A year ago on April 2, President Trump charted a new course for US trade, calling it “Liberation Day.” The president said his idea was simple: the US would charge the same tariffs as our trading partners. With this new regime in place, Trump made a host of promises:

These tariffs would mark the day “American industry was reborn.”

They would “make Americans wealthy.”

Reciprocal tariffs would “bring in trillions and trillions of dollars to pay down America’s debt.”

“Jobs and factories,” he claimed, “will come roaring back.”

The new production enabled by the tariffs would “lower prices for consumers.”

At the height of the trade war—including the “Liberation Day” and other tariffs imposed under the International Emergency Economic Powers Act (IEEPA), plus sector-specific tariffs imposed under Section 232 authorities—the tariffTariffs are taxes imposed by one country on goods imported from another country. Tariffs are trade barriers that raise prices, reduce available quantities of goods and services for US businesses and consumers, and create an economic burden on foreign exporters. rates were the highest since 1911, constituting a $3.2 trillion taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. hike over a decade.

One year later, the evidence shows the tariffs were not reciprocal, did not generate the promised investment boom, raised less revenue than projected, and contributed to higher prices.

Were the Tariffs Reciprocal?

Recalling how the Liberation Day tariffs were calculated and imposed under IEEPA shows they were not reciprocal.

While the president said his idea was simple—apply the same tariffs to trade partners that they apply to us—the tariffs actually imposed were a far stretch from that. They were not based on observed foreign trade barriers or tariff schedules. Instead, the United States Trade Representative’s office converted each country’s bilateral goods trade balance into a synthetic tariff rate with a 10 percent minimum. Because bilateral goods trade balances do not measure trade barriers, the resulting tariffs had no relationship with other countries’ trade barriers.

And those tariffs changed many, many times between the April 2 announcement and February 2026, when the Supreme Court ruled the authority under which Trump imposed them did not authorize tariffs.

The first major change came just days after the Liberation Day speech in a back-and-forth escalation with China that took the US tariff rate to 125 percent for a month while the country-specific rates on other trading partners were delayed. During that period, the US applied tariff rate reached 21.5 percent under the combination of the IEEPA tariffs (baseline tariffs and higher country-specific tariffs) and Section 232 sector-specific tariffs.

In the months that followed, US tariff policy changed more than 50 times, spanning rate increases, rate decreases, new product exemptions, and new product inclusions. After multiple sets of exemptions, by the end of 2025, the IEEPA tariffs affected just 42 percent of US imports, and the applied tariff rate had fallen from its high of 21.5 percent to 13.6 percent before the Supreme Court ruling. Rather than ask whether the predictions made when tariffs were at their peak levels came to pass, the relevant question is whether the tariffs, as they were actually imposed, achieved the administration’s stated goals.

Did Investment and Jobs Pour into the United States?

