Updated on November 21st, 2025 by Bob Ciura

In the world of investing, volatility matters. Investors are reminded of this every time there is a downturn in the broader market and individual stocks that are more volatile than others experience enormous swings in price.

Volatility is a proxy for risk; more volatility generally means a riskier portfolio. The volatility of a security or portfolio against a benchmark is called Beta.

In short, Beta is measured via a formula that calculates the price risk of a security or portfolio against a benchmark, which is typically the broader market as measured by the S&P 500.

Here’s how to read stock betas:

A beta of 1.0 means the stock moves equally with the S&P 500

A beta of 2.0 means the stock moves twice as much as the S&P 500

A beta of 0.0 means the stocks moves don’t correlate with the S&P 500

A beta of -1.0 means the stock moves precisely opposite the S&P 500

Interestingly, low beta stocks have historically outperformed the market… But more on that later.

You can download a spreadsheet of the 100 lowest beta S&P stocks (along with important financial metrics like price-to-earnings ratios and dividend yields) below:

This article will discuss beta more thoroughly, why low-beta stocks tend to outperform, and provide a discussion of the 5 lowest-beta dividend stocks in the Sure Analysis Research Database.

The table of contents below allows for easy navigation.

Table of Contents

The Evidence for Low Beta Stocks Outperformance

Beta is helpful in understanding the overall price risk level for investors during market downturns in particular. The lower the Beta value, the less volatility the stock or portfolio should exhibit against the benchmark.

This is beneficial for investors for obvious reasons, particularly those that are close to or already in retirement, as drawdowns should be relatively limited against the benchmark.

Importantly, low or high Beta simply measures the size of the moves a security makes; it does not mean necessarily that the price of the security stays nearly constant.

Securities can be low Beta and still be caught in long-term downtrends, so this is simply one more tool investors can use when building a portfolio.

The conventional wisdom would suggest that lower Beta stocks should underperform the broader markets during uptrends and outperform during downtrends, offering investors lower prospective returns in exchange for lower risk.

However, history would suggest that simply isn’t the case.

Indeed, this paper from Harvard Business School suggests that not only do low Beta stocks not underperform the broader market over time – including all market conditions – they actually outperform.

A long-term study wherein the stocks with the lowest 30% of Beta scores in the US were pitted against stocks with the highest 30% of Beta scores suggested that low Beta stocks outperform by several percentage points annually.

Over time, this sort of outperformance can mean the difference between a comfortable retirement and having to continue working.

While low Beta stocks aren’t a panacea, the case for their outperformance over time – and with lower risk – is quite compelling.

How To Calculate Beta

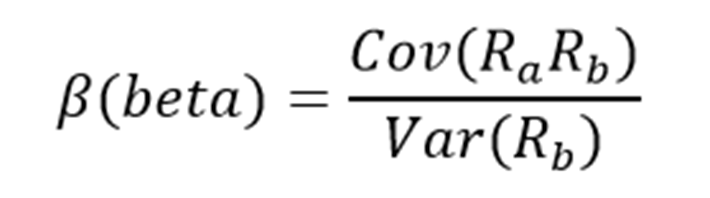

The formula to calculate a security’s Beta is fairly straightforward. The result, expressed as a number, shows the security’s tendency to move with the benchmark.

For example, a Beta value of 1.0 means that the security in question should move in lockstep with the benchmark. A Beta of 2.0 means that moves in the security should be twice as large in magnitude as the benchmark and in the same direction, while a negative Beta means that movements in the security and benchmark tend to move in opposite directions or are negatively correlated.

Related: The S&P 500 Stock With Negative Beta.

In other words, negatively correlated securities would be expected to rise when the overall market falls, or vice versa. A small value of Beta (something less than 1.0) indicates a stock that moves in the same direction as the benchmark, but with smaller relative changes.

Here’s a look at the formula:

The numerator is the covariance of the asset in question with the market, while the denominator is the variance of the market. These complicated-sounding variables aren’t actually that difficult to compute – especially in Excel.

Additionally, Beta can also be calculated as the correlation coefficient of the security in question and the market, multiplied by the security’s standard deviation divided by the market’s standard deviation.

