Published on March 11th, 2026 by Bob Ciura

The market is overvalued from a historical perspective. The S&P 500 Index currently trades at a Shiller PE ratio of 39, the highest level since the tech bubble.

The Shiller P/E ratio uses average earnings over the last ten years for the denominator in the P/E formula to smooth out and account for periods of temporary earnings declines.

The goal of rational investors is to maximize total return.

Therefore, we recommend investors buy-and-hold quality dividend stocks such as the Dividend Aristocrats, which are those companies that have raised their dividends for at least 25 consecutive years.

Even better, investors can buy the Dividend Aristocrats when they are undervalued.

You can download the full list of Dividend Aristocrats by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

In addition to analyzing a stock’s future growth prospects, its valuation is equally important. When market sentiment turns negative for a stock due to a temporary headwind, its valuation (measured by the P/E ratio) may become too cheap.

When the headwind subsides, the valuation of the stock is likely to revert to normal levels.

As a result, investors could potentially earn significant total returns by purchasing quality dividend growth stocks, when they are undervalued.

Therefore, this article will discuss the 10 Dividend Aristocrats with the lowest P/E ratios right now.

Table of Contents

The table of contents below allows for easy navigation. The stocks are listed by P/E ratio, from lowest to highest.

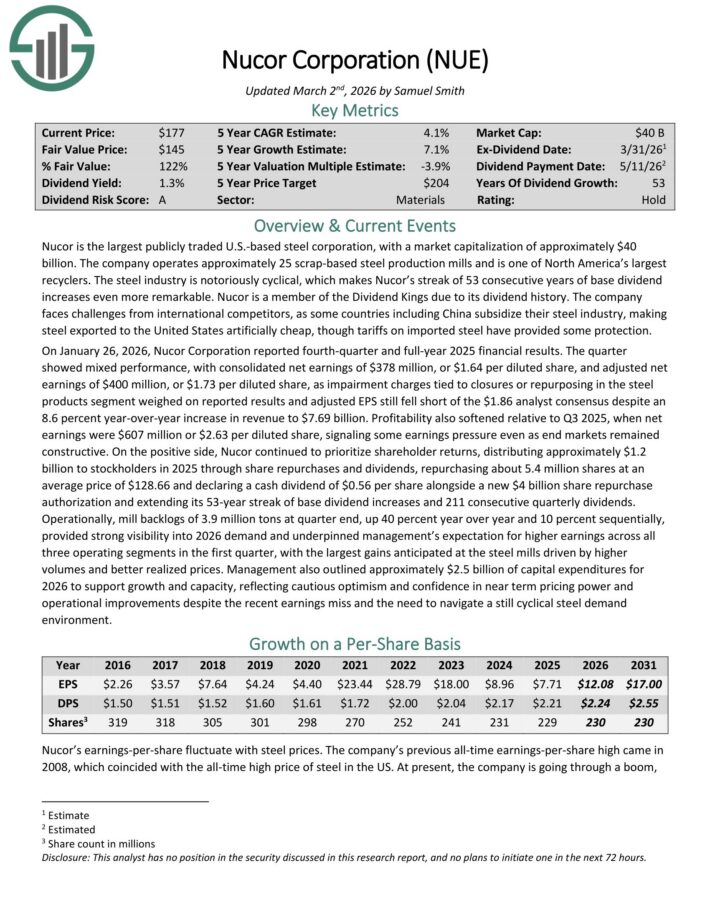

Undervalued Dividend Aristocrat #10: Nucor Corp. (NUE)

Nucor is the largest publicly traded U.S.-based steel corporation. The company operates approximately 25 scrap-based steel production mills and is one of North America’s largest recyclers.

On January 26, 2026, Nucor Corporation reported fourth-quarter and full-year 2025 financial results. The quarter showed mixed performance, with consolidated net earnings of $378 million, or $1.64 per diluted share, and adjusted net earnings of $400 million, or $1.73 per diluted share.

Impairment charges tied to closures or repurposing in the steel products segment weighed on reported results and adjusted EPS fell short of the $1.86 analyst consensus, despite an 8.6 percent year-over-year increase in revenue to $7.69 billion.

Profitability also softened relative to Q3 2025, when net earnings were $607 million or $2.63 per diluted share, signaling some earnings pressure even as end markets remained constructive.

Nucor continued to prioritize shareholder returns, distributing approximately $1.2 billion to stockholders in 2025 through share repurchases and dividends, repurchasing about 5.4 million shares at an average price of $128.66.

