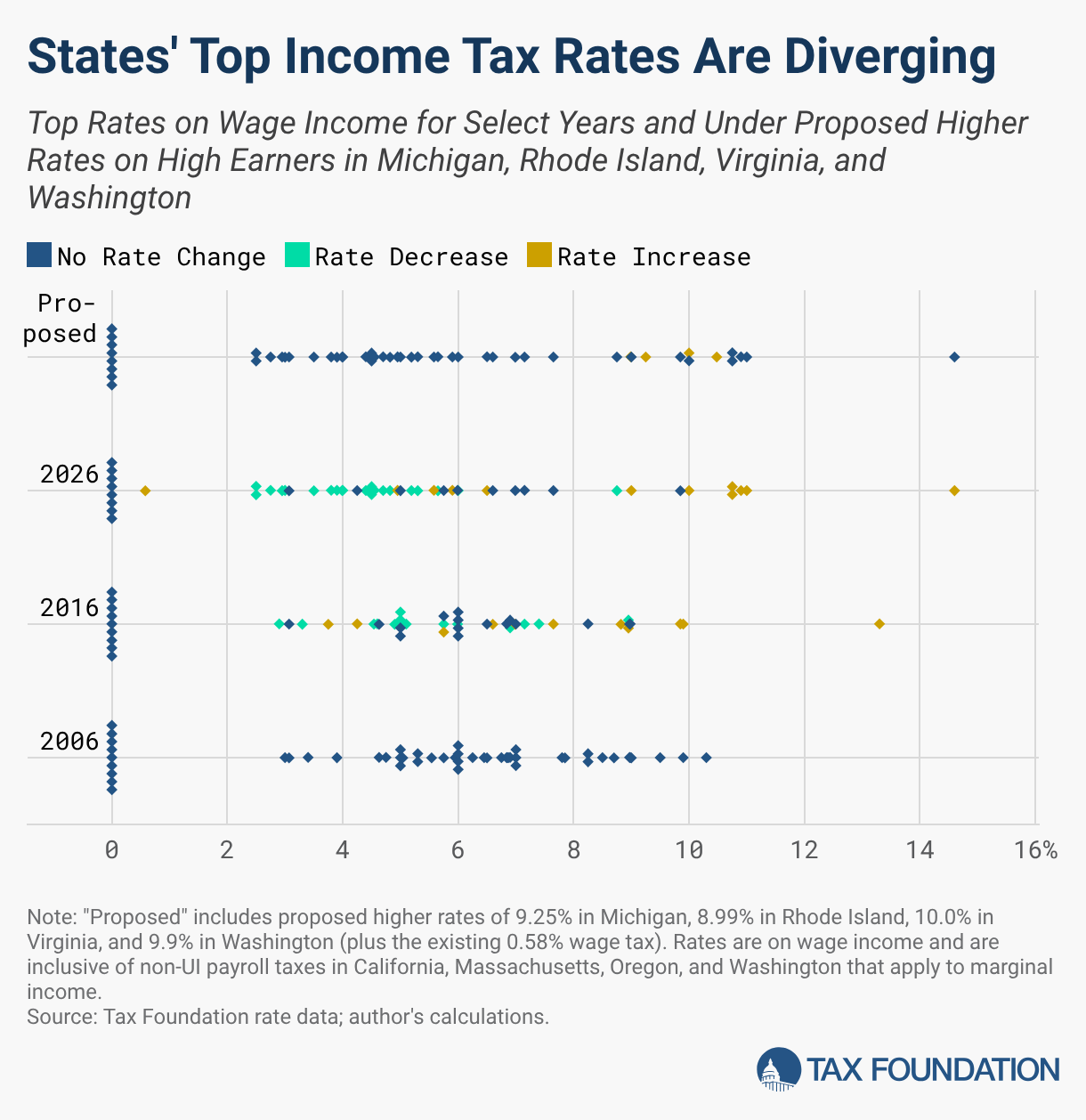

There was a time not too long ago when it was possible to speak of a “typical” state income tax with a top rate of about 6 percent. That is no longer the case. Today, far more states prioritize low, competitive rates, whereas a smaller number have abandoned the middle for much higher rates.

Two decades ago, 21 states had top rates between 5 and 7 percent. Today, there are 12. In 2006, 15 states had rates below 5 percent (including those with no taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. on wage income); now it’s 26. In 2006, only one state had a double-digit top rate, whereas six do today—a count that could increase under pending legislation.

