure, the advertisement tax rate has been reduced to 0%, effective from July 1, 2019. In May 2026, the 0% rate was embedded in a parliamentary act, keeping the advertising tax rate at 0% from July 1, 2026 onwards).

Italy (IT)3%· Advertising on a digital interfaceImplemented (Effective from January 1, 2020. In November 2022; on October 15, 2024, the Italian government approved the draft 2025 Budget Law, which eliminated from January 2025 the revenue thresholds, which required companies to have worldwide revenues of at least EUR 750 million and at least EUR 5.5 million from digital services in Italy to be liable for DST). Joined statement on October 21, 2021, that repeal of the DST would be contingent on Pillar One implementation. On March 20, 2024, the Italian Economy Minister announced that Italy might retain and modify its DST if Pillar One is not implemented.

· Multilateral digital interface that allows users to buy/sell goods and services

· Transmission of user data generated from using a digital interface

Latvia (LV)3%—Announced/Shows Intention (The Latvian government commissioned a study to determine the increase of tax revenue based on the assumption that the country levies a 3% DST. However, no further action has been taken for now).

Netherlands (NL)On October 24, 2023, the Dutch State Secretary wrote to the Dutch Parliament saying that an EU DST should be considered as an alternative to the OECD’s Pillar One, Amount A if a global agreement is not reached.

Norway (NO)—-Announced/Shows Intention (Norway plans to introduce a unilateral measure if the OECD does not reach a consensus solution; no announcements since the inclusive framework agreement).

Poland (PL)1.5%Audiovisual media service and audiovisual commercial communication–Implemented (Effective from July 2020; there is a separate proposal to introduce a 7% levy on digital sector enterprises with a significant digital presence in the territory of Poland. Additionally, a 5% levy on advertisement revenues is also discussed).

3%Digital advertisements, multilateral digital interfaces, and monetization of user data.EUR 1 billionPLN 25 million (EUR 5.9 million)Proposed (On January 27, 2026, the Polish Ministry of Digital Affairs announced its submission of a draft bill proposing a compensatory tax on certain digital services. The tax rate would be capped at 3% of revenue from specified services, reduced by corporate income tax owed).

Portugal (PT)4%, 1%Audiovisual commercial communication on video-sharing platforms (4%), subscriptions for video-on-demand services (1%)Implemented (Effective from February 2021).

Slovakia (SK)–Announced/Shows Intention (The Ministry of Finance opened a consultation on a proposal to introduce a DST on revenue of nonresidents from provision of services such as advertising, online platforms, and sale of user data. On August 18, 2025, Slovakia’s Ministry of Investments proposed introducing a DST that would remain in effect until a multilateral agreement under Pillar One is reached).

Slovenia (SI)—-Announced/Shows Intention (The Ministry of Finance announced a government proposal to submit a draft bill to the National Assembly introducing a digital services tax by April 1, 2020; however, there has been no development so far).

Spain (ES)3%· Online advertising servicesEUR 750 millionEUR 3 millionImplemented (Effective from January 16, 2021); joined statement on October 21, 2021, that repeal of the DST would be contingent on Pillar One implementation.

· Sale of online advertising

· Sale of user data

Sweden (SE)The Finance Ministers of Denmark, Finland, and Sweden released a joint statement on digital tax, indicating that the digital and traditional economy should be taxed where value is created, and any solution reached should be a consensus-based OECD solution.

Turkey (TR)5%Online services, including advertisements, sales of content, and paid services on social media websitesEUR 750 millionTRY 20 million (EUR 376,000 )Implemented (Effective from March 1, 2020; the president can reduce the DST rate as low as 1% or increase it as much as 15%. The rate was 7.5% until December 31, 2025, 5% in 2026, and will be 2.5% beginning January 1, 2027); agreed to same terms of the joint statement on October 21, 2021, that repeal of the DST would be contingent on Pillar One implementation.

United Kingdom (GB)2%· Social media platformsGBP 500 million (EUR 579 million)GBP 25 million (EUR 29 million)Implemented (Retroactively applicable as of April 1, 2020); joined statement on October 21, 2021, that repeal of the DST would be contingent on Pillar One implementation. The UK Treasury agreed to develop a contingency plan if the country’s DST needs to be extended beyond 2025. Since Pillar One has not yet been implemented, the DST remains as an interim measure.

· Internet search engine

· Online marketplace

Note: Current exchange rates were used. Source: KPMG, “Taxation of the digitalized economy: Developments summary,” last updated May 29, 2026, https://kpmg.com/kpmg-us/content/dam/kpmg/pdf/2023/digitalized-economy-taxation-developments-summary.pdf.