The company also declared a cash dividend of $0.56 per share alongside a new $4 billion share repurchase authorization and extended its 53-year streak of base dividend increases and 211 consecutive quarterly dividends.

Click here to download our most recent Sure Analysis report on NUE (preview of page 1 of 3 shown below):

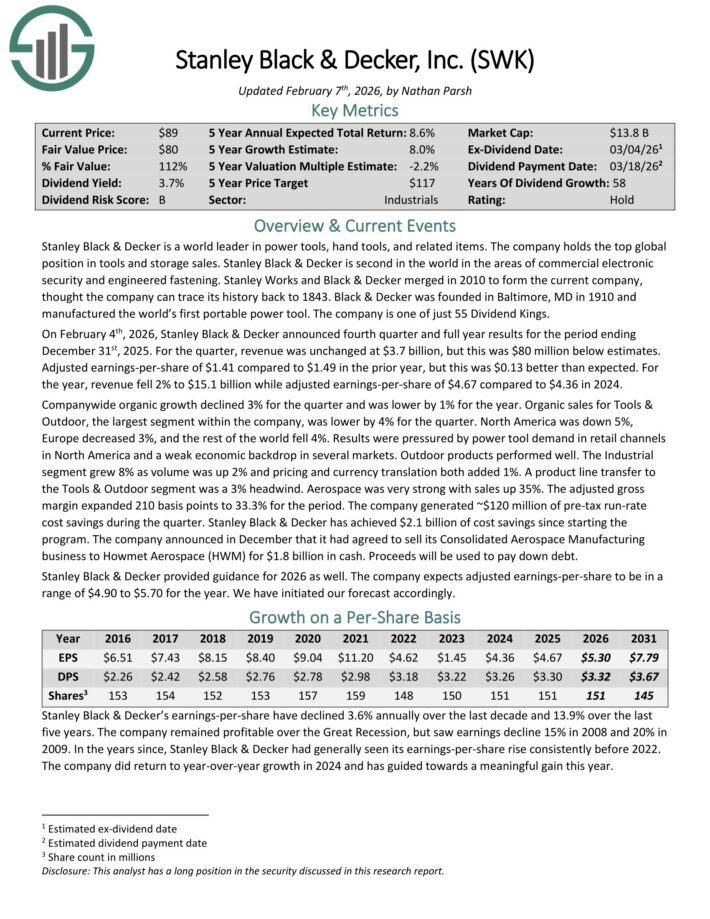

Undervalued Dividend Aristocrat #9: Stanley Black & Decker (SWK)

Stanley Black & Decker is a world leader in power tools, hand tools, and related items. The company holds the top global position in tools and storage sales.

Stanley Black & Decker is second in the world in the areas of commercial electronic security and engineered fastening. The company is composed of three segments: tools & outdoor, and industrial.

On February 4th, 2026, Stanley Black & Decker announced fourth quarter and full year results. For the quarter, revenue was unchanged at $3.7 billion, but this was $80 million below estimates.

Adjusted earnings-per-share of $1.41 compared to $1.49 in the prior year, but this was $0.13 better than expected. For the year, revenue fell 2% to $15.1 billion while adjusted earnings-per-share of $4.67 compared to $4.36 in 2024.

Company-wide organic growth declined 3% for the quarter and was lower by 1% for the year. Organic sales for Tools & Outdoor, the largest segment within the company, was lower by 4% for the quarter.

North America was down 5%, Europe decreased 3%, and the rest of the world fell 4%. Results were pressured by power tool demand in retail channels in North America and a weak economic backdrop in several markets.

Click here to download our most recent Sure Analysis report on SWK (preview of page 1 of 3 shown below):

Undervalued Dividend Aristocrat #8: Kimberly-Clark Corp. (KMB)

The Kimberly-Clark Corporation is a global consumer products company that operates in 175 countries and sells disposable consumer goods, including paper towels, diapers, and tissues.

It operates through two segments that each house many popular brands: Personal Care Segment (Huggies, Pull-Ups, Kotex, Depend, Poise) and the Consumer Tissue segment (Kleenex, Scott, Cottonelle, and Viva), generating about $20 billion in annual revenue.

Kimberly-Clark posted third quarter earnings on October 30th, 2025, and results were better than expected on both the top and bottom lines.

