Dear Chair Tridico and Distinguished Members of the FISC Subcommittee,

Thank you for the opportunity to discuss the taxation of ultra-high-net-worth individuals. My name is Michael Christl, and I am Research Fellow at Tax Foundation Europe.

I’d like to start by pointing out a great irony. Here in Europe, we have a long history full of important lessons. And we take learning from those lessons seriously. That is, after all, why we created the European Union: we learned that life was better when we worked together, rather than being at perpetual war. European governments learned how to create some of the most redistributive fiscal systems in the world.

However, when it comes to wealth taxes, some argue that we should ignore history. I disagree.

Since 1965, thirteen OECD countries have imposed a net wealth taxA wealth tax is imposed on an individual’s net wealth, or the market value of their total owned assets minus liabilities. A wealth tax can be narrowly or widely defined, and depending on the definition of wealth, the base for a wealth tax can vary.. However, by now, that number has dropped to 4. These repeals didn’t happen because the policies were so successful at generating revenue and solving inequality. They were changed because they didn’t work.

The question for policymakers is why, and what can we learn from our history. In my testimony, I will focus on four main issues with wealth taxes and conclude with two recommendations.

Revenue Expectations Are Overestimated

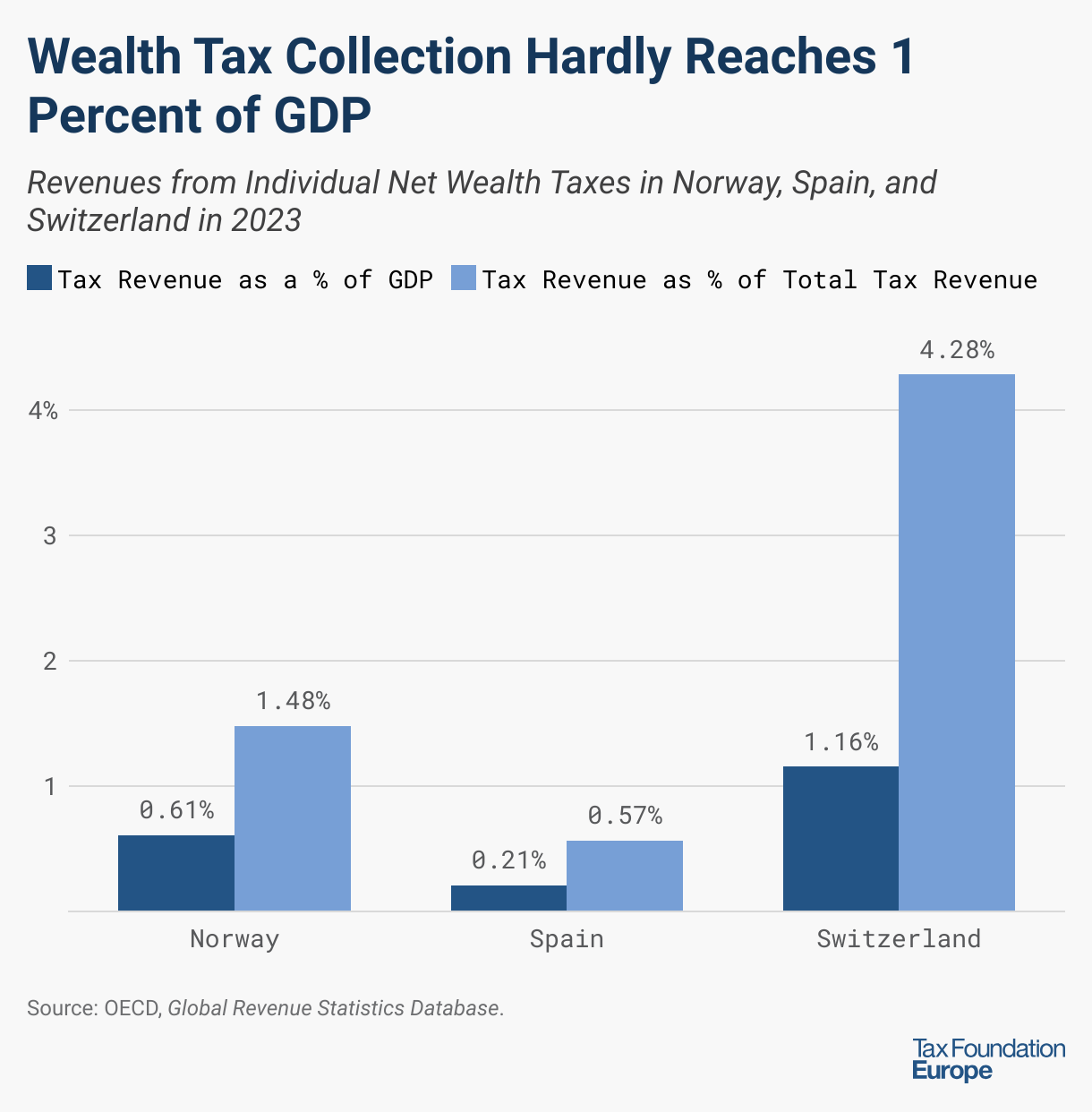

Let’s begin with a simple question: Do wealth taxes raise much money? Empirically, the answer is no. Before its 2017 repeal, the French wealth tax generated less than 0.2 percent of GDP. The current Spanish wealth tax doesn’t generate much more in GDP terms than that either. This shouldn’t be a surprise given that wealth taxes erode their own, usually very narrow base. Mobile individuals can (and do) restructure and reallocate their wealth to minimize liability. Additionally, net-wealth taxes reduce the base of broader-based taxes on income, payroll, and consumption. So, while theoretical estimates may promise billions, 60 years of real-world experience have shown that actual net-revenue is often a fraction of projections.

They Create Economic Inefficiencies and Negative Growth Effects

Second, wealth taxes are highly distortionary and are imposed on an asset’s value, irrespective of economic returns. This can generate double or even triple taxation. For safe investments like bonds or bank deposits, a wealth tax of 2 or 3 percent may confiscate all interest earnings, leaving no increase in savings over time. The problem is exacerbated in an inflationary environment. This leads to a disincentive to save and, in the medium term, a reduction in capital accumulation.