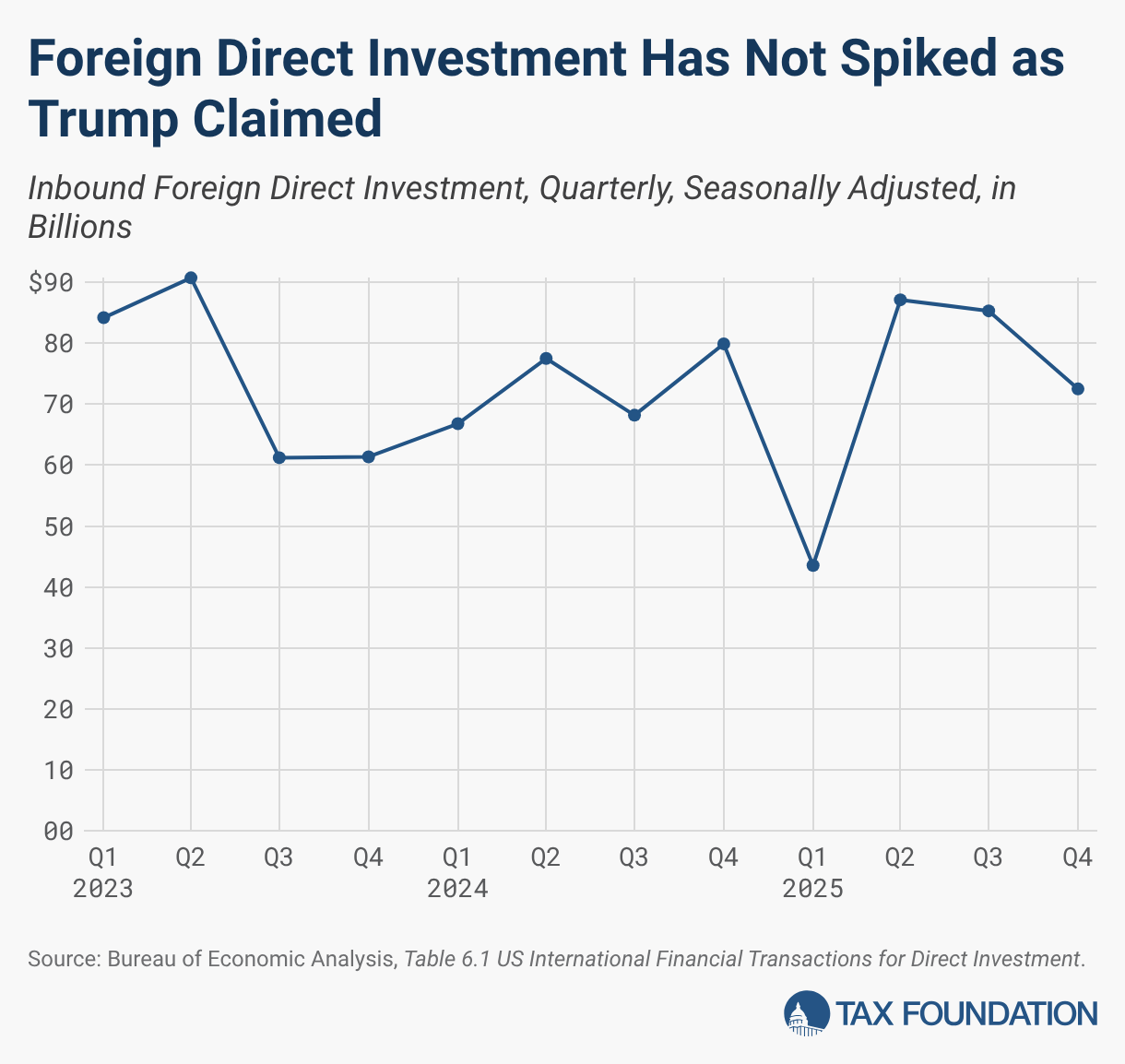

The data does not support claims of a large investment surge. During his Liberation Day remarks, President Trump claimed the US would see a rebirth of industries, with jobs and investment pouring into the United States. He claimed the US had already seen $6 trillion of investment and would see even more by year’s end. Throughout the year, he has claimed up to $18 trillion in new foreign investment into the United States.

Foreign direct investment (FDI) into the United States has seen no such dramatic spikes. In 2025, FDI totaled $288.4 billion—more than an order of magnitude smaller than President Trump’s claims. Total FDI in 2025 was below the prior 10 years’ average of $320.7 billion and lower than the annual totals in 2021, 2022, 2023, and 2024 ($405.5 billion, $338.4 billion, $297.4 billion, and $292.3 billion, respectively).

While various firms and countries have pledged, sometimes vaguely, to increase US investment, so far, those investments have not shown up in broad macroeconomic statistics. Aggregate FDI flows have remained within a typical range rather than exhibiting a sharp increase.