Adjusted earnings-per-share came to $1.82, which was seven cents ahead of estimates. Revenue was flat year-over-year at $4.15 billion, but did best estimates by $50 million.

Sales included negative impacts of about 2.2% from the exit of the private label diaper business in the US. Organic sales were up 2.5%, which was driven by a 2.4% gain in volume, while portfolio mix and price were flat.

Gross margin was 36.8% of revenue on an adjusted basis, off 170 basis points year-over-year. This reflected strong productivity gains that were more than offset by unfavorable pricing net of cost inflation.

Operating profit was $683 million on an adjusted basis, driven by lower marketing and R&D costs, as well as efficiency efforts. Net interest expense was $59 million, up from $49 million a year ago.

We now see $7.50 in adjusted earnings-per-share for this year, which would be the highest since 2020, if achieved. Separately, Kimberly-Clark announced its intention to buy Kenvue (KVUE) for $48.7 billion in a cash and stock deal.

Click here to download our most recent Sure Analysis report on KMB (preview of page 1 of 3 shown below):

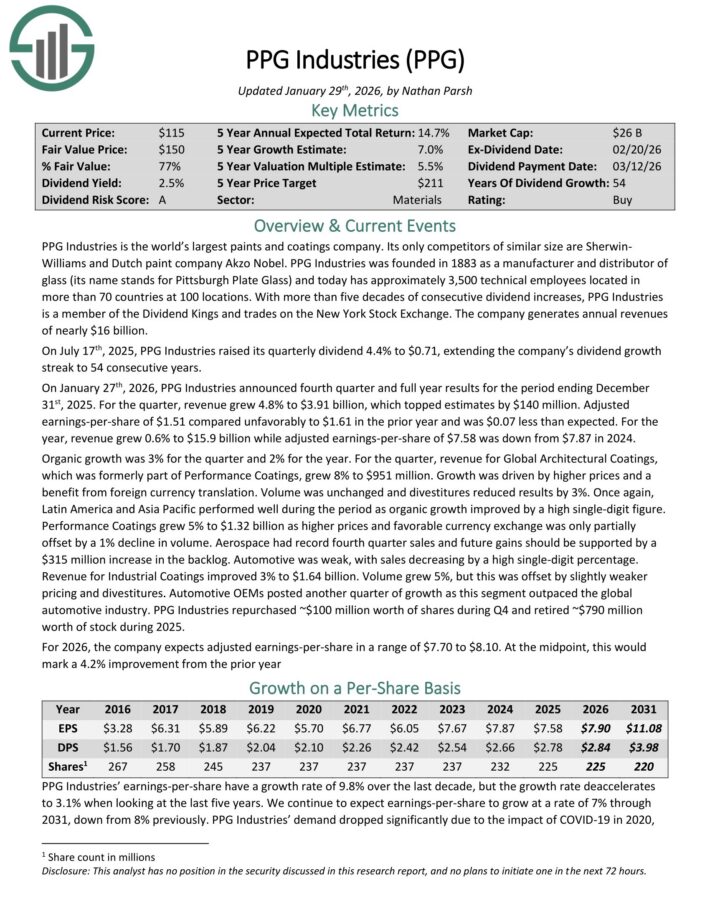

Undervalued Dividend Aristocrat #7: PPG Industries (PPG)

PPG Industries is the world’s largest paints and coatings company. Its only competitors of similar size are Sherwin-Williams and Dutch paint company Akzo Nobel.

On January 27th, 2026, PPG Industries announced fourth quarter and full year results. For the quarter, revenue grew 4.8% to $3.91 billion, which topped estimates by $140 million. Adjusted earnings-per-share of $1.51 compared unfavorably to $1.61 in the prior year and was $0.07 less than expected.

For the year, revenue grew 0.6% to $15.9 billion while adjusted earnings-per-share of $7.58 was down from $7.87 in 2024. Organic growth was 3% for the quarter and 2% for the year.

For the quarter, revenue for Global Architectural Coatings, which was formerly part of Performance Coatings, grew 8% to $951 million.

Growth was driven by higher prices and a benefit from foreign currency translation. Volume was unchanged and divestitures reduced results by 3%.

Once again, Latin America and Asia Pacific performed well during the period as organic growth improved by a high single-digit figure.

Performance Coatings grew 5% to $1.32 billion as higher prices and favorable currency exchange was only partially offset by a 1% decline in volume.

