In June 2026, the European Commission proposed a Tax Omnibus package to simplify the EU’s direct taxA direct tax is levied on individuals and organizations and is not expected to be passed on to another payer (unlike indirect taxes such as sales and excise taxes), though economic incidence can still fall upon others. Often with a direct tax, such as the individual income tax, tax rates increase as the taxpayer’s ability to pay, or financial resources, increases, resulting in what is called a p framework. Among other things, it would remove the holding-percentage requirement for exempting dividend, interest, and royalty payments between EU companies from withholdingWithholding is the income an employer takes out of an employee’s paycheck and remits to the federal, state, and/or local government. It is calculated based on the amount of income earned, the taxpayer’s filing status, the number of allowances claimed, and any additional amount the employee requests. taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.. Payments leaving the EU untaxed in the recipient’s state would instead face a border withholding tax. This measure would substantially reduce a source of double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. and administrative friction for cross-border investment in Europe.

How Does Cross-Border Tax Withholding Work?

A withholding tax is a tax that requires firms that pay dividends, interest, and royalties to foreign investors or businesses to withhold a certain portion for the tax authority in the source country.

Withholding taxes apply to income in its source jurisdiction, rather than in the recipient’s home jurisdiction, where it is usually taxed. This can help to ensure that resident taxpayers comply with the tax code and do not avoid taxation by shifting their income to other jurisdictions. However, withholding taxes can also lead to double taxation and distort the flow of capital across borders when investors’ income is taxed both domestically and abroad.

In practice, investors can usually credit withholding taxes paid abroad against domestic taxes due in their home country, but not always to the full amount or without delay. Therefore, even coordinated systems can create double taxation and administrative burdens, especially when refund or credit procedures are slow, inconsistent, or limited by treaty caps.

For example, when a company in Germany pays €100 in dividends to an investor in Greece, Germany withholds €26.37 (including a 5.5 percent solidarity surtaxA surtax is an additional tax levied on top of an already existing business or individual tax and can have a flat or progressive rate structure. Surtaxes are typically enacted to fund a specific program or initiative, whereas revenue from broader-based taxes, like the individual income tax, typically cover a multitude of programs and services. levied on the amount withheld) under domestic law. Under the bilateral tax treaty that limits withholding tax to 25 percent, the investor can reclaim €1.37 solidarity surtax from the German tax authority. Greece generally taxes dividends received by tax residents at a rate of 5 percent. But, when received from abroad, Greece grants a foreign tax credit for the amount already withheld in Germany, up to the domestic dividend tax rate. Due to the rate differential, a Greek tax resident pays a rate of 25 percent on his dividends received from a German company, instead of 5 percent when received from a company located either in Greece or a jurisdiction without withholding taxes on dividends, like the United Kingdom.

When withholding taxes generate double taxation or high administrative burdens, they can lead investors to invest in assets with lower pre-tax returns or hold less diversified portfolios to avoid those burdens.

Closing the Gap on Free Movement of Capital

Ideally, policymakers should aim to guarantee the free movement of capital across borders by eliminating double taxation and administrative friction for both inbound and outbound payments to allow capital to be invested in the assets and locations with the highest returns.

For this reason, double taxation agreements between countries often include provisions to reduce bilateral withholding tax rates. At the corporate level, EU Directives already prohibit Member States from withholding dividends paid by a subsidiary to its parent company in a different Member State, if certain conditions are met.

The European Commission estimates that extending the Directives to exempt interest, royalty, and dividend payments between EU companies from withholding tax regardless of holding percentage would raise long-run GDP by at least 0.043 percent, at a cost of 0.027 percent in overall tax revenue. European companies would save an estimated €700 million annually in compliance costs and another €700 million in opportunity costs currently lost to refund delays, while avoiding double taxation would generate €3.8 billion in tax savings.

Withholding Tax Burdens on Inbound and Outbound Payments in Europe

The maps below show the inbound and outbound statutory withholding tax rates for all 32 European OECD and EU countries, which apply when income crosses their borders. The average rate is weighted by the 2024 private capital stock of other European countries to approximate a broad, diversified European portfolio. A country’s inbound rates reflect the direct impact on a country’s savings opportunities for investors, while outbound rates reflect the business financing conditions.

For the ease of cross-border savings and investment, policymakers should seek to minimize double taxation risks and administrative frictions that can be posed by withholding taxes for either incoming or outgoing payments.

European countries differ considerably in their withholding tax burdens, with Belgium, Greece, Italy, Portugal, and Turkey showing consistently high burdens across both directions and types of payment. In contrast, Hungary, Switzerland, the United Kingdom, and the Czech Republic generally offer more favorable conditions for cross-border savings and investment.

On average, savers investing in a European stock portfolio face an inbound withholding tax rate of 5.6 percent. Investors residing in Cyprus (15.1 percent), Portugal (11.4 percent), and Greece (11.3 percent), face the highest inbound rates on dividends received from abroad. In contrast, investors based in Switzerland (2.3 percent) face the lowest inbound rates on dividends, followed by the United Kingdom (3.1 percent) and Denmark (3.4 percent).

For interest payments, investors earning cross-border interest income face an average withholding tax rate of 3.4 percent. Those residing in Cyprus (8.5 percent) face the highest withholding rates on interest received from abroad, followed by Turkey (7 percent) and Portugal (6.2 percent). By contrast, the Czech Republic (1 percent), Hungary (1.3 percent), and the Slovak Republic (1.4 percent) record the lowest inbound rates on interest.