References

[1] OECD, “Members of the OECD/G20 Inclusive Framework on BEPS,” Dec. 5, 2025, https://www.oecd.org/content/dam/oecd/en/topics/policy-issues/beps/inclusive-framework-on-beps-composition.pdf.

[2] OECD, “Pillar One Update from the Co-Chairs of the Inclusive Framework on BEPS,” Jan. 13, 2025, https://www.oecd.org/content/dam/oecd/en/topics/policy-issues/beps/pillar-one-update-co-chair-statement-inclusive-framework-on-beps-january-2025.pdf.

[3] Daniel Bunn and Sean Bray, “The Latest on the Global Tax Agreement,” Tax Foundation, Aug. 15, 2025, https://taxfoundation.org/blog/global-tax-agreement/.

[4] OECD, “Statement by the OECD/G20 Inclusive Framework on BEPS,” Apr. 11, 2025, https://www.oecd.org/content/dam/oecd/en/topics/policy-issues/beps/statement-oecd-g20-inclusive-framework-on-beps-april-2025.pdf.

[5] European Commission, “Fair Taxation of the Digital Economy,” Taxation and Customs Union – European Commission, Mar. 21, 2018, https://ec.europa.eu/taxation_customs/business/company-tax/fair-taxation-digital-economy_en.

[6] European Commission, “Proposal for a Council Directive on the Common System of a Digital Services Tax on Revenues Resulting from the Provision of Certain Digital Services,” Mar. 21, 2018, https://taxation-customs.ec.europa.eu/system/files/2018-03/proposal_common_system_digital_services_tax_21032018_en.pdf.

[7] European Parliament, “Mapping of Existing, Proposed and Potential Own Resources as Well as Other Revenue Sources,” Jan. 27, 2026, https://www.europarl.europa.eu/RegData/etudes/BRIE/2026/783556/BUDG_BRI(2026)783556_EN.pdf.

[8] European Parliament, “Interim digital services tax on revenues from certain digital services,” December 2018, https://www.europarl.europa.eu/RegData/etudes/BRIE/2018/625132/EPRS_BRI(2018)625132_EN.pdf.

[9] Total tax revenue data covers the EU-27 and is based on Eurostat data. See Eurostat, “Main National Accounts Tax Aggregates,” Apr. 27, 2026, https://ec.europa.eu/eurostat/databrowser/view/gov_10a_taxag/default/table?lang=en.

[10] United Nations, “UN Model Double TaxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. Convention between Developed and Developing Countries 2021,” Department of Economic and Social Affairs, May 2023, https://financing.desa.un.org/sites/default/files/2023-05/UN%20Model_2021.pdf; United Nations “Tax Consequences of Digitalized Economy,” consulted May 29, 2026, https://financing.desa.un.org/what-we-do/ECOSOC/tax-committee/thematic-areas/tax-consequences-digitalized-economy.

[11] James Munson, “UN Approves Roadmap for Tax Treaty Talks, 2027 Deadline,” Bloomberg Tax, Nov. 27, 2024, https://news.bloombergtax.com/daily-tax-report/un-approves-roadmap-for-tax-treaty-talks-2027-deadline.

[12] A summary of all announced, proposed, and implemented DSTs can be found in Table 1 of the Appendix.

[13] Jane G. Gravelle, “The OECD/G20 Pillar 1 and Digital Services Taxes: A Comparison,” Congressional Research Service, Apr. 1, 2024, https://crsreports.congress.gov/product/pdf/R/R47988.

[14] Ibid.

[15] This happens through higher advertising fees or higher seller fees. As a result, the tax burden is shifted to small businesses that rely on large platforms to reach customers and, indirectly, consumers through higher prices.

[16] Mark Sweney, “UK’s Digital Services Tax Reaps Almost £360m From US Tech Giants in First Year,” The Guardian, Nov. 22, 2022, https://www.theguardian.com/technology/2022/nov/23/uks-digital-services-tax-reaps-almost-360m-from-us-tech-giants-in-first-year.

[17] Google Ads, “Jurisdiction-Specific Surcharges,” https://support.google.com/google-ads/answer/9750227.

[18] Dominika Langenmayr and Rohit Reddy Muddasani, “Navigating the Amazon: The Incidence of Digital Service Taxes,” CESifo Working Paper, Jun. 12, 2025, https://storage.e.jimdo.com/file/b2f10b20-f37c-4d9b-8d16-d86f91b1b04f/2025_05%20DST.pdf.

