Updated on April 1st, 2026 by Nathan Parsh

Monthly dividend stocks are great candidates for income-oriented investors’ portfolios. They distribute their dividends monthly and offer a smoother income stream.

In addition, many of these stocks are laser-focused on maximizing their distributions to their shareholders.

You can download our full Excel spreadsheet of all 117 monthly dividend stocks (along with metrics that matter like dividend yields and payout ratios) by clicking on the link below:

In this article, we will analyze the prospects of Fortitude Gold Corporation (FTCO).

Business Overview

Fortitude Gold is a U.S.-based gold producer that generates ~99% of its revenue from gold and targets projects with low operating costs, high returns on capital, and wide margins.

The company targets high-grade gold open pit heap leach operations averaging one gram per tonne of gold or greater. Its property portfolio currently consists of 100% ownership in seven high-grade gold properties.

All seven properties are within an approximate 30-mile radius of one another within the prolific Walker Lane Mineral Belt. The company generated over $18 million in revenues last year, most of which were from gold.

Source: Investor Presentation

On March 3rd, 2026, Fortitude Gold reported its Q4 results for the period ending December 31st, 2025. Revenue for the year was $18.4 million, 51% lower than last year.

The revenue decline was driven by a 64% drop in the number of ounces of gold sold. Silver sales volumes fell 43%. These declines were partially offset by a 36% increase in gold prices and a 31% improvement in silver prices.

As Fortitude Gold generates essentially all of its revenue from gold, it is obviously highly sensitive to the cycles of the price of gold. The average price of gold grew 64% to $4325.45 per ounce during 2025. Gold is up nearly 7% year-to-date as well.

Moving to the bottom line, the company recorded a mine gross profit of $10.0 million compared to $18.3 million in 2024 due to lower net sales.

The company recorded net income of $0.4 million versus a net loss of $2.0 million in 2024. On a per share basis, the company posted net income of $0.02, compared to a loss of $0.08 per share in the prior year.

We believe the company will produce earnings-per-share of $0.25 in 2026, which would be a significant improvement over last year’s result.

Growth Prospects

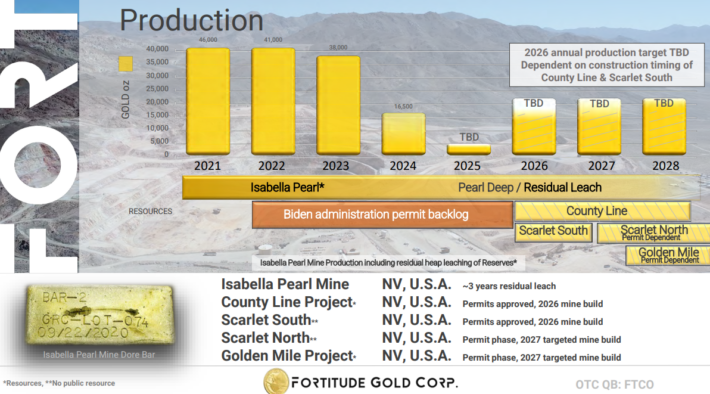

Some of Fortitude Gold’s previously cloudily outlook has been removed as it was approved for deeper mining operations at the Isabella Pearl deposit. Furthermore, operations commenced at both the County Line and Scarlet South locations earlier this year.

Source: Investor Presentation

Therefore, FTCO stock is a high-risk, high-reward situation. On one hand, rising gold prices and improved operating processes can significantly enhance the company’s financial performance amid higher profit margins.

On the other hand, declining gold prices and rising expenses, could negatively affect profitability. Furthermore, high gold prices weren’t enough to help the company turn a profit in 2024 and results last year were only mildly improved.

On the bright side, inflation has persisted, and with the Federal Reserve unlikely to lower interest rates in the near-term, gold prices are likely to remain high.

This bodes well for the price of gold, and by extension FTCO, for the foreseeable future. That said, given how the company has performed even with gold at record highs, we forecast annual earnings growth of 0% through 2031.

Competitive Advantages & Recession Performance

Gold producers are infamous for their cyclicality, which is caused by the wild swings in the price of gold. Fortitude Gold is inevitably vulnerable to these cycles, but it is an above-average gold producer thanks to some key characteristics.

Its properties also feature exceptionally high-ore grade and near-surface deposits, resulting in low-cost operations relative to its peers.

Additionally, the balance sheet is pristine, with $136.2 million in total assets against just $31.8million in total liabilities, resulting in a strong equity value of $104.4 million.

Moreover, Fortitude Gold enjoys another key competitive advantage: namely, the exceptional grade of Isabella Pearl Mine.

As a result, Fortitude Gold is much more profitable than most of its peers at a given gold price and is one of the most resilient gold producers to price downturns.

It is also worth noting that the price of gold often rises during recessions, as the precious metal is considered a safe haven during selloffs of the stock market. This means that Fortitude Gold is likely to perform well during recessions.

Dividend & Valuation Analysis

Income investors should avoid gold stocks in principle due to the high cyclicality that results from the swings of the price of gold. It is not accidental that there are no gold producers in the list of Dividend Aristocrats.

Fortitude Gold hasn’t been immune to this volatility. The company was forced to cut its monthly dividend by 75% to just $0.01 in May of 2025. Whereas the stock used to yield nearly 10%, it now yields 2.4%.

While the cut was painful, it does bring the expected payout ratio to a much more reasonable 48% for 2026.

Furthermore, the gold producer’s healthy balance sheet means that the current dividend is likely to remain safe for the foreseeable future.

Conversely, investors should always be aware of commodity producers’ vulnerability to commodity cycles.

If the price of gold enters a prolonged downturn at some point in the future, Fortitude Gold’s dividend is likely to come under pressure again. Gold producers need to spend significant amounts on capital expenses to replenish their reserves.

Fortitude Gold trades at 20.3 times expected earnings-per-share of $0.25. This is far above our target price-to-earnings ratio of 8.5 and implies an annual headwind from multiple contraction of 16% over the next five years.

Even with the starting dividend yield, total returns are expected to be -11.7% per year through 2031.

Final Thoughts

Gold producers are highly cyclical and should, therefore, be avoided by most income investors, who cannot stomach a volatile stock price and a potential dividend cut.

Fortitude Gold is highly sensitive to the cycles of the gold price, but it has some unique advantages, such as its high-quality projects. Its strong balance sheet also makes it much easier to endure the downturns of this business.

While it does pay a monthly dividend, Fortitude Gold had to reduce its distribution significantly last year, which caused the yield to plummet. Therefore, we believe the stock is an unappealing and risky stock for income investors to own.

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

{kind=link}