Published on May 6th, 2026 by Josh Arnold

Paramount Resources (PRMRF) has two appealing investment characteristics:

#1: It is offering an above average dividend yield of 1.9%, which is nearly twice the dividend yield of the S&P 500.#2: It pays dividends monthly instead of quarterly.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

The combination of an above-average dividend yield and a monthly dividend renders Paramount Resources appealing to individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about Paramount Resources.

Business Overview

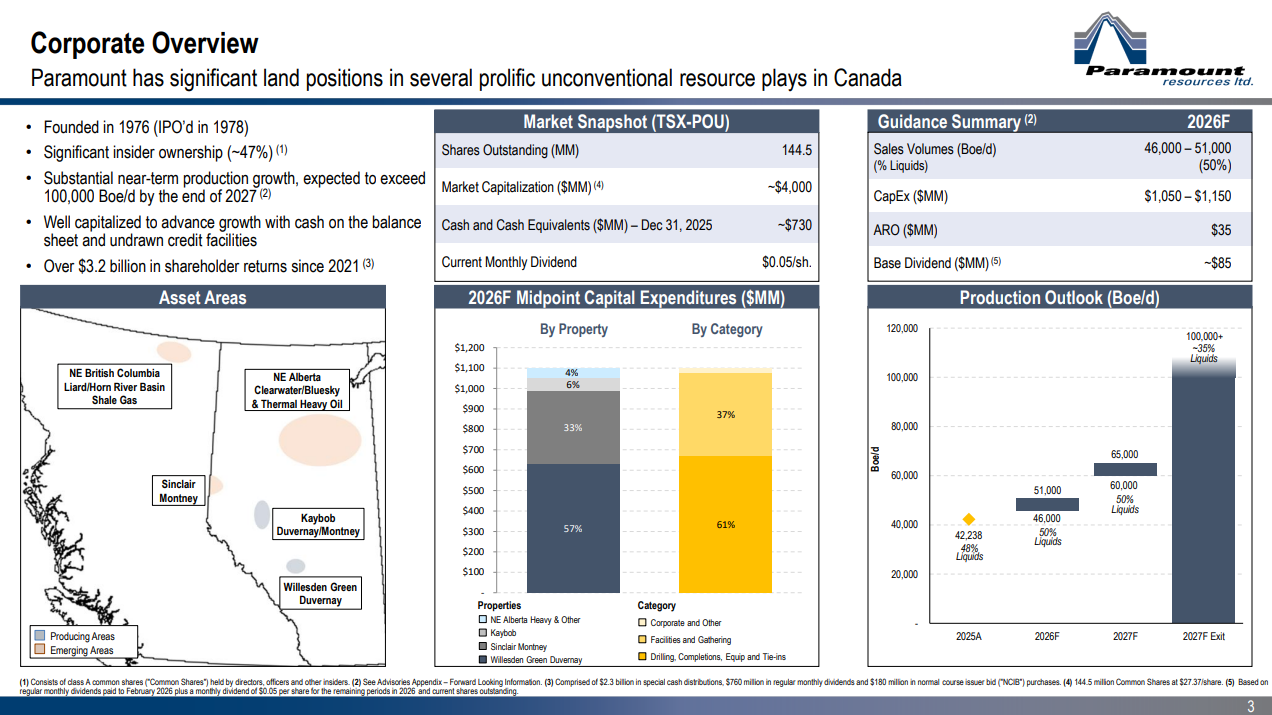

Paramount Resources explores for and produces oil and natural gas from conventional and unconventional fields in the Western Canadian Sedimentary Basin.

The company holds interests in the Karr and Wapiti Montney properties, which cover an area of 185,000 net acres south of Grande Prairie, Alberta. It was founded in 1976 and is based in Calgary, Canada.

Paramount Resources has an aspirational average production rate of about 100,000 barrels per day and total proved reserves of 400+ million barrels of oil equivalent, with oil and gas at a roughly 50/50 ratio.

Source: Investor Presentation

It is also important to note that 46% of the company is owned by insiders. This is a remarkably high percentage of ownership, which results in the alignment of interests between insiders and the other individual shareholders.

As an oil and gas producer, Paramount Resources is highly cyclical due to the dramatic swings in oil and gas prices. The company has reported losses in five of the last ten years and resumed its dividend payments only in the summer of 2021, after 22 years without a dividend payment.

On the other hand, Paramount Resources has some advantages over well-known oil and gas producers. Most oil and gas producers have been struggling to replenish their reserves due to the natural decline of their producing wells.

Paramount posted fourth quarter and full-year earnings on March 3rd, 2026, and results were somewhat weak. Earnings fell to a fractional loss, which was sharply lower from a profit of 43 cents per share a year earlier. The company divested some assets, so a decline was expected, but perhaps not one quite this large. The company completed the first phase of its Alhambra Plant in July of 2025, which was ahead of schedule. Production there should ramp up in the ensuing months, but no progress in results just yet.

We see just 55 cents in adjusted earnings-per-share for this year, noting Paramount stands to benefit from higher energy prices so long as they persist.

Growth Prospects

The company has ample room for production growth thanks to accelerating its development efforts in its producing areas.

Source: Investor Presentation

Paramount Resources has a proven record of identifying key resource areas with a low decline rate and more than 15 years of production.