[19] Alan Cole and Patrick Dunn, “Reviewing the International Tax Provisions in the One Big Beautiful Bill Act,” Tax Foundation, Aug. 6, 2025, https://taxfoundation.org/blog/big-beautiful-bill-international-tax-changes/.

[20] European Commission, “Impact Assessment Accompanying the Document Proposal for a Council Directive Laying Down Rules Relating to the Corporate Taxation of a Significant Digital Presence and Proposal for a Council Directive on the Common System of a Digital Services Tax on Revenues Resulting from the Provision of Certain Digital Services,” Mar. 21, 2018, https://ec.europa.eu/taxation_customs/sites/taxation/files/fair_taxation_digital_economy_ia_21032018.pdf.

[21] Tax Foundation, “Tax PyramidingTax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action.,” TaxEDU, https://taxfoundation.org/taxedu/glossary/tax-pyramiding/.

[22] Garrett Watson and Daniel Bunn, “Learning from Europe and America’s Gross Receipts TaxGross receipts taxes are applied to a company’s gross sales, without deductions for a firm’s business expenses, like compensation, costs of goods sold, and overhead costs. Unlike a sales tax, a gross receipts tax is assessed on businesses and applies to transactions at every stage of the production process, leading to tax pyramiding. Experiences,” Tax Foundation, Feb. 12, 2019, https://taxfoundation.org/europe-america-gross-receipts-taxes/.

[23] Council of the European Union, “OPINION of the European Economic and Social Committee: Proposal for a Council Directive on the common system of a digital services tax on revenues resulting from the provision of certain digital services,” Jul. 30, 2018, https://data.consilium.europa.eu/doc/document/ST-11484-2018-INIT/en/pdf.

[24] Kristian Jensen, Petteri Orpo, and Magdalena Andersson, “Nordic states urge U-turn on EU digital tax plans,” Euobserver, Jun. 1, 2018, https://euobserver.com/nordics/ar6f098882.

[25] Directorate-General for Taxation and Customs Union, “EU VAT rules for e-commerce two years on: Updated revenue figures point again to a successful implementation,” Taxation and Customs Union, Jun. 30, 2023, https://taxation-customs.ec.europa.eu/news/eu-vat-rules-e-commerce-two-years-updated-revenue-figures-point-again-successful-implementation-2023-06-30_en.

[26] Directorate-General for Taxation and Customs Union, “Continued growth in revenue and registrations confirms success of reformed EU VAT rules for e-commerce,” Taxation and Customs Union, Jul. 23, 2025, https://taxation-customs.ec.europa.eu/news/continued-growth-revenue-and-registrations-confirms-success-reformed-eu-vat-rules-e-commerce-2025-07-23_en.

[27] European Commission, “EU spending and revenue: Data 2000-2024,” Sep. 25, 2025, https://commission.europa.eu/document/download/45d0623a-529e-44d2-aae4-2ca9bac87ec3_en?filename=eu_budget_spending_and_revenue_2000-2023.xlsx.

[28] The national VAT base to which the call rate is applied cannot exceed 50 percent of the gross national income. Currently the call rate is 0.3 percent. Source: Council of the EU, “Value added tax (VAT) in the EU,” https://www.consilium.europa.eu/en/policies/vat/#:~:text=Financing%20the%20EU%20budget,the%20EU’s%20own%20resource%20revenue.

[29] Until recently, the VAT resource base for a member country for a given year was the total net VAT revenue collected during that year divided by the rate at which the VAT rate was levied during the year. If more than one VAT rate was applied, the harmonized VAT base was calculated by dividing the VAT revenue by the weighted average rate. However, from 2021, each Member State will apply the weighted average VAT rate of 2016, throughout the 2021-2027 period. See: European Commission, “The Value Added Tax (VAT)-based own resource in 2021-2027,” December 2022, https://commission.europa.eu/ strategy-and-policy/eu-budget/long-term-eu-budget/2021-2027/revenue/own-resources/value-added-tax_en.

[30] If the VAT base cap is not binding and the new own resources framework envisages its removal.

Additionally, by increasing the call rate from 0.3 percent to its historical level of 1 percent, the additional revenue for the EU budget would rise to approximately €7.7 billion.

[31] Cristina Enache, “How Smart Policy Can Unlock VAT’s Revenue Potential,” Tax Foundation, Apr. 7, 2026, https://taxfoundation.org/blog/eu-vat-policy-government-revenue/.

Share this article

{kind=link}