Aerospace had record fourth quarter sales and future gains should be supported by a $315 million increase in the backlog. Automotive was weak, with sales decreasing by a high single-digit percentage.

Revenue for Industrial Coatings improved 3% to $1.64 billion. Volume grew 5%, but this was offset by slightly weaker pricing and divestitures. Automotive OEMs posted another quarter of growth as this segment outpaced the global automotive industry.

PPG Industries repurchased ~$100 million worth of shares during Q4 and retired ~$790 million worth of stock during 2025.

Click here to download our most recent Sure Analysis report on PPG (preview of page 1 of 3 shown below):

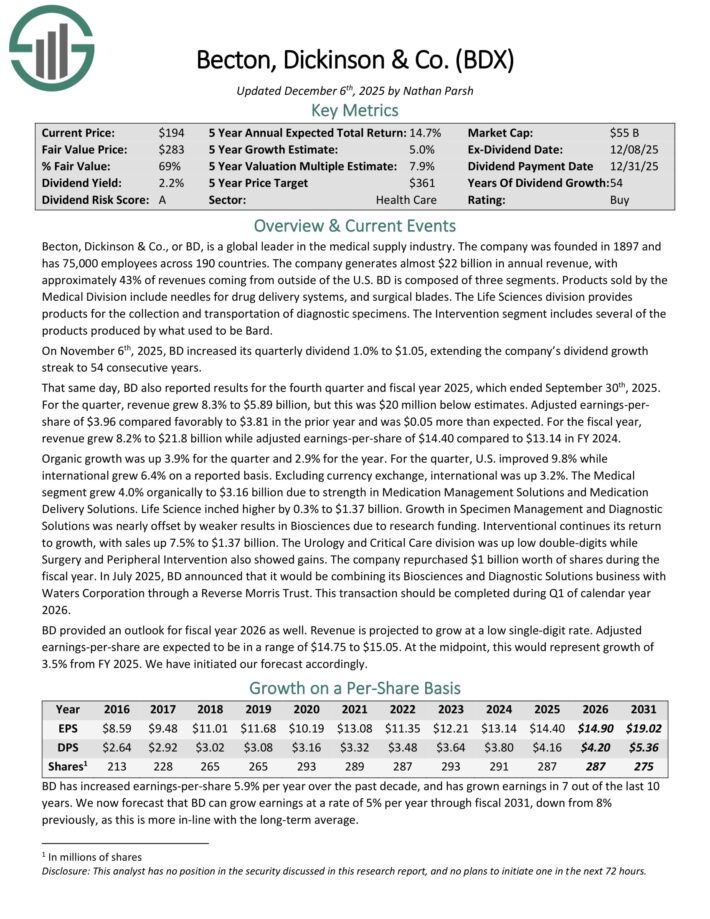

Undervalued Dividend Aristocrat #6: Becton, Dickinson & Co. (BDX)

Becton, Dickinson & Co. is a global leader in the medical supply industry. The company was founded in 1897 and has 75,000 employees across 190 countries.

The company generates about $20 billion in annual revenue, with approximately 43% of revenues coming from outside of the U.S.

On November 6th, 2025, BD increased its quarterly dividend 1.0% to $1.05, extending the company’s dividend growth streak to 54 consecutive years.

BD also reported results for the fourth quarter and fiscal year 2025, which ended September 30th, 2025. For the quarter, revenue grew 8.3% to $5.89 billion, but this was $20 million below estimates.

Adjusted earnings-per-share of $3.96 compared favorably to $3.81 in the prior year and was $0.05 more than expected. For the fiscal year, revenue grew 8.2% to $21.8 billion while adjusted earnings-per-share of $14.40 compared to $13.14 in FY 2024.

BD provided an outlook for fiscal year 2026 as well. Revenue is projected to grow at a low single-digit rate. Adjusted earnings-per-share are expected to be in a range of $14.75 to $15.05.

At the midpoint, this would represent growth of 3.5% from FY 2025.