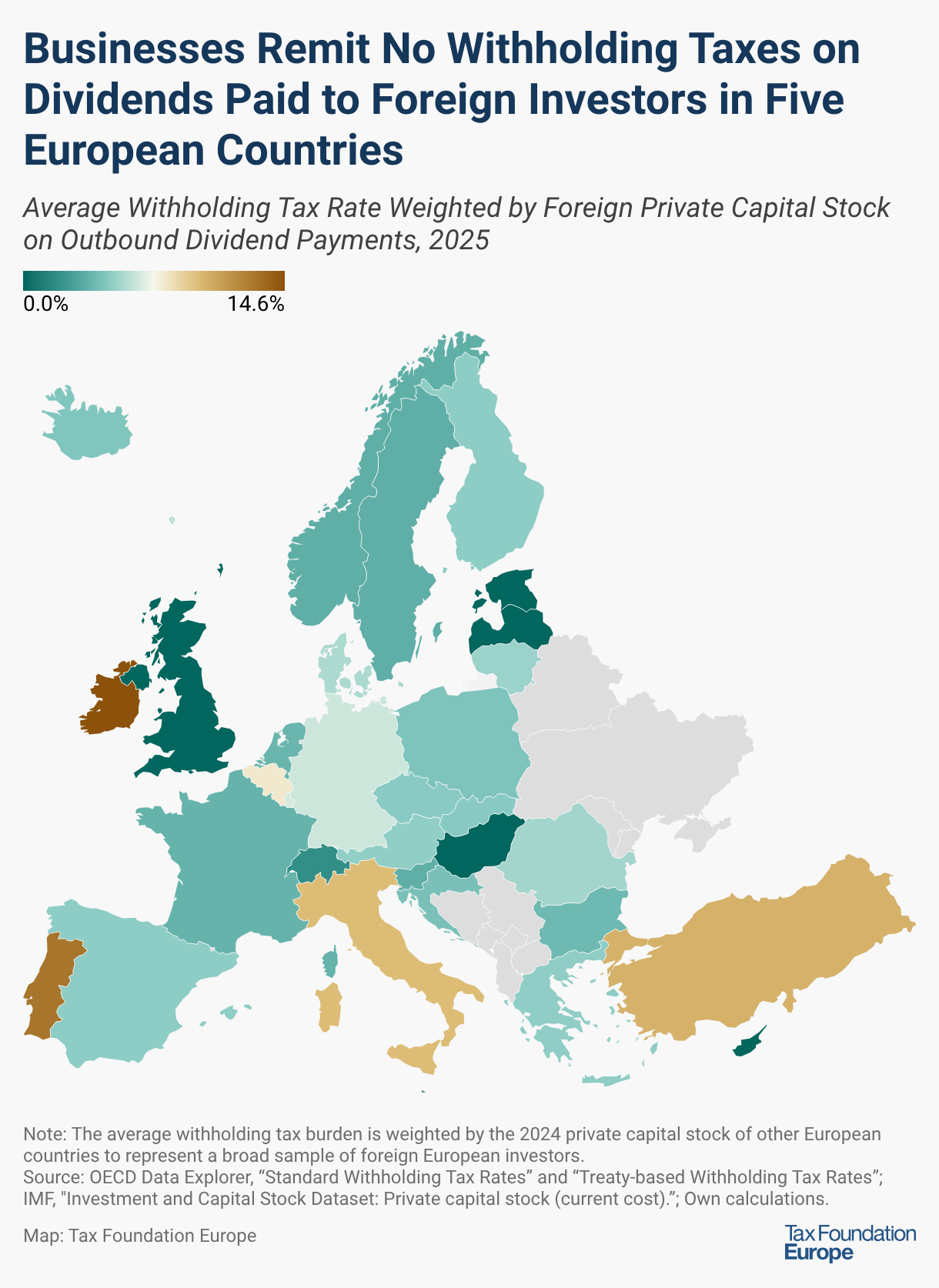

Businesses residing in Ireland (14.6 percent), Greece (14 percent), Portugal (13 percent), and Turkey (10.3 percent) remit the highest outbound rates on dividends paid to their foreign shareholders, while businesses in Cyprus, Estonia, Hungary, Latvia, Malta, and the United Kingdom are not obliged to remit withholding tax on outbound dividends.

Withholding taxation remains a source of double taxation and administrative friction for cross-border savings and investment in Europe. Extending existing exemptions to remove withholding taxes on intra-EU dividend, interest, and royalty payments regardless of holding percentage would address this friction directly and bring the Single Market closer to the free movement of capital it is intended to guarantee.

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign Up

Average Inbound and Outbound Withholding Tax Burdens in European OECD and EU Countries, 2025

Note: The average withholding tax burden is weighted by the 2024 private capital stock of other European countries to represent a broad sample of foreign European investors.

Source: OECD Data Explorer, “Standard Withholding Tax Rates” and “Treaty-based Withholding Tax Rates”; IMF, “Investment and Capital Stock Dataset: Private capital stock (current cost)”; authors’ calculations.

Share this article

")

Q2 2026 Preview: EPS Est. alt=")

")

{kind=link}