Public health organizations continue to push for excise taxes on sugar-sweetened beverages (SSBs). The World Health Organization, for example, recently announced its 3 by 25 Initiative, an effort to increase consumer-facing prices of tobacco, alcohol, and sugary drinks by at least 50 percent by 2035. Several governments around the globe already levy an excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. on sugary beverages. In today’s post, we examine the effects of the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. in Catalonia, Spain.

The goal of SSB taxes is to curb the growing obesity epidemic. In theory, the pathway to achieving that outcome appears rather straightforward. Sugary beverages contain easy-to-consume calories. If those calories were removed from a diet, holding everything else constant, less caloric consumption would translate into less body weight. The lower body weight and decreased sugar consumption would alleviate some strain on public health institutions and decrease the expenditures needed to address the problems with obesity and diabetes.

In reality, the causal chain needed to connect less SSB consumption to improved health outcomes often contains broken links. We previously outlined the steps necessary to translate an SSB tax into improved public health outcomes.

In the case of SSB taxes, the tax needs to increase the price of the product to incentivize consumers to purchase less. After consuming fewer SSBs, consumers cannot substitute the calories elsewhere in their diet, and SSB drinkers must maintain the same level of caloric output with the decreased caloric consumption. Only then could these aggregate changes translate into improved health.

In 2017, Catalonia implemented a tiered excise tax on SSBs. The tax rate varies by sugar content, with drinks containing 5g or less sugar per 100mL carrying no tax, drinks with 5g to 8g of sugar per 100mL being charged 10 cents per liter, and drinks with more than 8g of sugar per 100mL having a 15 cents per liter tax.

The tax applies to nectars and some dairy beverages, though drinkable yogurts and fermented milk are excluded. The tax doesn’t apply to any solid products. The law also requires the tax to be passed on to the final consumer, increasing the likelihood that consumers experience a tax-induced price increase.

Several academic studies have examined the impact of the Catalonia SSB tax, with most of the focus being on the extent to which SSB consumption fell after the tax. Studies suggest that SSB purchases fell between 7.7 percent and 16.7 percent following the tax.

Few studies have explored the tax’s effect on the primary outcomes of obesity rates, body mass index (BMI), sugar intake, or diabetes rates. We present data compiled by Catalan and Spanish health organizations on these outcome measures.

