AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Related Coverage

Transcript

Marathon Petroleum Corporation (MPC) Q1 2026 Earnings Call Transcript

May 5, 2026

Breaking News

Marathon Petroleum Releases Q1 2026 Financial Results

May 5, 2026

Stock $252.54 (+2.6%)

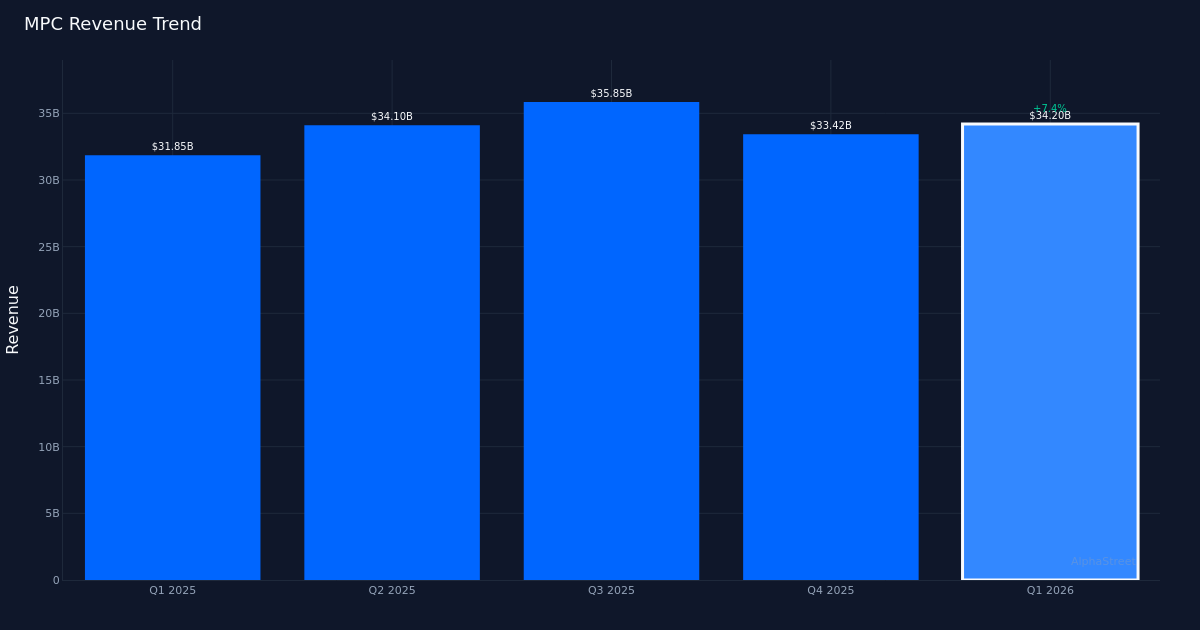

Strong Beat. Marathon Petroleum Corporation (NYSE: MPC) delivered Q1 2026 adjusted earnings of $1.65 per share, crushing the $0.75 consensus estimate by 120.0%. The refining and marketing giant generated $34.20B in revenue for the quarter, up 8.5% from the $31.52B recorded in Q1 2025, demonstrating both earnings power and top-line momentum. Adjusted net income reached $487.0M as the company capitalized on favorable refining conditions during the period.

Operational Execution. The quality of this beat appears driven by genuine operational performance rather than financial engineering. With revenue climbing alongside earnings, Marathon is extracting value from both volume and margin expansion in its refining operations. The company’s crude oil capacity utilization stood at 89.0% for the quarter, reflecting healthy demand for refined products and disciplined asset management.

Market Response. Shares rose 2.6% to $252.54 following the results, though the modest gain suggests investors may have anticipated strength or are looking ahead to potential margin compression concerns. The stock’s reaction indicates some caution despite the dramatic earnings surprise, possibly reflecting broader macro headwinds facing the refining sector or questions about sustainability of current crack spreads. Nevertheless, the upward movement confirms that the market views this quarter’s performance positively, even if not transformationally so.

Analyst Positioning. Wall Street maintains a constructive stance on Marathon Petroleum, with consensus showing 12 buy ratings and 10 hold ratings, while notably zero analysts recommend selling the stock. This positioning suggests the investment community sees Marathon as either fairly valued or modestly undervalued at current levels, with the buy-rated analysts likely betting on continued refining margin strength and the company’s capital return program. The absence of sell ratings is particularly noteworthy in a cyclical industry prone to volatility.

What to Watch: Marathon’s ability to sustain utilization rates near 89.0% while maintaining margin discipline will determine whether this quarter represents peak earnings or the beginning of an extended upcycle. Investors should monitor crack spread trends and management’s capital allocation priorities as the company navigates a potentially volatile refining environment in the quarters ahead.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}