Click here to download our most recent Sure Analysis report on BDX (preview of page 1 of 3 shown below):

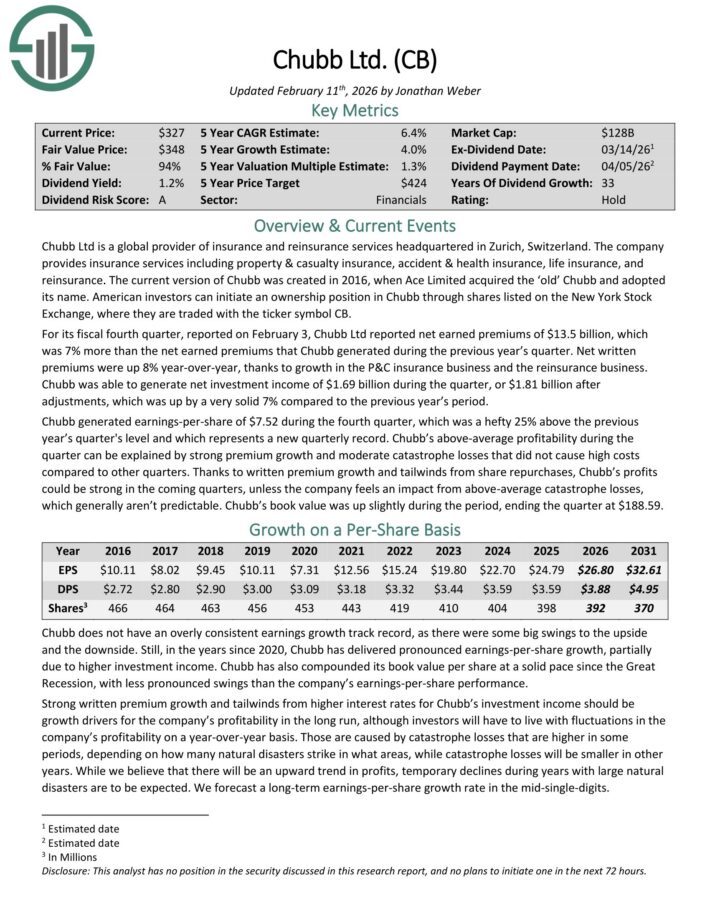

Undervalued Dividend Aristocrat #5: Chubb Ltd. (CB)

Chubb Ltd is a global provider of insurance and reinsurance services headquartered in Zurich, Switzerland. The company provides insurance services including property & casualty insurance, accident & health insurance, life insurance, and reinsurance.

For its fiscal fourth quarter, reported on February 3, Chubb Ltd reported net earned premiums of $13.5 billion, which was 7% more than the net earned premiums that Chubb generated during the previous year’s quarter.

Net written premiums were up 8% year-over-year, thanks to growth in the P&C insurance business and the reinsurance business.

Chubb was able to generate net investment income of $1.69 billion during the quarter, or $1.81 billion after adjustments, which was up by a very solid 7% compared to the previous year’s period.

Chubb generated earnings-per-share of $7.52 during the fourth quarter, which was a hefty 25% above the previous year’s quarter’s level and which represents a new quarterly record.

Chubb’s above-average profitability during the quarter can be explained by strong premium growth and moderate catastrophe losses that did not cause high costscompared to other quarters.

Chubb’s book value was up slightly during the period, ending the quarter at $188.59.

Click here to download our most recent Sure Analysis report on CB (preview of page 1 of 3 shown below):

