Stock $45.6 (-7%)

EPS YoY +14%|Rev YoY +12.4%|Net Margin 15.4%

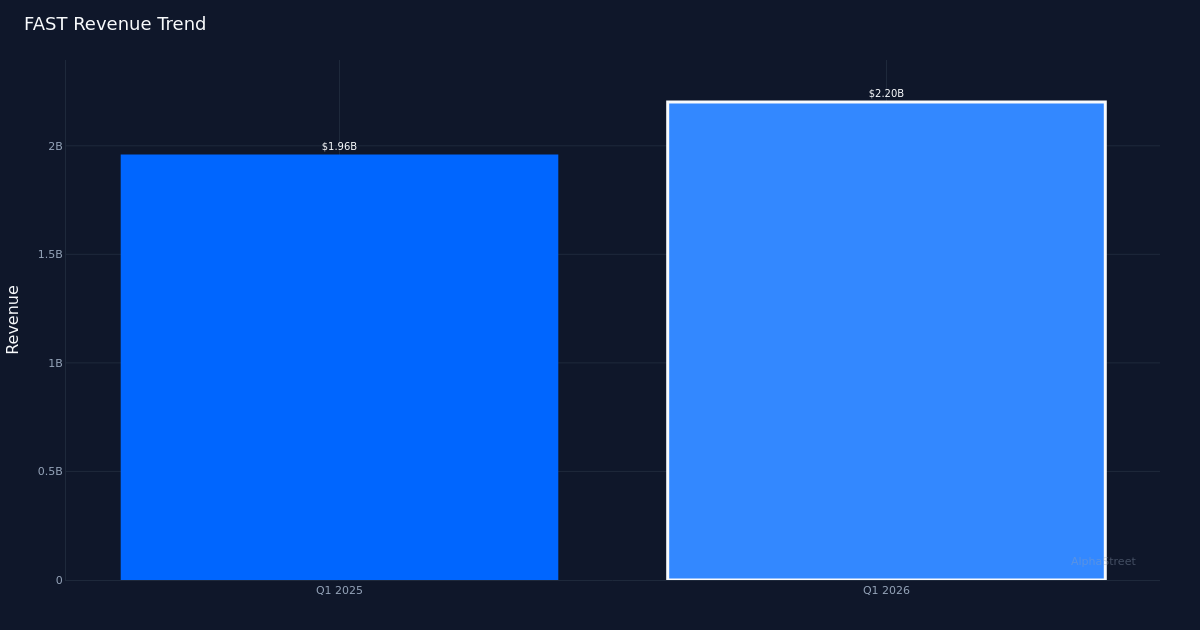

Fastenal Company’s (NASDAQ: FAST) earnings matched expectations in its first quarter, delivering exactly $0.30 per share against consensus estimates. The industrial distributor posted revenue of $2.20B and net income of $339.8M, representing a 12.4% top-line expansion that marked the company’s third consecutive quarter of double-digit growth. The stock declined following the announcement.

The earnings quality story reveals genuine operating leverage at work, not financial engineering. Net margin expanded to 15.4% from 15.2% a year ago, a 0.2 percentage point improvement that demonstrates Fastenal’s ability to convert incremental revenue into bottom-line profit. Operating margin reached 20.3%, while gross margin stood at 44.7%—both metrics reflecting the company’s pricing power and efficiency gains in a still-challenging industrial environment. The absolute dollar growth is compelling: net income climbed from $298.7M to $339.8M year-over-year, translating to a 14% EPS increase that outpaced revenue growth and signals improving operational efficiency.

The revenue trajectory shows sustained momentum but warrants closer examination of its composition. Q1 2026 revenue of $2.20B represents an acceleration from the prior year’s Q1 2025 result of $1.96B, with daily sales reaching $34.9M. Management highlighted that “our daily sales growth trends on a quarterly basis improved to 12.4% for the quarter from just over 11% in the fourth quarter of last year, and we continue to outperform the market.” This acceleration, while modest, suggests Fastenal is gaining share in an industrial distribution market that remains uneven. The 12.4% growth rate reflects both volume gains and pricing actions, though management’s commentary around price-cost neutrality—specifically the question “when would you expect to achieve price cost neutrality”—indicates that pricing dynamics remain a work in progress and could pressure future margin expansion if input costs rise faster than the company’s ability to pass through increases.