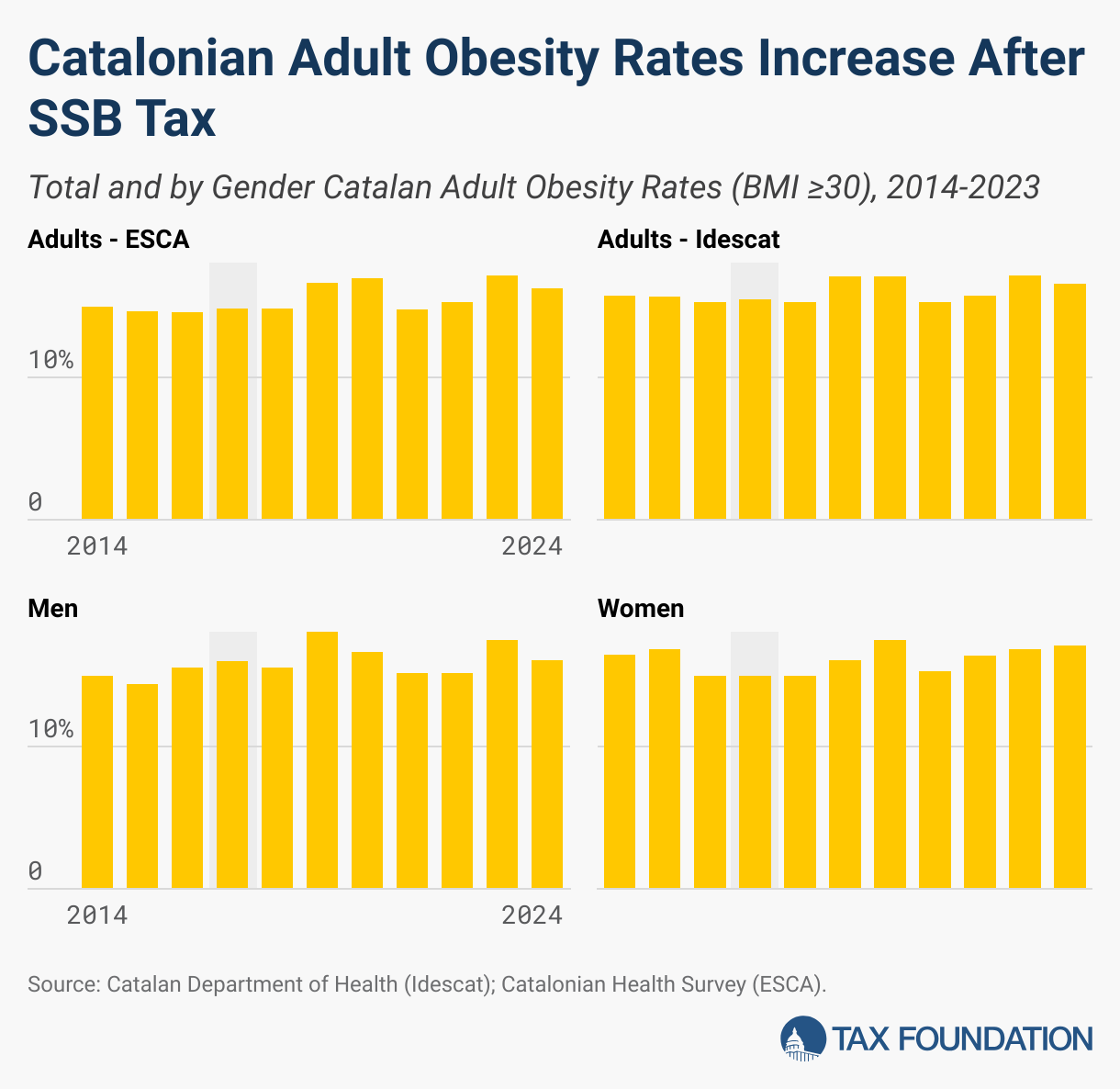

Following the SSB tax, Catalan adult obesity increased substantially from 2017 to 2023 according to data from the Catalan Health Survey (ESCA) and the Statistical Institute of Catalonia (Idescat). Adult obesity rates increased for both men and women.