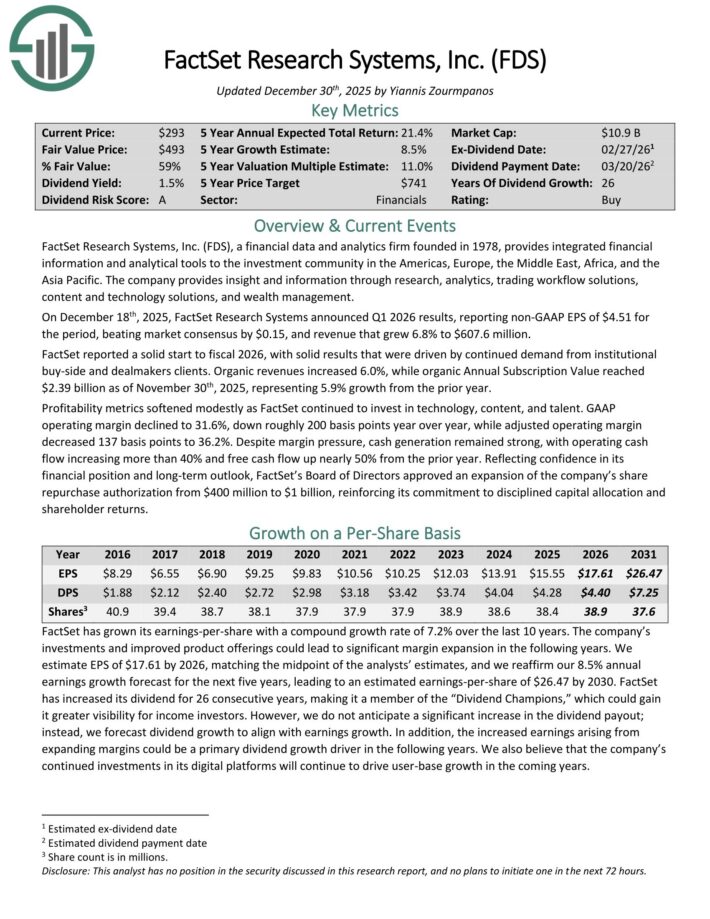

Undervalued Dividend Aristocrat #4: Factset Research Systems (FDS)

FactSet Research Systems, a financial data and analytics firm founded in 1978, provides integrated financial information and analytical tools to the investment community in the Americas, Europe, the Middle East, Africa, and Asia-Pacific.

The company provides insight and information through research, analytics, trading workflow solutions, content and technology solutions, and wealth management.

On December 18th, 2025, FactSet Research Systems announced Q1 2026 results, reporting non-GAAP EPS of $4.51 for the period, beating market consensus by $0.15, and revenue that grew 6.8% to $607.6 million.

FactSet reported a solid start to fiscal 2026, with solid results that were driven by continued demand from institutional buy-side and dealmakers clients.

Organic revenues increased 6.0%, while organic Annual Subscription Value reached $2.39 billion as of November 30th, 2025, representing 5.9% growth from the prior year.

Profitability metrics softened modestly as FactSet continued to invest in technology, content, and talent. GAAP operating margin declined to 31.6%, down roughly 200 basis points year over year, while adjusted operating margin decreased 137 basis points to 36.2%.

Despite margin pressure, cash generation remained strong, with operating cash flow increasing more than 40% and free cash flow up nearly 50% from the prior year.

Reflecting confidence in its financial position and long-term outlook, FactSet’s Board of Directors approved an expansion of the company’s share repurchase authorization from $400 million to $1 billion.

Click here to download our most recent Sure Analysis report on FDS (preview of page 1 of 3 shown below):

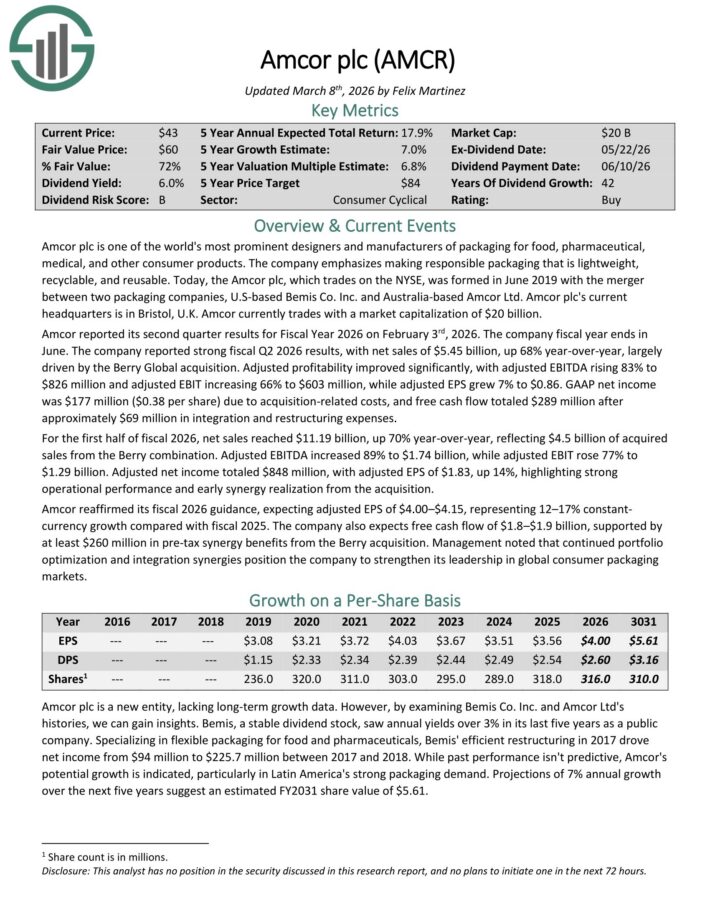

Undervalued Dividend Aristocrat #3: Amcor plc (AMCR)

Amcor plc is one of the world’s most prominent designers and manufacturers of packaging for food, pharmaceutical, medical, and other consumer products. The company emphasizes making responsible packaging that is lightweight, recyclable, and reusable.