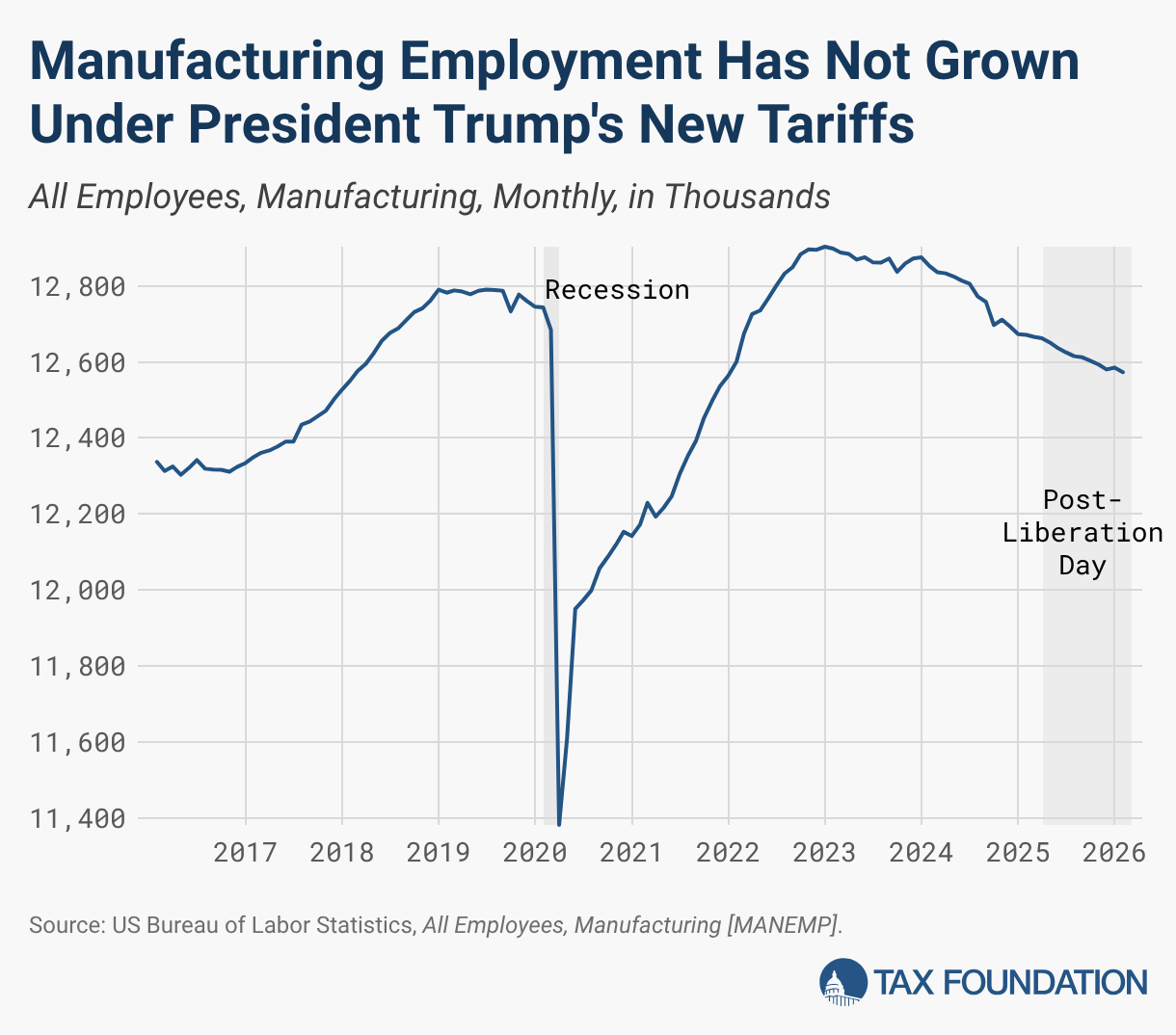

Neither has employment in the manufacturing sector reversed the trend. Manufacturing employment has continued to decline after Liberation Day, declining by 89,000 jobs between April 2025 and February 2026. The decline is broadly consistent with pre-existing trends.