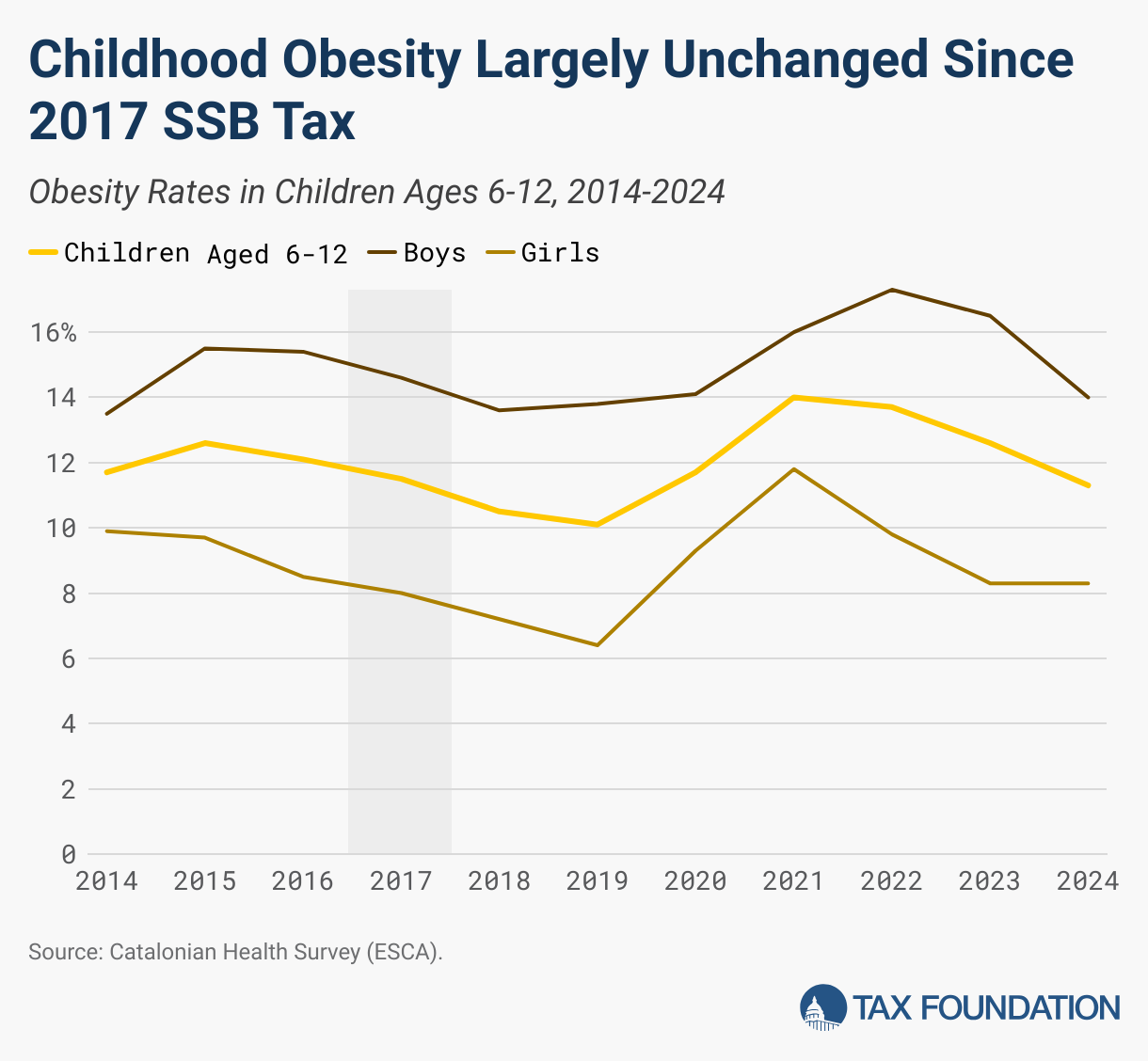

The ESCA also quantifies childhood obesity rates for children ages 6-12. Childhood obesity rates decreased slightly following the SSB tax in 2017. However, after 2019, childhood obesity rates rebounded to near or above their initial levels in 2017. This pattern occurred for both boys and girls.