On the other hand, as an oil and gas producer, Paramount Resources is highly sensitive to oil and gas price cycles. This is clearly reflected in the company’s performance record, which has posted material losses in three of the last ten years.

The price of oil has risen significantly from its low so far this year due to the war in Iran. The longer high prices persist, the better for Paramount’s earnings.

Given Paramount Resources’ promising production growth prospects and the highly cyclical nature of the oil and gas industry, we expect Paramount Resources’ earnings per share to grow by about 8.0% per year on average over the next five years, from an estimate of $0.55 this year to $0.81 in 2031.

Dividend & Valuation Analysis

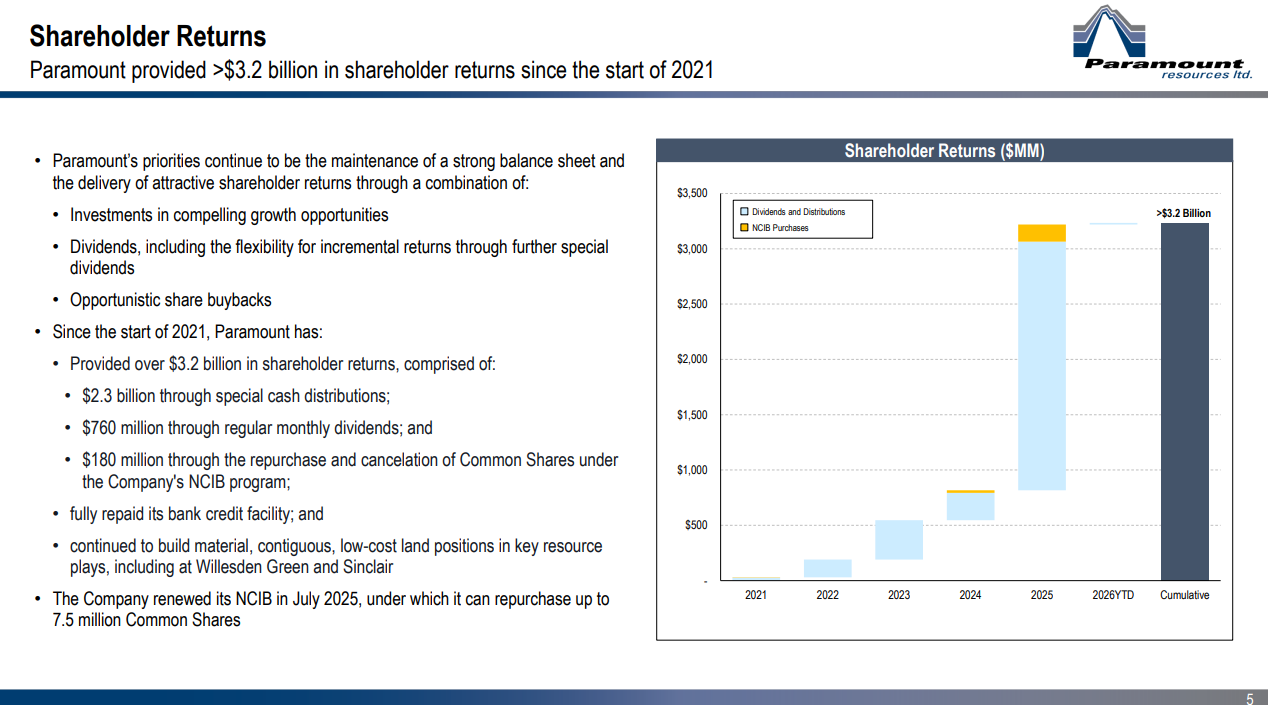

Paramount Resources is currently offering an above-average dividend yield of 1.9% , which is nearly double the ~1% yield of the S&P 500. The stock is thus an interesting candidate for income-oriented investors, but they should be aware that the dividend is far from safe due to the dramatic cycles of oil and gas prices. Paramount Resources has an elevated payout ratio of 78%.

However, it is critical to note that Paramount Resources reinstated its dividend only in mid-2021, after 22 years without a dividend payment.

The company failed to offer a dividend in the preceding years, as it incurred material losses in many of those years. Therefore, the company’s dividend is far from safe.

Regarding valuation, Paramount Resources is currently trading for a staggering 42 times its expected earnings per share of $0.55 this year.

Given the company’s high cyclicality, we assume a fair price-to-earnings ratio of 11, which is a typical mid-cycle valuation level for oil and gas producers.

Considering the 8.0% annual growth of earnings per share, the 1.9% current dividend yield, and a massive headwind from the valuation, Paramount Resources could offer a heavily negative annual total return over the next five years.

The expected return signals that the stock is quite unattractive today for long-term buyers, particularly if energy prices decline from currently very high levels. Therefore, investors should wait for a lower entry point.

Final Thoughts

Thanks to the above-average oil and gas prices, Paramount Resources has thrived since early 2022, and again in early 2026. The stock offers an above-average dividend yield of 1.9% and a payout ratio of 78%, so its attractiveness as an income stock has diminished meaningfully.

Moreover, the company has proved highly vulnerable to oil and gas price cycles. As the price of oil has peaked and may have a material downside, the stock is risky right now.

Paramount Resources also has a below-average trading volume. This means that it may be difficult to establish or sell a large position in this stock, but we recommend a sell rating.

Additional Reading

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Florida Roads Become a Battleground for Illegal Immigration")

{kind=link}