Finally, there’s a greatly simplified way to calculate Beta by manipulating the capital asset pricing model formula (more on Beta and the capital asset pricing model later in this article).

Here’s an example of the data you’ll need to calculate Beta:

Risk-free rate (typically Treasuries at least two years out)

Your asset’s rate of return over some period (typically one year to five years)

Your benchmark’s rate of return over the same period as the asset

To show how to use these variables to do the calculation of Beta, we’ll assume a risk-free rate of 2%, our stock’s rate of return of 7% and the benchmark’s rate of return of 8%.

You start by subtracting the risk-free rate of return from both the security in question and the benchmark. In this case, our asset’s rate of return net of the risk-free rate would be 5% (7% – 2%).

The same calculation for the benchmark would yield 6% (8% – 2%).

These two numbers – 5% and 6%, respectively – are the numerator and denominator for the Beta formula. Five divided by six yields a value of 0.83, and that is the Beta for this hypothetical security.

On average, we’d expect an asset with this Beta value to be 83% as volatile as the benchmark.

Thinking about it another way, this asset should be about 17% less volatile than the benchmark while still having its expected returns correlated in the same direction.

Beta & The Capital Asset Pricing Model (CAPM)

The Capital Asset Pricing Model, or CAPM, is a common investing formula that utilizes the Beta calculation to account for the time value of money as well as the risk-adjusted returns expected for a particular asset.

Beta is an essential component of the CAPM because without it, riskier securities would appear more favorable to prospective investors. Their risk wouldn’t be accounted for in the calculation.

The CAPM formula is as follows:

The variables are defined as:

ERi = Expected return of investment

Rf = Risk-free rate

βi = Beta of the investment

ERm = Expected return of market

The risk-free rate is the same as in the Beta formula, while the Beta that you’ve already calculated is simply placed into the CAPM formula. The expected return of the market (or benchmark) is placed into the parentheses with the market risk premium, which is also from the Beta formula. This is the expected benchmark’s return minus the risk-free rate.

To continue our example, here is how the CAPM actually works:

ER = 2% + 0.83(8% – 2%)

In this case, our security has an expected return of 6.98% against an expected benchmark return of 8%. That may be okay depending upon the investor’s goals as the security in question should experience less volatility than the market thanks to its Beta of less than 1.

While the CAPM certainly isn’t perfect, it is relatively easy to calculate and gives investors a means of comparison between two investment alternatives.

Now, we’ll take a look at five stocks that not only offer investors low Beta scores, but attractive prospective returns as well.

Analysis On The Top 5 Low Beta Stocks

The following 5 low beta stocks have the lowest (but positive) Beta values, in ascending order from lowest to highest. They also pay dividends to shareholders.

We focused on Betas above 0, as we are still looking for stocks that are positively correlated with the broader market:

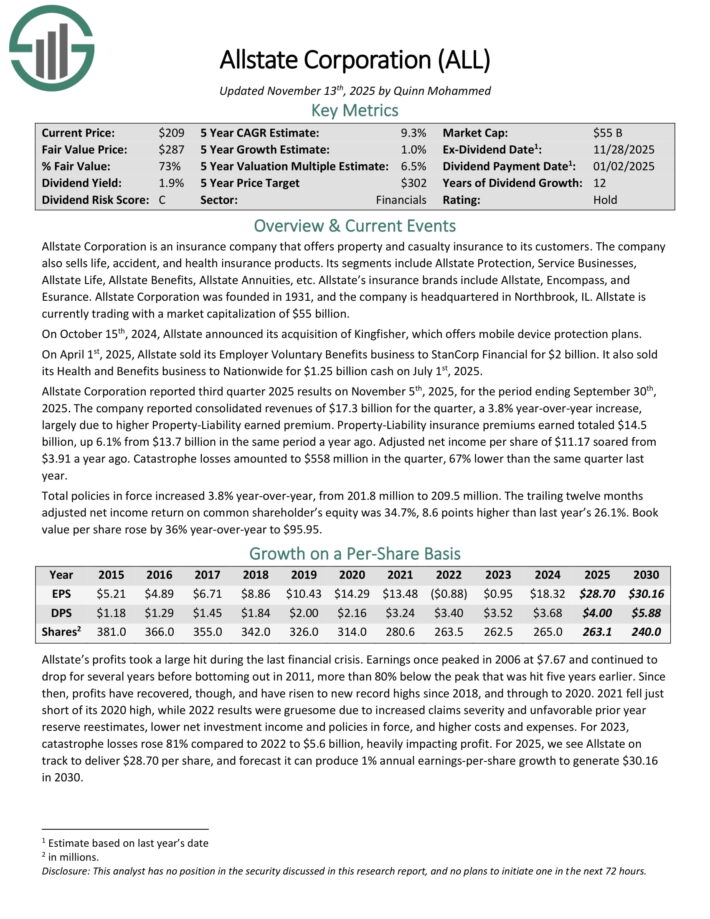

5. Allstate Corporation (ALL)

Allstate Corporation is an insurance company that offers property and casualty insurance to its customers. The company also sells life, accident, and health insurance products.

Its segments include Allstate Protection, Service Businesses, Allstate Life, Allstate Benefits, Allstate Annuities, etc. Allstate’s insurance brands include Allstate, Encompass, and Esurance.

Allstate Corporation reported third quarter 2025 results on November 5th, 2025. The company reported consolidated revenues of $17.3 billion for the quarter, a 3.8% year-over-year increase, largely due to higher Property-Liability earned premium.

Property-Liability insurance premiums earned totaled $14.5 billion, up 6.1% from $13.7 billion in the same period a year ago. Adjusted net income per share of $11.17 soared from $3.91 a year ago.

The insurance industry is not a high-growth industry, nevertheless, Allstate has managed to grow earnings successfully over the long term, with ebbs and flows over certain time periods.

The company benefits from rising interest rates, as this allows it to deploy its insurance float more profitably.

Allstate has successfully reduced its share count throughout the last decade, and it is likely that share repurchases will remain a key factor in earnings-per-share growth going forward as well.

In the last five years, the company has reduced its common shares outstanding by 4.1% annually.

Click here to download our most recent Sure Analysis report on ALL (preview of page 1 of 3 shown below):

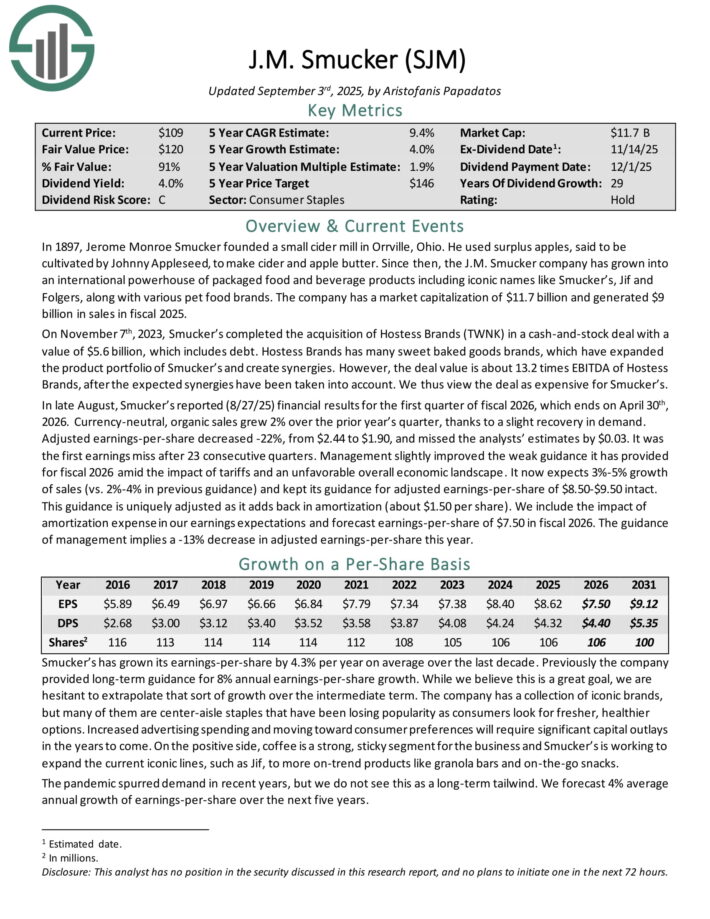

4. JM Smucker (SJM)

J.M. Smucker has grown into an international powerhouse of packaged food and beverage products including iconic names like Smucker’s, Jif and Folgers, along with various pet food brands.

