Updated on April 23rd, 2026 by Josh Arnold

Dynex Capital (DX) is a mortgage Real Estate Investment Trust (mREIT) that offers an appealing 14.8% yield, making it a potentially attractive high yield stock.

Dynex Capital also pays its dividends monthly, which is rare in a world where the vast majority of companies pay them quarterly.

There are currently 119 companies with monthly dividend payments.

You can see the full list of monthly dividend stocks (along with relevant financial metrics such as dividend yields, payout ratios, and more) by clicking on the link below:

Dynex Capital’s high dividend yield and monthly dividend payments make it an intriguing stock for investors, even though its dividend payment has declined in recent years, and it subjects investors to high levels of risk.

However, as with many high-dividend stocks, the sustainability of the dividend is an important consideration. This article will analyze Dynex Capital’s investment prospects.

Business Overview

Dynex Capital is a mortgage Real Estate Investment Trust (REIT). As a mortgage REIT, Dynex Capital invests in mortgage-backed securities (MBS) on a leveraged basis in the United States. It invests in agency and non-agency MBS, including residential MBS, commercial MBS (CMBS), and CMBS interest-only securities.

Agency MBS have a guaranty of principal payment by a U.S. government agency or a U.S. government-sponsored entity, such as Fannie Mae and Freddie Mac. Non-Agency MBS has no such payment guarantee. Dynex Capital, Inc., was founded in 1987 and is headquartered in Glen Allen, Virginia.