Amcor reported its second quarter results for Fiscal Year 2026 on February 3rd, 2026. The company reported strong fiscal Q2 2026 results, with net sales of $5.45 billion, up 68% year-over-year, largely driven by the Berry Global acquisition.

Adjusted profitability improved significantly, with adjusted EBITDA rising 83% to $826 million and adjusted EBIT increasing 66% to $603 million, while adjusted EPS grew 7% to $0.86.

GAAP net income was $177 million ($0.38 per share) due to acquisition-related costs, and free cash flow totaled $289 million after approximately $69 million in integration and restructuring expenses.

For the first half of fiscal 2026, net sales reached $11.19 billion, up 70% year-over-year, reflecting $4.5 billion of acquired sales from the Berry combination.

Adjusted EBITDA increased 89% to $1.74 billion, while adjusted EBIT rose 77% to $1.29 billion. Adjusted net income totaled $848 million, with adjusted EPS of $1.83, up 14%, highlighting strong operational performance and early synergy realization from the acquisition.

Amcor reaffirmed its fiscal 2026 guidance, expecting adjusted EPS of $4.00–$4.15, representing 12–17% constant currency growth compared with fiscal 2025.

The company also expects free cash flow of $1.8–$1.9 billion, supported by at least $260 million in pre-tax synergy benefits from the Berry acquisition.

Click here to download our most recent Sure Analysis report on AMCR (preview of page 1 of 3 shown below):

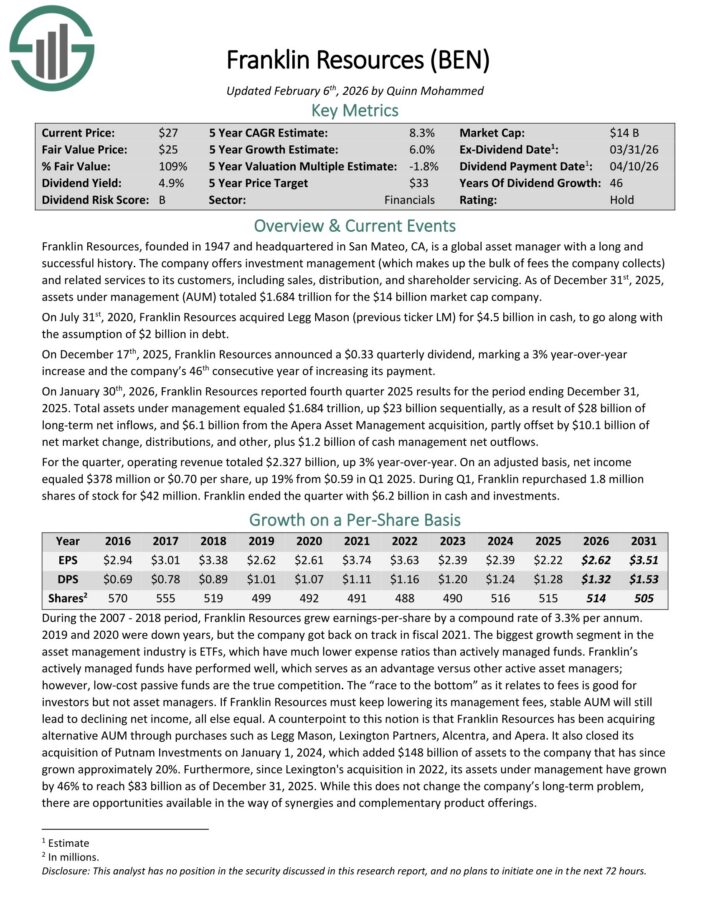

Undervalued Dividend Aristocrat #2: Franklin Resources (BEN)

Franklin Resources is a global asset manager that offers investment management (which makes up the bulk of fees the company collects) and related services to its customers, including sales, distribution, and shareholder servicing.

As of December 31st, 2025, assets under management (AUM) totaled $1.684 trillion.

On December 17th, 2025, Franklin Resources announced a $0.33 quarterly dividend, marking a 3% year-over-year increase and the company’s 46th consecutive year of increasing its payment.

On January 30th, 2026, Franklin Resources reported fourth quarter 2025 results for the period ending December 31, 2025.