In late August, Smucker’s reported (8/27/25) financial results for the first quarter of fiscal 2026, which ends on April 30th, 2026. Currency-neutral, organic sales grew 2% over the prior year’s quarter, thanks to a slight recovery in demand.

Adjusted earnings-per-share decreased -22%, from $2.44 to $1.90, and missed the analysts’ estimates by $0.03. It was the first earnings miss after 23 consecutive quarters.

Management slightly improved the weak guidance it has provided for fiscal 2026 amid the impact of tariffs and an unfavorable overall economic landscape.

It now expects 3%-5% growth of sales (vs. 2%-4% in previous guidance) and kept its guidance for adjusted earnings-per-share of $8.50-$9.50 intact. This guidance is uniquely adjusted as it adds back in amortization (about $1.50 per share).

Smucker’s iconic brands continue to enjoy recognition, but this moat is eroding somewhat as consumers look for fresher and healthier alternatives.

During the last recession, Smucker’s held up exceptionally well, growing both earnings and dividends during this time.

Click here to download our most recent Sure Analysis report on SJM (preview of page 1 of 3 shown below):

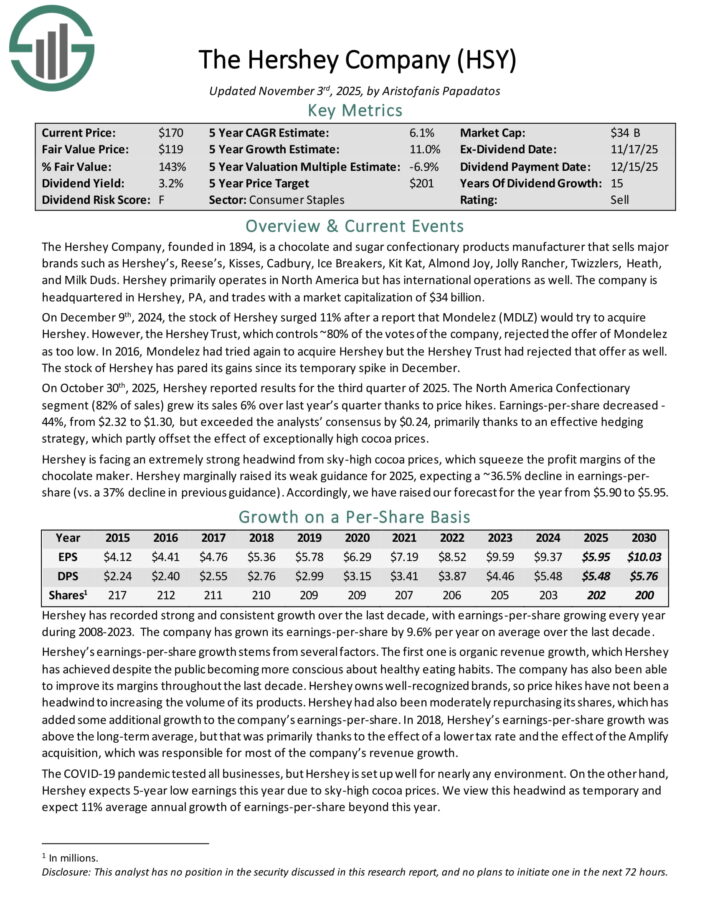

3. The Hershey Company (HSY)

The Hershey Company, founded in 1894, is a chocolate and sugar confectionary products manufacturer that sells major brands such as Hershey’s, Reese’s, Kisses, Cadbury, Ice Breakers, Kit Kat, Almond Joy, Jolly Rancher, Twizzlers, Heath, and Milk Duds. Hershey primarily operates in North America but has international operations as well.

On October 30th, 2025, Hershey reported results for the third quarter of 2025. The North America Confectionary segment (82% of sales) grew its sales 6% over last year’s quarter thanks to price hikes.

Earnings-per-share decreased 44%, from $2.32 to $1.30, but exceeded the analysts’ consensus by $0.24, primarily thanks to an effective hedging strategy, which partly offset the effect of exceptionally high cocoa prices.