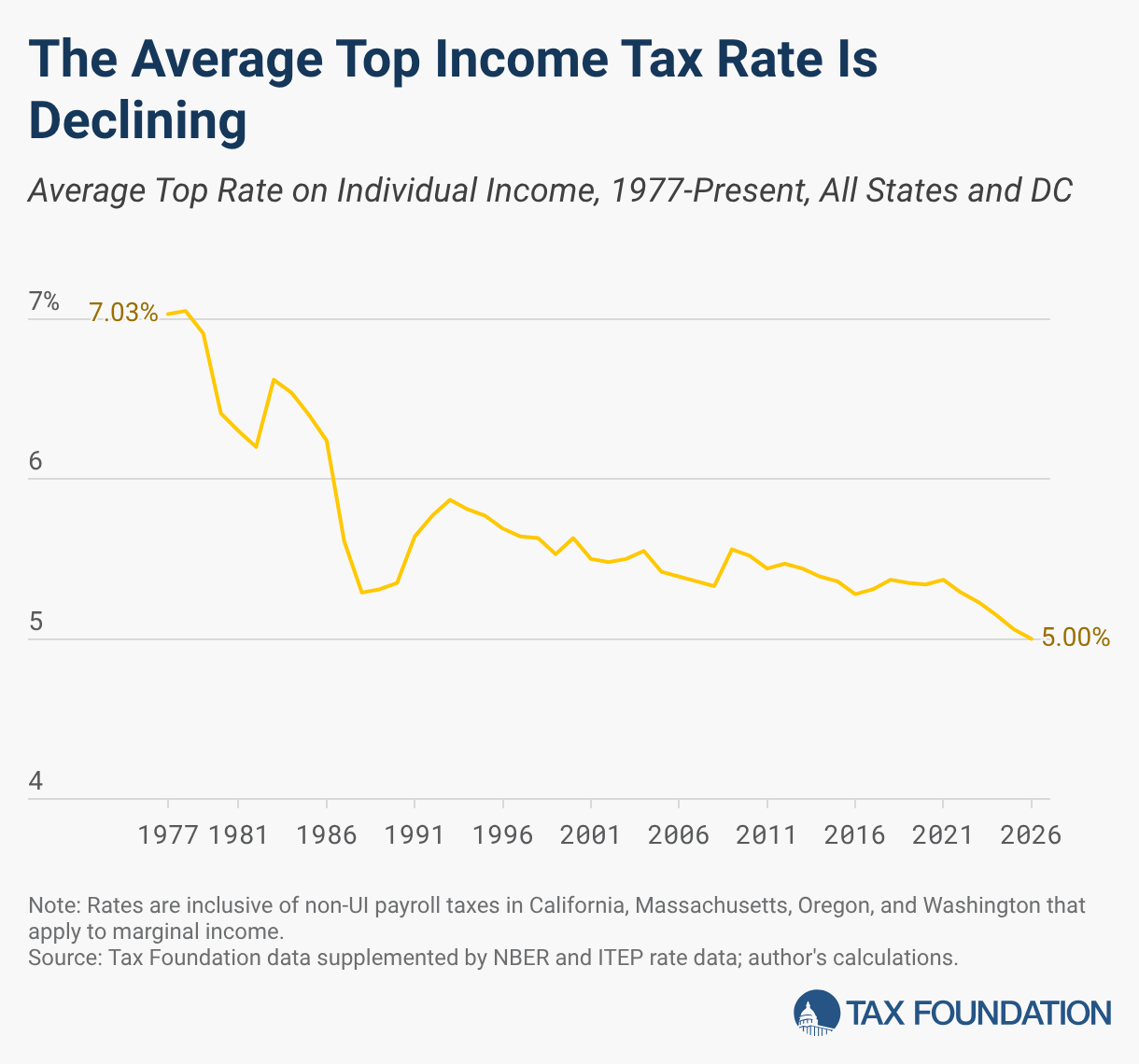

Twenty-three states have reduced their top marginal income tax rates since 2021, while six states and the District of Columbia have raised them (counting two that imposed uncapped wage taxes). Both the average and median top rate on wage income are now 5.0 percent, with recent cuts accelerating a trend of rate reductions dating back three decades.

Base-broadening provisions of the Tax Cuts and Jobs Act (2017) enabled some of these rate reductions. Absent rate cuts, that legislation—a tax cut at the federal level, with a combination of base broadening and federal rate reductions—yielded a substantial net tax increase at the state level, to which many states eventually responded with partially offsetting rate reductions.

But 2021 marked a significant pivot toward tax competitiveness, following closely on the heels of a movement for higher taxes on high earners that gained traction in the late 2010s. The pandemic and years of robust revenue growth paused some states’ deliberations on tax hikes on high earners, but those proposals have returned in force in 2026.

Essentially, then, we are witnessing two opposite movements: in some states, concerted efforts to raise taxes on high earners, and in many others, a strong focus on cutting rates and prioritizing greater tax competitiveness.

The chart below shows every state’s top rate on wage income in 2006, 2016, and 2026, along with a line incorporating proposed rate increases in Michigan (4.25 to 9.25 percent), Rhode Island (5.99 to 8.99 percent), Virginia (5.75 to 10.0 percent), and Washington (a 0.58 percent wage tax to a 9.99 percent tax on high earners plus the existing wage tax). A significant clustering of top rates between 4.63 and 7.0 percent in 2006 is followed by dispersion, with most states’ top rates declining while a few states’ rates increase dramatically.

This divergence increases the risk for high-tax states. Not only are their rates far higher than the norm for recent decades, but these high rates are set against a backdrop of rate relief elsewhere, and in an environment of increasing mobility for individuals and businesses alike. Taxpayers seeking to avoid high taxes or to secure jobs and opportunities that tend to flow to lower-tax environments have more options than ever before and greater incentives to move due to the growing divergence.

Moving involves friction, but it becomes more attractive when tax rates are unusually high relative to alternatives (and when those high taxes undercut local job opportunities), and it becomes much easier to move when there are many lower-tax options. States like Florida and Texas continue to attract new residents, but the growing number of states with competitive income tax rates provides additional options that could accelerate outmigration from high-tax states.

Lawmakers in many states continue to pursue additional income tax relief, while their counterparts elsewhere pursue the opposite goal. The result could be an increasingly bimodal rate distribution, in which it makes less and less sense to speak of a “typical” rate, only of low or high rates.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

Share this article

Q4 2025 Earnings Call Transcript")

Shares Fall 7.5% to .40 on Sector Weakness")

{kind=link}