The volatility in both rates and coverage created significant policy uncertainty, which likely weighed on investment and hiring decisions.

Did the Tariffs Make the Federal Government Wealthier?

Tariffs increased federal revenue, but fell far short of the Trump administration’s claims and did not pay down the national debt.

President Trump asserted that in the 1880s, when tariffs were high, the US was proportionately the wealthiest it had ever been: at that time, the federal government ran large budget surpluses because taxes generated more revenue for the government than it spent. President Trump often refers to the Congressional Commissions of that day, which were tasked with addressing the budgetary surpluses. They did so by increasing government spending, which proved unpopular in the 1890s.

While tariffs were the main source of federal revenue then, total spending was an order of magnitude lower, averaging under 3 percent of GDP rather than roughly 23 percent of GDP in 2025. The taxes that funded the federal government of the 1880s mathematically cannot raise enough revenue to fund the federal government today.

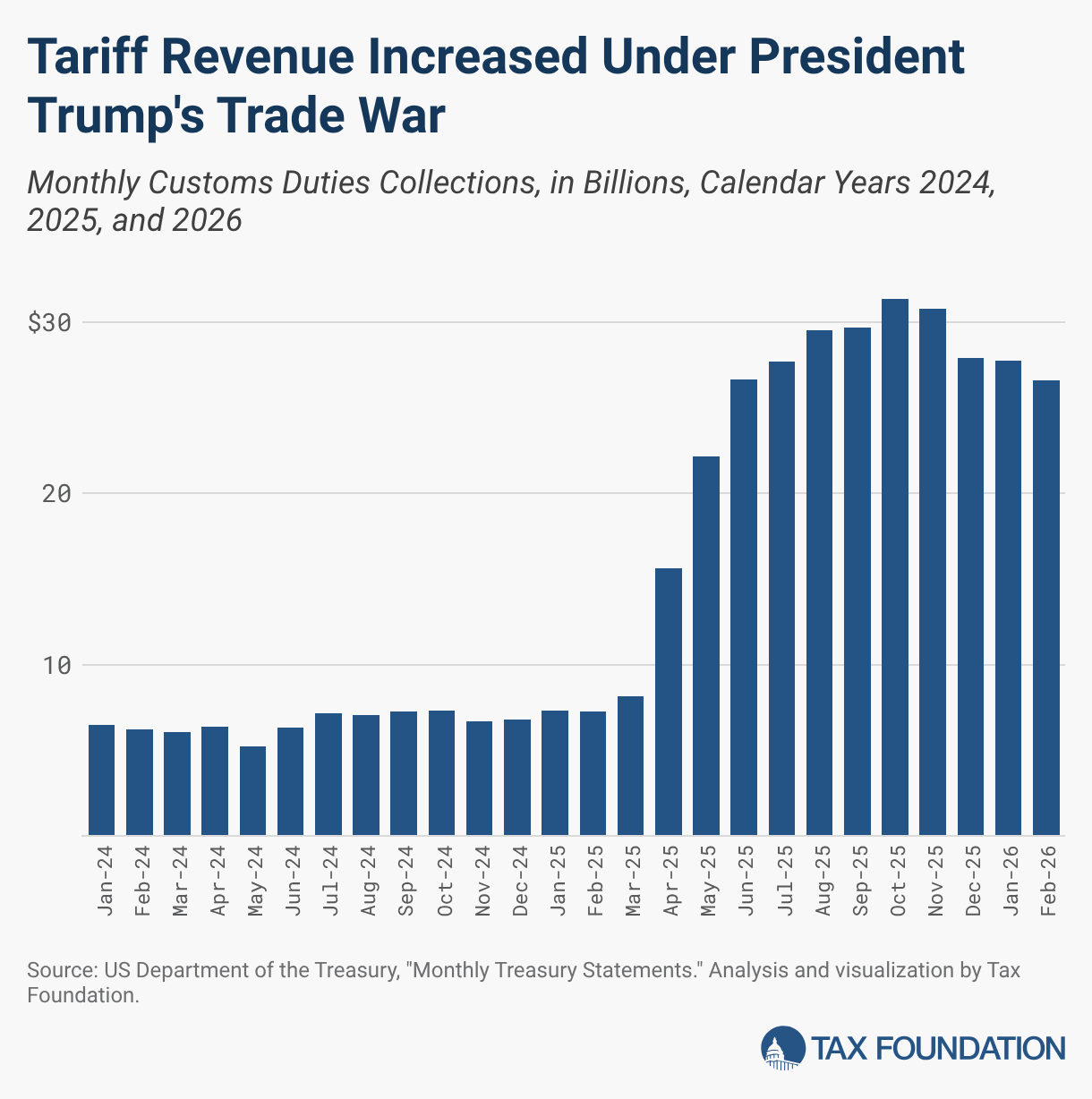

President Trump predicted tariffs would “direct hundreds of billions of dollars and even trillions of dollars into our Treasury to strengthen our economy and pay down debt.” And his advisors, such as Peter Navarro, estimated that the new tariffs would bring in $600 billion a year.

