Updated on Febuaury 19, 2026 by Felix Martinez

Over time, the Dividend Aristocrats have proven to be among the best-performing dividend growth stocks in the entire market. Broadly speaking, the Dividend Aristocrats have leadership positions in their respective industries, with durable competitive advantages that allow them to generate long-term growth.

The Dividend Aristocrats are 69 S&P 500 companies that have increased their dividends for 25+ consecutive years.

You can download the full spreadsheet of all 69 Dividend Aristocrats, along with several important financial metrics such as price-to-earnings ratios and dividend yields, by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

A select number of Dividend Aristocrats also qualify as Dividend Kings, an even more exclusive group of 50 stocks that have raised their dividends for 50+ consecutive years.

Colgate-Palmolive (CL) is a Dividend Aristocrat and King. Its long history of dividend increases is due to its strong brands and dominant position across multiple product categories.

Colgate-Palmolive has paid uninterrupted dividends since 1895 and has increased its dividend payments for the past 64 consecutive years.

Colgate-Palmolive stock may be trading at a premium today, but it remains a strong holding for reliable, steady dividend growth.

Business Overview

Colgate-Palmolive’s roots date back to 1806, making it one of the oldest companies in the US stock market. It was founded by William Colgate, who started a business making starch, soap, and candles in New York City.

Today, the company manufactures oral care products like toothpaste, personal care products such as soap, home cleaning products, and pet food.

Major brands include Colgate, Palmolive, Hill’s Science Diet, and many more. The core segment is Oral Care, which constitutes nearly half of the company’s revenues. Colgate-Palmolive is a global giant. The company sells its products in over 200 countries and territories worldwide and generates annual sales of over $20.4 billion.

Colgate-Palmolive has a highly diversified product and geographic market portfolio. Approximately half of the company’s revenue comes from emerging markets, though its reliance on them for growth has waned recently.

This is due to the success of the company’s pet nutrition business, as it continues to take a revenue share from other segments. Emerging markets will be a critical growth catalyst for the company moving forward. Colgate-Palmolive has the #1 position in China, with a market share above 30%.

However, the company also faces several challenges, including global supply chain issues and pronounced inflation that’s increasing costs across the board, including in raw materials and labor. These factors could keep a lid on growth going forward.

Growth Prospects

Colgate-Palmolive generally enjoys a world-class brand portfolio and high profit margins. The company’s pet food products, in particular, are a compelling growth catalyst in the U.S., where pet food is a growth industry.

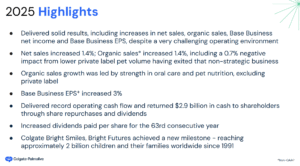

Colgate posted fourth-quarter earnings on January 30th, 2026. The company reported strong Q4 2025 underlying results, with base business EPS of $0.95, beating estimates, and net sales rising 5.8% year over year to $5.23 billion. Organic sales grew 2.2%, supported by pricing and continued strength in oral care and Hill’s Pet Nutrition, while global market leadership remained intact with 41.3% toothpaste share and 32.4% manual toothbrush share year-to-date.

Reported GAAP EPS declined to $(0.05) due to a $794 million after-tax goodwill and intangible impairment tied to the skin health business, masking otherwise stable operating performance.

For full-year 2025, net sales increased 1.4% to $20.4 billion, while base business EPS rose 3% to $3.69, demonstrating resilient earnings growth despite slower category demand and private-label headwinds in pet nutrition.

Operating cash flow reached a record $4.2 billion, allowing the company to return $2.9 billion to shareholders through dividends and share repurchases. GAAP EPS declined 25% to $2.63, primarily reflecting the non-cash impairment charge rather than deterioration in core operations.

Looking ahead to 2026, management expects net sales growth of 2%–6% and organic sales growth of 1%–4%, alongside gross margin expansion and increased advertising investment to support brand growth.

The company projects double-digit GAAP EPS growth and low-to-mid single-digit base business EPS growth, supported by innovation, digital and AI capabilities, and continued expansion in emerging markets, positioning Colgate-Palmolive for steady long-term earnings compounding despite a challenging consumer environment.

Source: Investor Presentation

We see Colgate-Palmolive producing an average annual earnings-per-share growth rate of 6% over the next five years.

Competitive Advantages & Recession Performance

Colgate-Palmolive has many competitive advantages that have fueled its growth over the past 200+ years.

First, it has built a dominant position in its core product categories, most notably in toothpaste, where Colgate-Palmolive’s market share has risen steadily for many years. Today, it commands a higher market share than the next three biggest competitors combined.

Such a high market share allows Colgate-Palmolive to charge higher prices for its premium products and raise prices over time. Pricing power is a critical competitive advantage for consumer goods stocks.

Another major advantage for Colgate-Palmolive is that its products are necessities of modern life. Consumers need oral, personal, and pet care products regardless of economic conditions. Colgate-Palmolive enjoys steady demand, which gives the company consistent profitability, even during recessions.

Colgate-Palmolive’s earnings-per-share through the Great Recession are shown below:

2007 earnings-per-share of $1.69

2008 earnings-per-share of $1.83 (8.3% increase)

2009 earnings-per-share of $2.19 (20% increase)

2010 earnings-per-share of $2.16 (1.4% decline)

Colgate-Palmolive generated positive earnings growth in 2008 and 2009, during the worst years of the recession. Earnings dipped slightly in 2010 but resumed growing in 2011 and thereafter.

The company’s strong performance from 2007 to 2010 is a credit to its strong business model and powerful brands. These same qualities helped Colgate-Palmolive remain highly profitable and raise its dividend in 2020, even with the impact of the global coronavirus pandemic.

Colgate-Palmolive’s dividend is also very safe. The company’s projected dividend payout ratio for fiscal 2026 is 53%, suggesting the dividend is well-covered.

Valuation & Expected Returns

With earnings-per-share expectations of about $3.90 for 2026, Colgate-Palmolive stock has a price-to-earnings ratio of 24.5.

Our fair value estimate for CL stock is a P/E multiple of 25. Therefore, the stock appears to be slightly undervalued. An increase in the P/E multiple could boost annual returns by 0.3% over the next five years.

In addition, CL shares have a current dividend yield of 2.2%.

Assuming the stock maintains a fairly stable valuation, along with our projected earnings growth and estimated adjusted earnings per share for 2026, we forecast that Colgate-Palmolive can deliver annualized total returns of approximately 8.5% through 2031.

As a result, we have assigned a hold rating to the company’s shares.

Source: Investor Presentation

Final Thoughts

Colgate-Palmolive is a high-quality business with several category-leading brands. The company has growth potential through product innovation, its Hill’s Pet Food brand, and growth in emerging markets.

Colgate’s dividend should remain well-covered, and so further dividend hikes in the coming years should be relatively easy.

With annual returns just above 8.5%, we currently rate CL stock a hold.

Looking for more dependable dividend growth stocks? The following Sure Dividend databases contain the most trustworthy dividend growers in our investment universe:

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

{kind=link}