Hershey is facing an extremely strong headwind from sky-high cocoa prices, which squeeze the profit margins of the chocolate maker. Hershey marginally raised its weak guidance for 2025, expecting a ~36.5% decline in earnings-per-share.

Click here to download our most recent Sure Analysis report on HSY (preview of page 1 of 3 shown below):

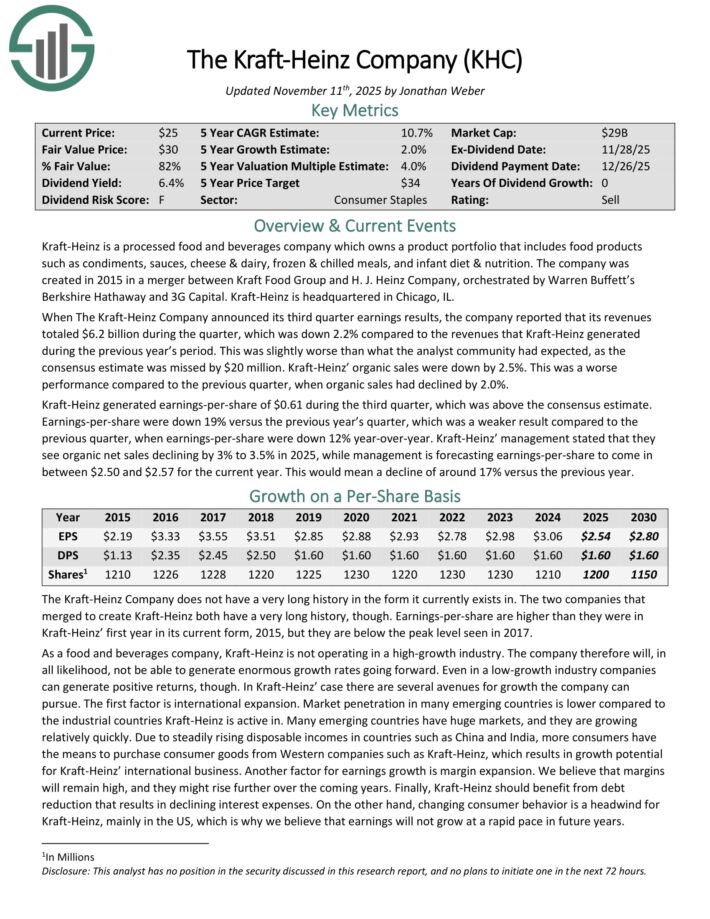

2. The Kraft-Heinz Company (KHC)

Kraft-Heinz is a processed food and beverages company which owns a product portfolio that includes food products such as condiments, sauces, cheese & dairy, frozen & chilled meals, and infant diet & nutrition.

When The Kraft-Heinz Company announced its third quarter earnings results, the company reported that its revenues totaled $6.2 billion during the quarter, which was down 2.2% compared to the revenues that Kraft-Heinz generated during the previous year’s period.

This was slightly worse than what the analyst community had expected, as the consensus estimate was missed by $20 million. Kraft-Heinz’ organic sales were down by 2.5%.

Kraft-Heinz generated earnings-per-share of $0.61 during the third quarter, which was above the consensus estimate. Earnings-per-share were down 19% versus the previous year’s quarter.

Kraft-Heinz’ management stated that they see organic net sales declining by 3% to 3.5% in 2025, while management is forecasting earnings-per-share to come in between $2.50 and $2.57 for the current year. This would mean a decline of around 17% versus the previous year.