Total assets under management equaled $1.684 trillion, up $23 billion sequentially, as a result of $28 billion of long-term net inflows, and $6.1 billion from the Apera Asset Management acquisition, partly offset by $10.1 billion of net market change, distributions, and other, plus $1.2 billion of cash management net outflows.

For the quarter, operating revenue totaled $2.327 billion, up 3% year-over-year. On an adjusted basis, net income equaled $378 million or $0.70 per share, up 19% from $0.59 in Q1 2025.

During Q1, Franklin repurchased 1.8 million shares of stock for $42 million. Franklin ended the quarter with $6.2 billion in cash and investments.

Click here to download our most recent Sure Analysis report on BEN (preview of page 1 of 3 shown below):

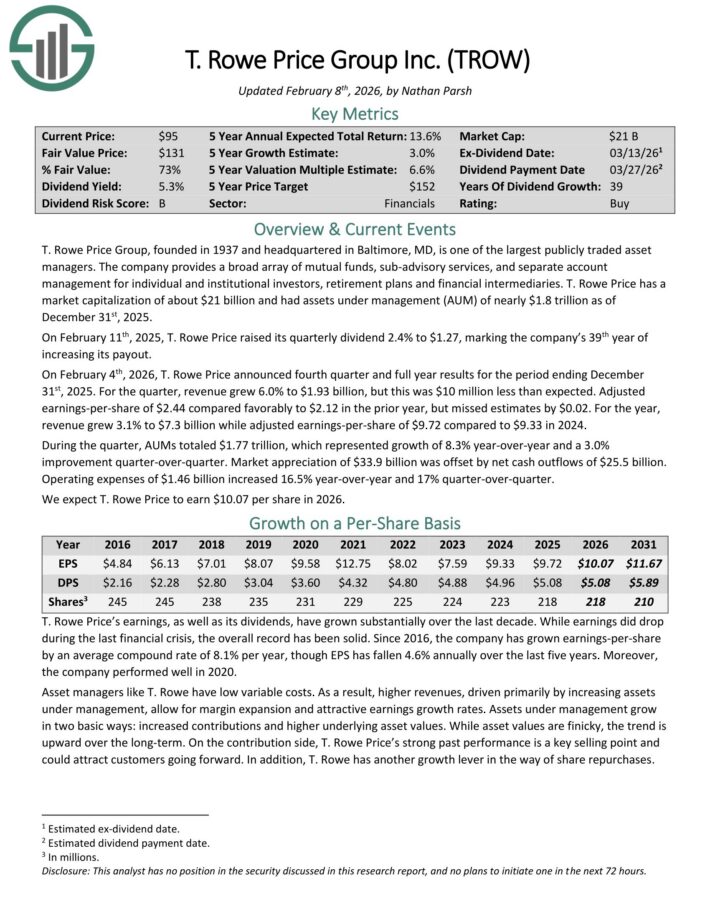

Undervalued Dividend Aristocrat #1: T. Rowe Price Group (TROW)

T. Rowe Price Group is one of the largest publicly traded asset managers. The company provides a broad array of mutual funds, sub-advisory services, and separate account management for individual and institutional investors, retirement plans and financial intermediaries.

T. Rowe Price had assets under management (AUM) of nearly $1.8 trillion as of December 31st, 2025.

On February 11th, 2025, T. Rowe Price raised its quarterly dividend 2.4% to $1.27, marking the company’s 39th year of increasing its payout.

On February 4th, 2026, T. Rowe Price announced fourth quarter and full year results for the period ending December 31st, 2025.

For the quarter, revenue grew 6.0% to $1.93 billion, but this was $10 million less than expected. Adjusted earnings-per-share of $2.44 compared favorably to $2.12 in the prior year, but missed estimates by $0.02.

For the year, revenue grew 3.1% to $7.3 billion while adjusted earnings-per-share of $9.72 compared to $9.33 in 2024. During the quarter, AUMs totaled $1.77 trillion, which represented growth of 8.3% year-over-year and a 3.0% improvement quarter-over-quarter.

Market appreciation of $33.9 billion was offset by net cash outflows of $25.5 billion. Operating expenses of $1.46 billion increased 16.5% year-over-year and 17% quarter-over-quarter.

Click here to download our most recent Sure Analysis report on TROW (preview of page 1 of 3 shown below):

Additional Reading

The following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

{kind=link}