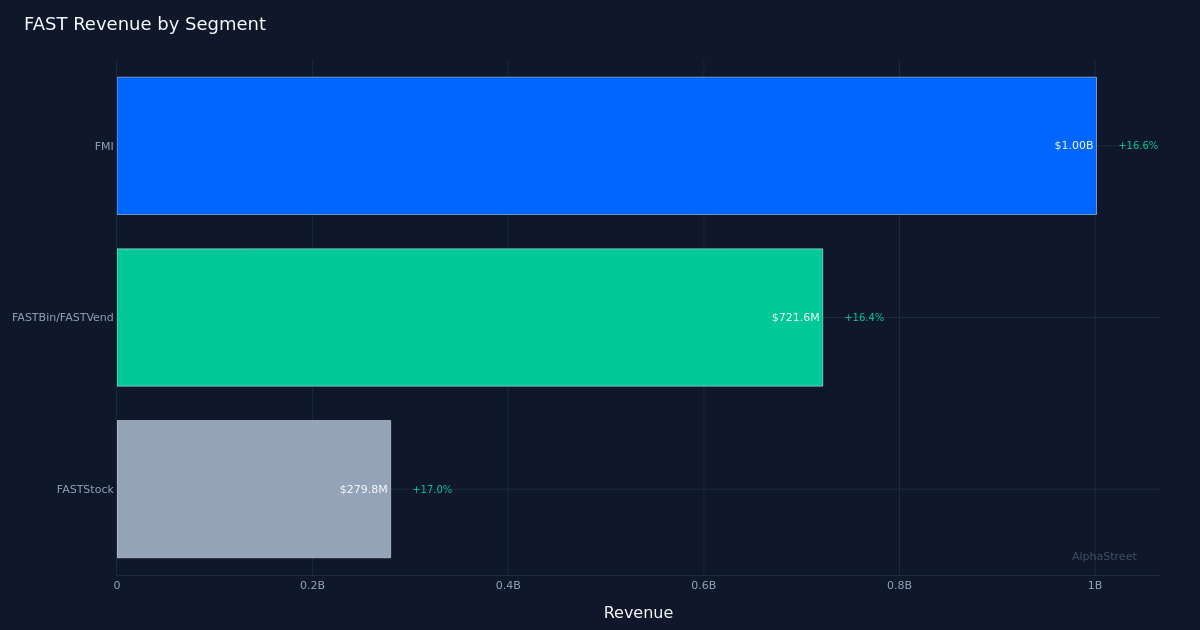

Segment performance reveals that Fastenal’s technology-enabled solutions are driving disproportionate growth. The FASTBin/FASTVend segment, which represents automated inventory management solutions, generated $721.6M with 16.4% growth. The FMI (Fastenal Managed Inventory) segment contributed $1.00B with 16.6% growth, while the FASTStock segment added $279.8M with 17.0% growth. All three segments are expanding at rates meaningfully above the company’s overall 12.4% revenue growth, which implies that legacy, non-technology-enabled business lines are growing more slowly or potentially declining. This bifurcation matters: the high-growth segments represent stickier, higher-margin revenue streams with embedded customer relationships that create switching costs. The company’s total sites reached 92,445, providing the distribution density that enables these technology solutions to scale. The segment data underscores Fastenal’s successful transition from a traditional fastener distributor to a comprehensive industrial supply chain solutions provider.

Operating cash flow of $378.4M demonstrates strong cash conversion but raises questions about working capital efficiency. While the absolute cash generation is healthy, the relationship between operating cash flow and net income of $339.8M shows limited cash conversion above reported earnings. For an industrial distributor managing 92,445 sites, inventory efficiency and receivables management become critical drivers of cash generation that deserve scrutiny in coming quarters.

The market’s reaction—shares declined and traded lower during Monday’s session. Investors appear to be worried about the flat results – in line with estimates – and muted margin performance. Even management recognizes that 20 basis points of operating margin expansion may not satisfy growth expectations.

The competitive positioning commentary reveals confidence in market share gains, though the magnitude remains unquantified. Management’s assertion that “we continue to outperform the market” during a period of 12.4% growth implies that the broader industrial distribution market is growing at a slower rate, but without specific market growth benchmarks, the scale of share gains remains unclear. The sustainability of this outperformance depends on whether it stems from secular shifts toward technology-enabled solutions (favorable and defensible) or cyclical factors like regional industrial activity patterns (less sustainable).

What to Watch: The path to price-cost neutrality will determine whether Fastenal can sustain or expand its 20.3% operating margin. Monitor whether the 20 basis point quarterly margin improvement rate accelerates, as management commentary suggests this is the key debate. Segment growth rates for FASTBin/FASTVend and FMI in Q2 will indicate whether the technology-enabled solutions can maintain their 16%-plus growth trajectory. Finally, the relationship between operating cash flow and net income in coming quarters will reveal whether working capital is becoming a headwind to cash generation as the business scales beyond 92,445 sites.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.

Has a By-Product Cash Engine Bigger Than a Simple Copper-Price Trade")

-1024x683.jpg "Florida Roads Become a Battleground for Illegal Immigration")

-1024x768.jpg "Red Snapper Used as Cudgel by Fed Judge")

(SPX:) (SPX:)")

{kind=link}