AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $24.77

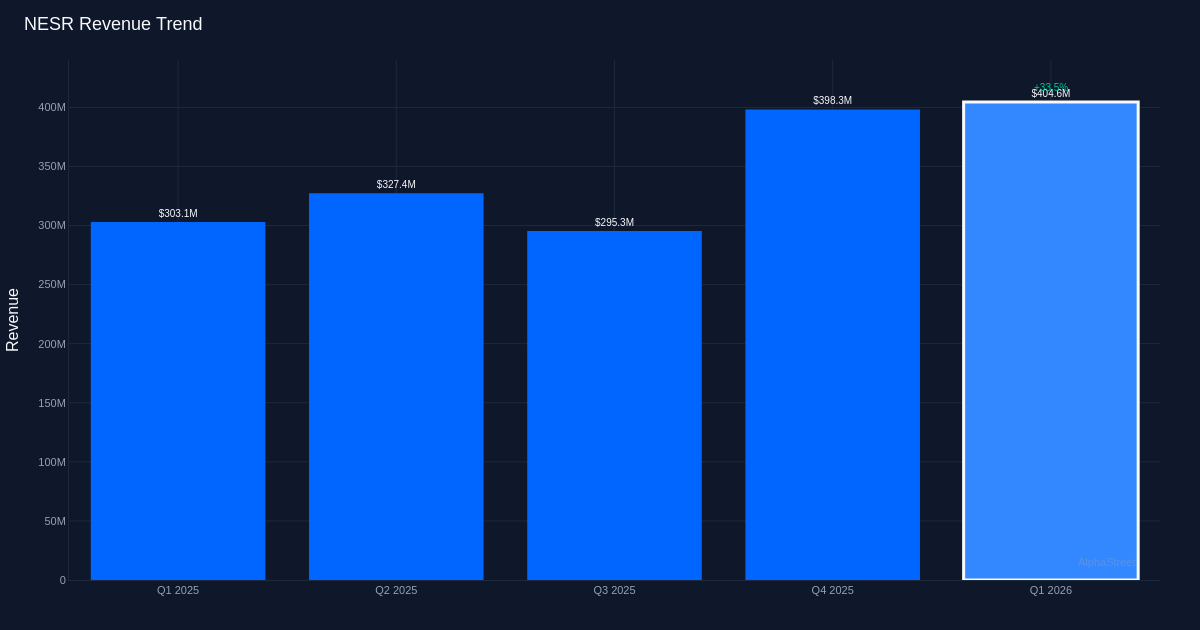

Solid Beat. National Energy Services Reunited Corp. (NESR) delivered a convincing first quarter performance, with adjusted diluted EPS of $0.26 per share surpassing the consensus estimate of $0.21 by 23.8%. The oilfield services provider demonstrated strength across its business, posting revenue of $404.6M that topped Wall Street’s $376.4M expectation by 7.5%. The company reported net income of $26.7M for the quarter, reflecting improved profitability as operations scaled.

Revenue-Driven Growth. The quality of this quarter’s outperformance appears encouraging, with the top-line expansion providing the foundation for the earnings beat. Revenue surged 33.5% year-over-year from $303.1M in Q1 2025, signaling robust demand for the company’s equipment and services amid an active drilling environment. This magnitude of organic growth suggests NESR is capturing market share or benefiting from favorable industry dynamics rather than merely cutting costs to meet earnings targets. The company generated Adjusted EBITDA of $77M for the quarter, though this figure provides limited context without sequential or year-ago comparisons.

Market Positioning. The substantial revenue acceleration positions NESR favorably within the oil and gas equipment and services sector, where operators have been selectively increasing capital expenditures in response to stabilizing commodity prices. The 33.5% year-over-year revenue growth rate substantially outpaces typical industry expansion, indicating the company is either winning new contracts, expanding service offerings with existing clients, or operating in particularly active geographic markets. The ability to convert this top-line momentum into profitability—evidenced by the $26.7M adjusted net income figure—demonstrates operating leverage within the business model.

Stock Response. Shares rose 7.2% to $24.77 in morning trade on Monday.

Analyst Confidence. Wall Street maintains a decidedly bullish stance on NESR, with consensus standing at 8 buy ratings, 1 hold, and 0 sell recommendations. This overwhelmingly positive view from the analyst community suggests confidence in the company’s business model and growth trajectory extends beyond a single strong quarter.

What to Watch: The critical question is whether NESR can sustain this 33.5% revenue growth trajectory or if Q1 represented a cyclical peak. Investors should monitor contract backlog disclosures, utilization rates for key equipment, and management commentary on pricing power as indicators of whether this momentum can continue through 2026.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

")

{kind=link}