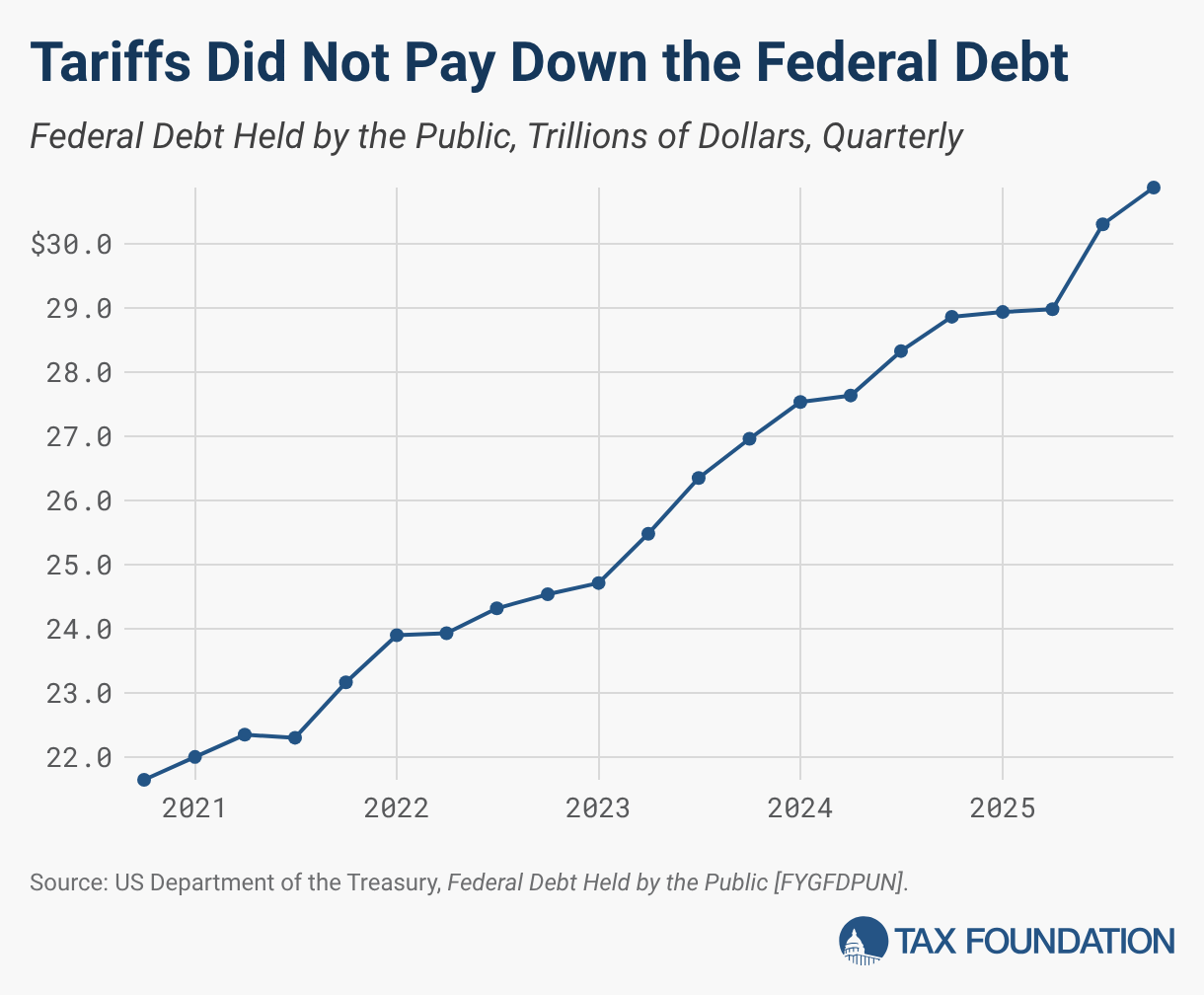

The Liberation Day tariffs undoubtedly raised taxes for the US Treasury—but far short of what the Trump administration predicted. Before the Court ruled against the IEEPA tariffs in February, they generated approximately $166 billion in tariff payments. Altogether, tariffs brought in $264 billion in customs duties from January through December 2025, accounting for 4.9 percent of total tax receipts for the calendar year. The net revenue generated by the tariffs is less, because tariffs mechanically reduce how much revenue is raised by income and payroll taxes. Though the tariffs increased tax revenues while they were in effect, federal debt has continued to grow under President Trump.

Did Tariffs Affect Prices and Employment?

Tariffs raised prices and weighed on economic activity, contrary to claims that they would be paid by foreign countries, lower consumer costs, and boost economic activity.

President Trump and his advisors have repeatedly asserted that Americans would not have to pay the tariffs, and the president even suggested that under the tariffs, “more production at home will mean stronger competition and lower prices for consumers.”

Tariffs are taxes on imports legally paid by the importer, and economically paid by a combination of imports, downstream businesses, final consumers, and foreign sellers. By raising the cost of imported goods, tariffs increase relative prices and can also lead domestic producers to raise prices in response. Tariffs can also affect employment in the short run as firms may lay off workers (or slow hiring) to hold employment costs (including the new taxes) fixed.

While research is still ongoing into both the price and employment effects of the tariffs in 2025, the findings so far are contrary to President Trump’s claims. The new tariffs have passed through to the US economy, lifting prices for importers and retail consumers and weighing down hiring.