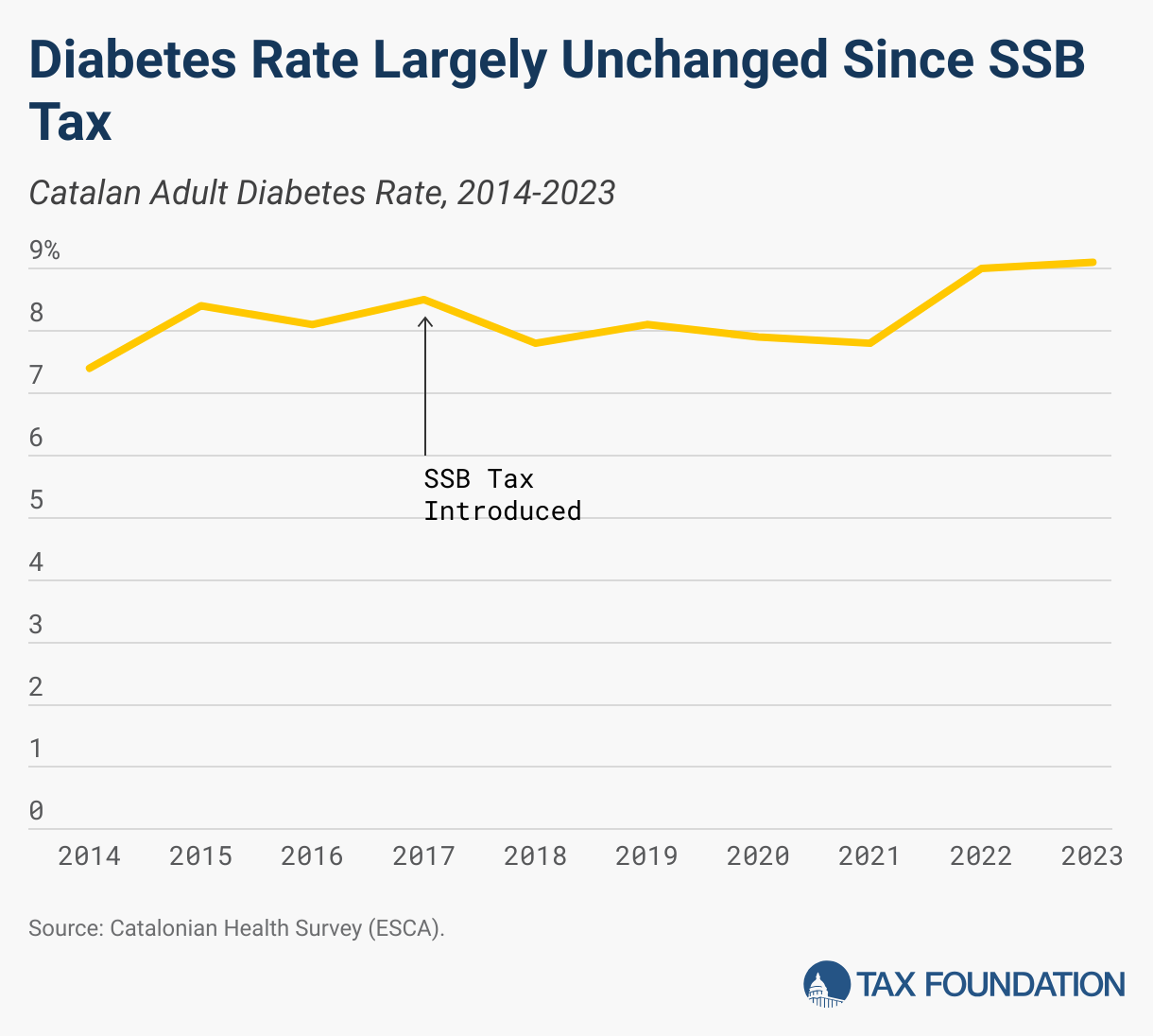

Next, we examine diabetes rates in Catalonia. In 2016, the diabetes rate was 8.1 percent, and by 2023, the diabetes rate was 9.1 percent, an increase of more than 12 percentage points. Similar to obesity rates, Catalan rates of diabetes have increased since the imposition of the SSB tax.

Significantly more Catalans report daily consumption of sugar-sweetened products left out of the SSB tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.. Among teens and young adults aged 15 to 69, rates of daily consumption of SSBs were nearly half that of daily consumption of similarly sugary but untaxed products like non-home-made pastries. Among children aged 3 to 14, rates of daily consumption of SSBs were less than half that of daily consumption of untaxed sugar-sweetened products.

Catalonia’s SSB tax doesn’t appear to have solved its problems with obesity or diabetes. An important question to consider is how Catalonia residents compare to those in other regions where no SSB tax was implemented. If the trend in all Spanish cities includes growing rates of obesity and diabetes, the results of Catalonia’s SSB tax might not look so underwhelming.