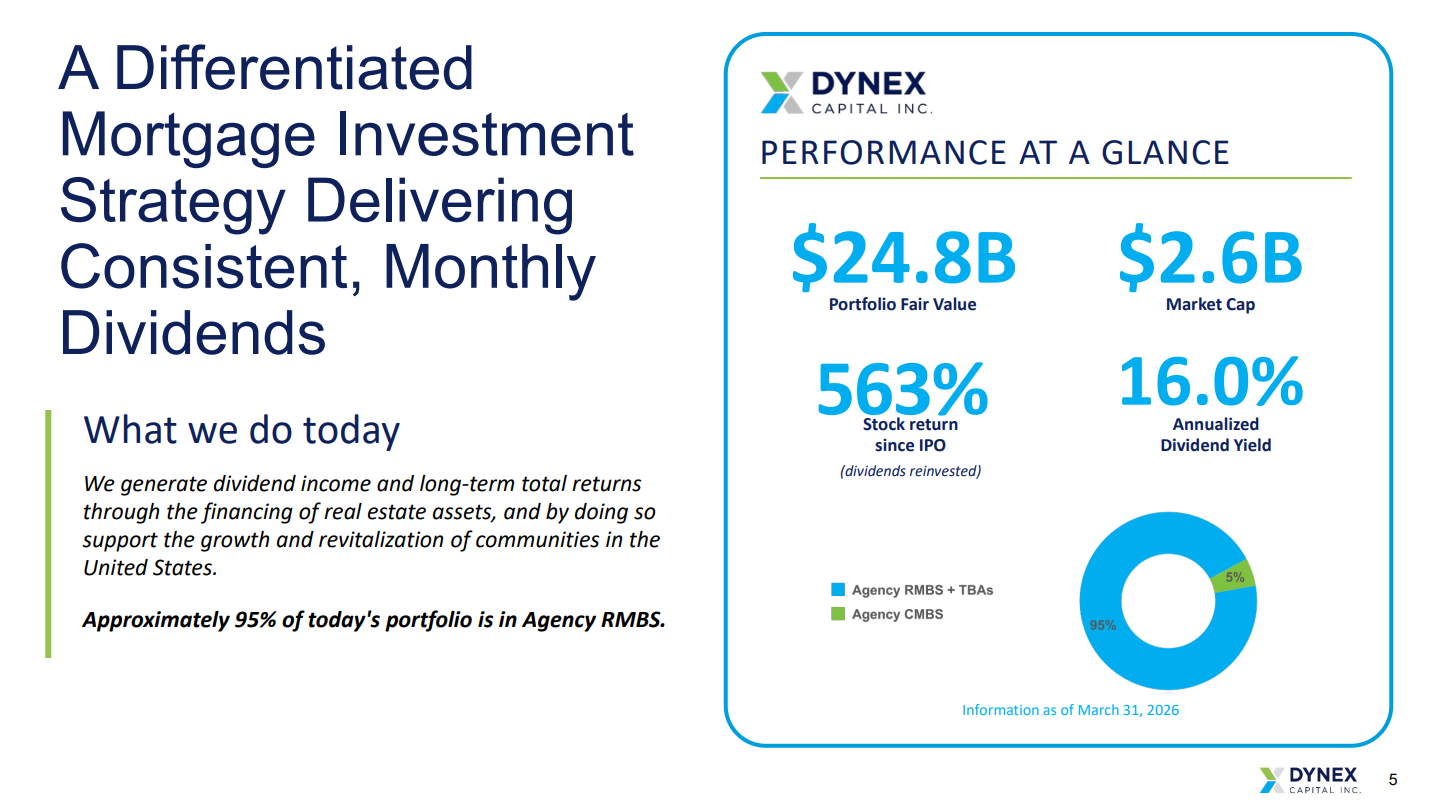

The company is structured to have internal management, which is generally positive because it can reduce conflicts of interest. Additionally, when they increase total equity, operating expenses have no material impact. Over time, Dynex’s management team has built a strong track record of generating attractive total returns for shareholders:

Source: Investor presentation

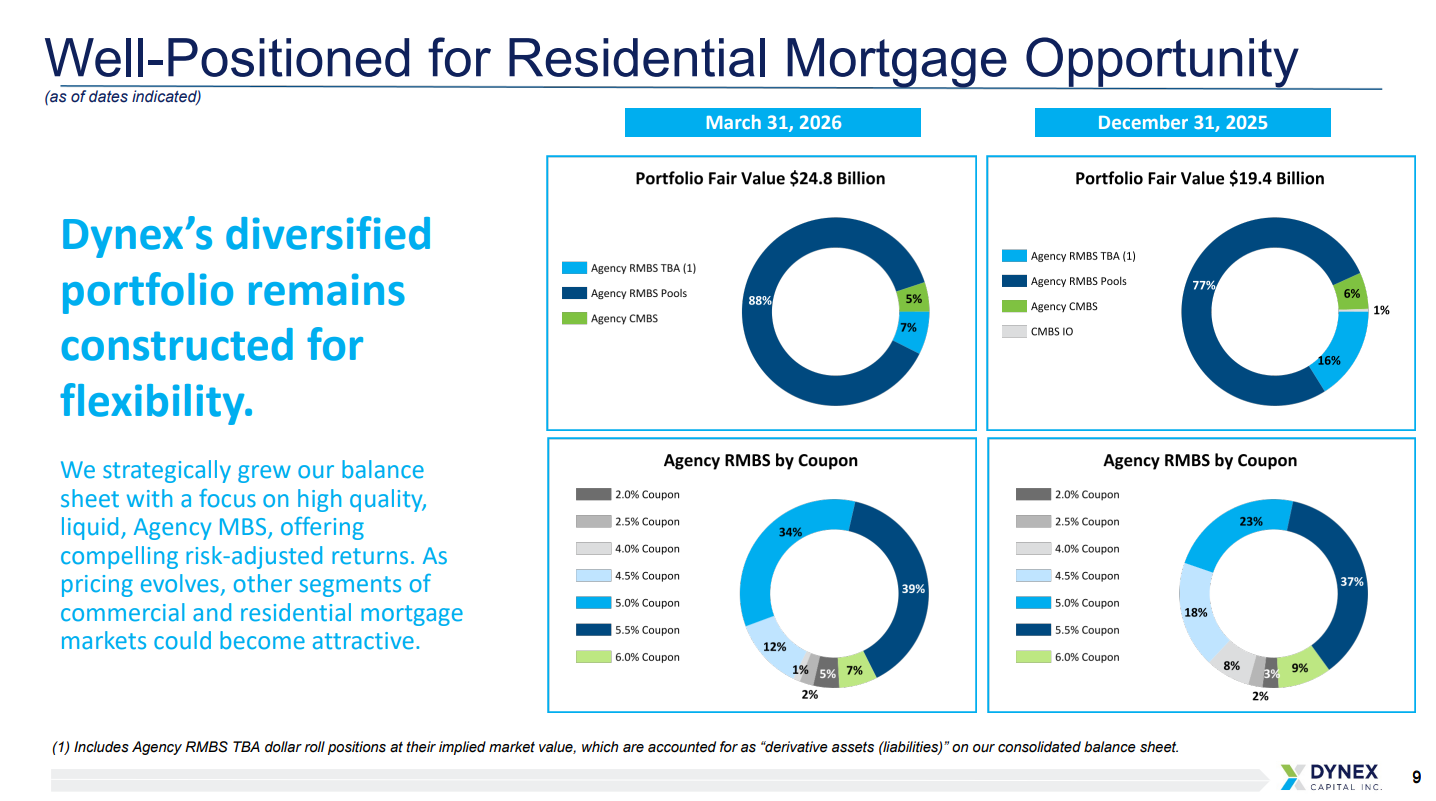

Dynex’s portfolio is structured to be widely diversified across residential and commercial agency securities. This diversified approach creates an attractive risk-to-reward balance that has benefited the company for many years. Over time, the mix of CMBS and RMBS investments has reduced the negative impacts of prepayments on portfolio returns. Furthermore, agency CMBS acts as a cushion in the event of unexpected volatility in interest rates.

Finally, the high-quality CMBS IO are selected for shorter duration and higher yield, with the intended impact of limiting portfolio volatility. A significant portion of Dynex’s Agency 30-year RMBS fixed-rate portfolio has prepayment protection via limits on incentives to refinance.

Management anticipates opportunistically increasing leverage in the high-quality asset portfolio while avoiding credit-sensitive assets that are leveraged with short-term financing. As a result, the company enjoys a highly flexible portfolio that frees management to pivot rapidly to other attractive opportunities as markets remain volatile.

Dynex posted first quarter earnings on April 20th, 2026, and results were mixed. Earnings on a GAAP basis came to a loss of 41 cents per share. Net interest income was up 82% year-over-year to $79.3 million. However, book value declined as wider mortgage spreads that occurred late in the quarter weighed on results. Earnings available for distribution came to 31 cents per share, beating estimates for 28 cents, and up sharply from 22 cents in the fourth quarter.

Book value per share fell to $12.60 in March, from $13.45 in December. This was driven mostly by a $1.40 per share loss in the investment portfolio, net of hedges, resulting from widening mortgage spreads. Estimates for book value were higher at $12.73. Total economic return for the quarter was -34 cents per share, or about 2.5%.

The trust issued $442 million in equity capital during the quarter through at-the-market transactions, causing the share count to rise once again, and diluting existing shareholders.

We see $1.17 in adjusted earnings-per-share for this year, but note the first quarter was not a particularly good start to 2026.

Growth Prospects

With interest rates now largely flat and the mortgage market suffering from tepid demand, Dynex may have a challenging time growing. On top of that, a recession is considered increasingly likely, which could lead to a jump in defaults on Dynex’s investments, posing a further headwind to growth. As a result, when combined with Dynex’s sky-high payout ratio, we expect earnings growth to be a challenge.

Source: Investor Presentation

We also note that results are inherently volatile, with book value and the trust’s ability to pay its distribution both being subject to the whims of interest rate markets.

Competitive Advantage & Recession Performance

Dynex possesses some competitive advantages, which may bolster investor returns throughout business cycles. These advantages include the accomplished management team with experience in managing securitized real estate assets through multiple economic cycles. Additionally, the trust’s focus on maintaining a diversified pool of highly liquid mortgage investments with the smallest amount of credit risk could be another advantage.

The trust’s normalized diluted earnings per share were quite stable through the last recession, though shares still sold off very heavily, losing about 40% of their market value. Overall, there’s little margin of safety here due largely to the payout ratio being so high, combined with highly volatile earnings-per-share.

Another risk is that prepayment speeds could rise due to seasonal factors. Additionally, the drop in mortgage rates could increase refinancing activity, further cutting into profits.

While some cash-out refinancing is already factored into the company’s prepayment expectations, and their portfolio has been structured to hedge against some of this, there will likely be some lost profits. This explains the company’s recent pattern of dividend reductions since 2019.

Dividend Analysis

The dividend has not been fully covered by earnings since 2021, with very weak earnings in those years and high dividend payments. In 2026, we expect this pattern to repeat itself, with only about half of the dividend expected to be covered by earnings. As a result, we expect the dividend to be cut at some point in the coming years.

Final Thoughts

Dynex Capital’s high dividend yield and monthly dividend payments make it attractive to high-yield dividend investors. However, we remain extremely cautious about the stock.

The company does not cover its dividend with earnings per share. Furthermore, the riskiness of the business model sets Dynex up for potentially steep losses if the economy slips into recession and defaults rise.

This makes the stock very risky. Despite the high dividend yield, investors looking for monthly income have better choices with more favorable growth prospects and safer dividends elsewhere.

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}