Click here to download our most recent Sure Analysis report on KHC (preview of page 1 of 3 shown below):

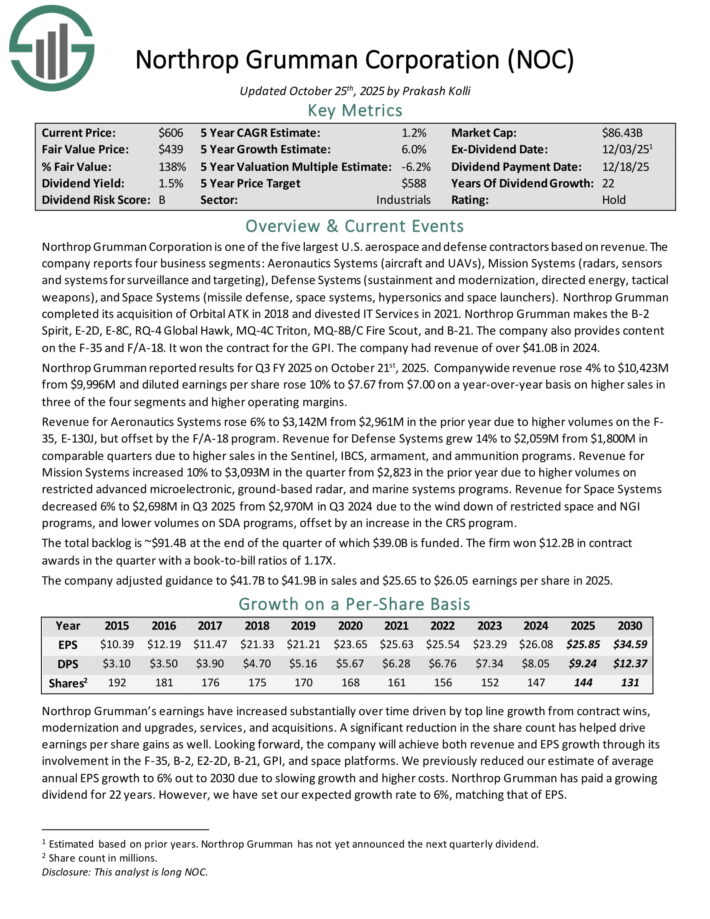

1. Northrop Grumman (NOC)

Northrop Grumman Corporation is one of the five largest U.S. aerospace and defense contractors based on revenue.

The company reports four business segments: Aeronautics Systems (aircraft and UAVs), Mission Systems (radars, sensors and systems for surveillance and targeting), Defense Systems (sustainment and modernization, directed energy, tactical weapons), and Space Systems (missile defense, space systems, hypersonics and space launchers).

Northrop Grumman makes the B-2 Spirit, E-2D, E-8C, RQ-4 Global Hawk, MQ-4C Triton, MQ-8B/C Fire Scout, and B-21. The company also provides content on the F-35 and F/A-18. It won the contract for the GPI. The company had revenue of over $41.0B in 2024.

Northrop Grumman reported results for Q3 FY 2025 on October 21st, 2025. Company-wide revenue rose 4% and diluted earnings per share rose 10% to $7.67 from $7.00 on a year-over-year basis on higher sales in three of the four segments and higher operating margins.

Revenue for Aeronautics Systems rose 6% due to higher volumes on the F-35, E-130J, but offset by the F/A-18 program. Revenue for Defense Systems grew 14% in comparable quarters due to higher sales in the Sentinel, IBCS, armament, and ammunition programs.

Revenue for Mission Systems increased 10% in the quarter due to higher volumes on restricted advanced microelectronic, ground-based radar, and marine systems programs. The company adjusted guidance to $41.7B to $41.9B in sales and $25.65 to $26.05 earnings per share in 2025.

Click here to download our most recent Sure Analysis report on NOC (preview of page 1 of 3 shown below):

Final Thoughts

Investors must take risk into account when selecting from prospective investments. After all, if two securities are otherwise similar in terms of expected returns but one offers a much lower Beta, the investor would do well to select the low Beta security as they may offer better risk-adjusted returns.

Using Beta can help investors determine which securities will produce more volatility than the broader market and which ones may help diversify a portfolio, such as the ones listed here.

The five stocks we’ve looked at not only offer low Beta scores, but they also offer attractive dividend yields. Sifting through the immense number of stocks available for purchase to investors using criteria like these can help investors find the best stocks to suit their needs.

At Sure Dividend, we often advocate for investing in companies with a high probability of increasing their dividends each and every year.

If that strategy appeals to you, it may be useful to browse through the following databases of dividend growth stocks:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

s: What Advisors Need to Know for a Smooth End of Year")

PT to , Cites Persistent Brand Advertising Headwinds")

{kind=link}