In simple terms, taxing the stock of capital slows the very investment and innovation we depend on for long-run prosperity. A recent OECD report concludes similarly: “from both an efficiency and equity perspective, there are limited arguments for having a net wealth tax in addition to broad-based personal capital income taxes and well-designed inheritance and gift taxes.”

There Are Usually Strong Behavioral Responses

Third, we must account for behavioral responses. Before repealing its wealth tax, France saw a significant outflow of millionaires; an estimated 12,000 people left in 2016 alone. Recently, this year’s Nobel laureate Philippe Aghion cautioned that the proposed “Zucman tax” risks penalising entrepreneurship and weakening high-growth start-ups, something that would hurt the EU’s competitiveness. The expected revenue is substantially overestimated, with realistic yields far below headline claims. I share this view: taxing unrealised business wealth would drain liquidity from innovative firms while generating much less revenue than proponents suggest.

In 2022, Norway raised its wealth tax and quickly saw an exodus of high-net-worth individuals to countries like Switzerland and the UK. These are not just anecdotes. These responses undermine the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates., and create unintended spillovers: lower investment, job losses, and, as mentioned, net revenue declines. Princeton economist Christine Blandhol estimates that long-run output in Norway could fall by 1.3 percent as a result.

Administrative Complexity

Finally, let’s consider administration and enforcement. Most wealth among the very rich is not held in cash or shares. It’s in private businesses, real estate, art, trusts—all of which are illiquid and difficult to value.

That creates a huge enforcement challenge. Annual valuations are time-consuming, expensive, and prone to legal disputes, as we’ve seen in the Netherlands, Germany, and Spain. Moreover, the wealthiest individuals often have access to sophisticated tax planners, further undermining enforcement equity. In some cases, compliance costs and enforcement burdens outweigh the revenue collected. That’s not a recipe for efficient tax policy.

What Could Be Done Instead?

Instead of pursuing new net wealth taxes, policymakers should focus on making the current tax system more efficient, transparent, and enforceable. A streamlined tax system with fewer exemptions and special regimes can achieve broader equity and improve compliance. Furthermore, enhanced information exchange between tax authorities, better asset tracking, and digital reporting systems can curb evasion without introducing new taxes.

Finally, if extra revenue is needed, policymakers should focus on efficient policy designs with immobile bases such as broad-based consumption taxes or real property taxes that fall on land. After 60 years of evidence, it is clear that wealth taxes are not the solution.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

")

{kind=link}