Federal Reserve Chair Jerome Powell has attributed much of the remaining inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin to tariffs, explaining in a recent press conference: “These elevated readings largely reflect inflation in the goods sector, which has been boosted by the effects of tariffs.”

Research from the Pricing Lab at Harvard estimates that through October 2025, tariff pass-through to retail prices reached 24 percent, contributing a cumulative 0.76 percentage points to Consumer Price Index inflation. Prices for imported goods and for domestic substitutes have both risen. Initial research from the Kansas City Fed suggests (albeit with high levels of uncertainty) that tariffs likely reduced employment growth in 2025.

Additional research from the Federal Reserve found that rather than a sudden, one-time price hike after the tariffs were imposed, price pressure developed gradually and retailers slowly adjusted prices over time. The same uncertainty that held back investment and hiring may have also been an important factor limiting retail-level pass-through in 2025.

Conclusion

One year after Liberation Day, the evidence does not support the administration’s central claims about how tariffs were supposed to benefit the American economy. The tariffs were not reciprocal, did not produce a surge in investment or manufacturing employment, generated less revenue than projected, did not pay down the national debt, and contributed to higher prices and weaker economic activity. As policymakers consider future tariff actions under alternative authorities, these outcomes provide important context for evaluating the likely economic effects of continued trade restrictions.

Launch Tariff Tracker

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

Share this article

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}