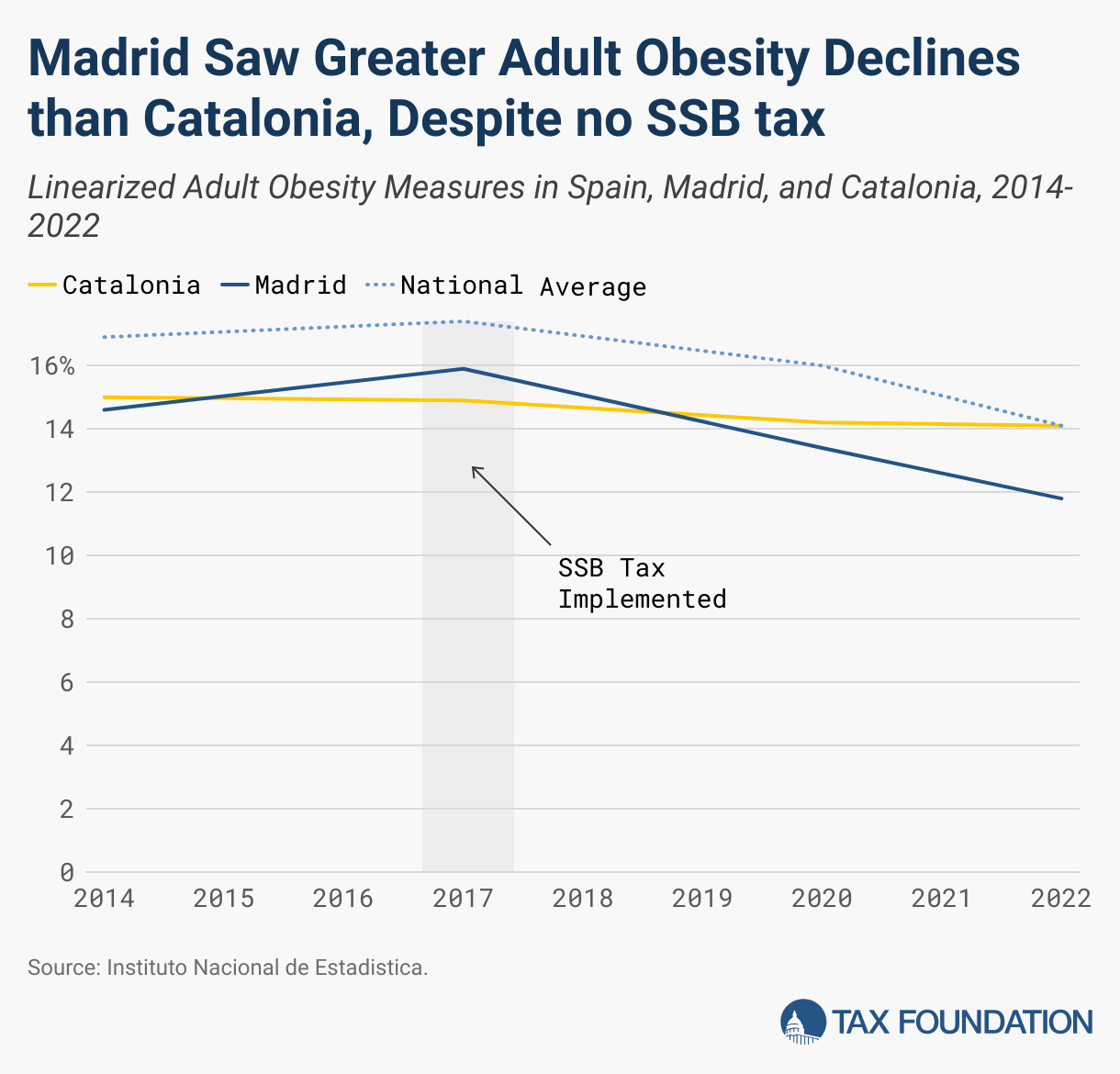

In 2017, the year the SSB tax was implemented, Catalan adults had an obesity rate of 14.9 percent, according to data from the Instituto Nacional de Estadistica. By 2022, these data suggest obesity had fallen slightly to 14.1 percent.

Adult obesity in Madrid, where there was no SSB tax, declined much more, from 15.9 to 11.8 percent. This mirrors the national Spanish average obesity rate, which declined from 17.4 to 14.1 percent over the same time period. According to these data, Catalonia lagged behind other regional and national obesity trends, despite the SSB tax.

The data show that the SSB tax hasn’t solved Catalonia’s problems with obesity or diabetes. Consumers drank fewer SSBs after the tax, but that hasn’t been sufficient to impact sugar consumption or any meaningful measures of public health.

As currently designed, Catalonia’s SSB tax has such a narrow base that consumers can substitute alternative sugary products to maintain their level of sugar consumption. If the external costs of obesity are largely driven by caloric, and specifically sugar, consumption, nutrient taxes on all foods and beverages, not just SSBs, are the best tax base and would grant the most neutral tax treatment. A low-rate, specific tax based on each product’s added grams of sugar or total kilocalories would have a far better chance at decreasing obesity and improving public health than narrowly targeted SSB taxes.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

Share this article

")

{kind=link}