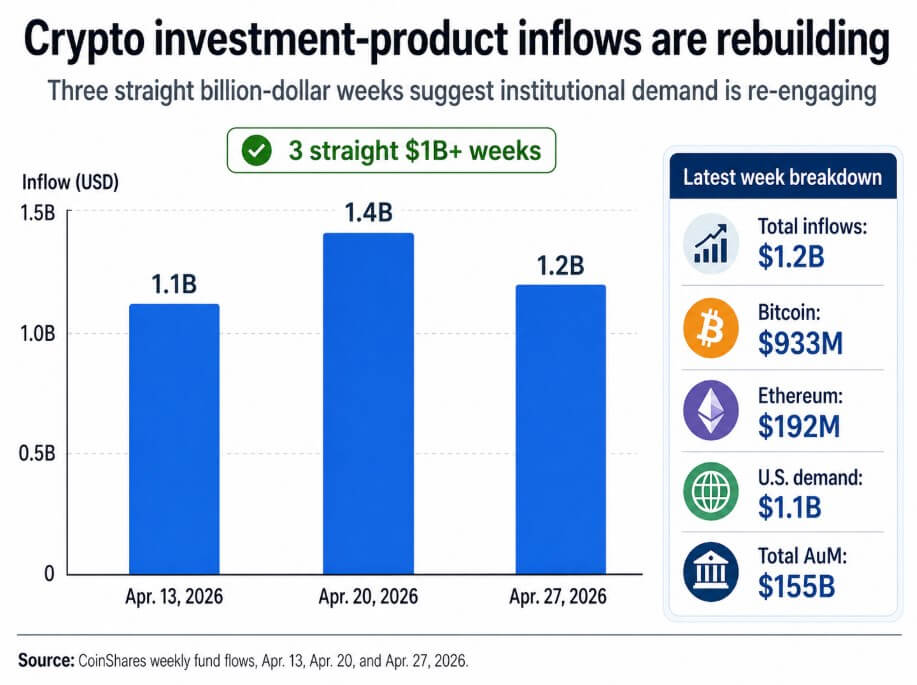

Crypto investment products recorded $1.2 billion in inflows last week, capping three straight weeks above $1 billion and a fourth consecutive positive week overall.

According to CoinShares data, Bitcoin pulled $933 million of that total, Ethereum added $192 million, and the US accounted for $1.1 billion of regional demand. Total assets under management climbed to $155 billion, the highest reading since Feb. 1, though still below the October 2025 peak of $263 billion.

CoinShares attributed the three-week streak to improving institutional demand while flagging the Apr. 28-29 FOMC decision as a source of marginal caution.

The demand stack

The inflow data converges with signals from several other channels simultaneously, which is what distinguishes it from a single-report anomaly.

On regulated derivatives, CME reported that its average daily volume of crypto rose from 191,000 to 310,000 contracts year over year in the first quarter, with average daily open interest reaching 313,900 contracts, up 25% from the first quarter of 2025.

Open interest at that level means capital is staying in the marketplace, pointing to a longer-horizon positioning posture.

The CoinShares report noted that blockchain equity ETFs have taken in $617 million over the past three weeks, reinforcing the view that institutions are buying infrastructure exposure alongside direct coin positions.

Corporate treasury accumulation has continued on its own track. Strategy’s Apr. 27 SEC filing shows another 3,273 BTC purchased during Apr. 20-26, bringing its total to 818,334 BTC at an aggregate cost of $61.8 billion, according to Bitcoin Treasuries.

Hong Kong-listed Bitfire is targeting over 10,000 BTC for a regulated “Alpha BTC” strategy within a year, while Avenir held $908 million of BlackRock’s IBIT at the end of 2025.

The geographic spread, comprising US corporate treasuries, regulated Asian asset management, and global investment products all moving in the same direction, gives the demand recovery a structural quality that a single weekly inflow report could not establish on its own.

DefiLlama puts the total stablecoin market cap at roughly $320.7 billion, up 1.73% over 30 days, meaning the on-ramp infrastructure for deploying capital into Bitcoin is expanding.

Beyond demand

Market structure adds a layer that prevents demand recovery from being read as settled.

Glassnode’s Apr. 22 report placed Bitcoin back above the True Market Mean at $78,100, with the short-term holder cost basis at $80,100 now serving as the immediate resistance ceiling.

ETF flows had turned modestly positive again, and spot demand showed early signs of recovery. Glassnode also reported that short-term holders realized profit had spiked to $4.4 million per hour, nearly three times the $1.5 million threshold that marked prior local tops this year.

At that rate, recent buyers are locking in gains at a pace the market has historically struggled to absorb without a pause or pullback.

Glassnode’s spot breakdown noted that Binance’s cumulative volume delta (CVD) drove much of the recent buying, while Coinbase activity stayed comparatively muted.

Coinbase is the primary venue for US institutional spot activity, and a recovery driven more by offshore retail and mid-tier funds leaves the bid less anchored than the headline inflow figures imply.

Farside Investors’ daily US ETF data makes the same point from a different angle. Spot Bitcoin ETFs posted positive flows for nine trading sessions, surpassing $2 billion, before turning negative on Apr. 27.

Three weeks of billion-dollar inflow readings and a single-day reversal can both be true at once, and together they describe a demand recovery that is directionally real but still fragile enough to break on a macro catalyst.

Improving signalsFragility signalsETF flows turned modestly positive again$80.1K remains immediate resistanceSpot demand showed early recoveryRealized profit rose to $4.4M/hourBitcoin reclaimed $78.1K True Market MeanCoinbase activity remained mutedThree straight $1B+ weekly product inflow weeksProfit-taking risk rises as buyers move into gain

The Apr. 28-29 FOMC meeting is now the first hard test to see if the institutional bid that has been built over four weeks can hold its ground.

CoinShares explicitly tied current investor caution to that decision window, and the market structure data from Glassnode explains that Bitcoin is pressing into the $80,100 zone, where over 54% of recent buyers would be sitting on profit, historically the zone where distribution selling has exhausted bear market rallies.

A Fed outcome that leaves financial conditions roughly unchanged removes the largest near-term macro headwind.

A hawkish surprise, or language that tightens the rate-cut timeline further, hands sellers exactly the external trigger they need to act on those elevated profit readings.

The two paths forward

The bull case rests on the Fed passing without adding fresh macro stress, weekly product inflows holding near or above $1 billion, US ETF demand re-accelerating past the Apr. 27 wobble, and Coinbase spot activity closing the gap with offshore venues.

The demand recovery becomes self-reinforcing, and Bitcoin clearing $80,100 with consistent spot absorption behind it would shift the market structure from “rally on trial” to a confirmed demand regime, pulling in the next layer of institutional allocators who have been waiting for the price structure to confirm the flow data.

In that scenario, the October 2025 AUM peak of $263 billion becomes the relevant reference point, and the three-week inflow streak gets read as the early phase of a durable re-engagement.

The bear case turns on the same variables running in reverse. If the Fed re-tightens financial conditions at the margin, the weekly flow streak breaks, and Glassnode’s realized profit warning starts to dominate price action, the recent move resolves as another distribution rally, particularly if ETF demand fades and price cannot hold above the reclaimed mean.

Glassnode’s own record shows that prior rallies this year have struggled at exactly that point, and with liquidity conditions still thin, a breakdown at $78,100 could accelerate faster than inflow data would predict.

Total AUM at $155 billion is 41% below the October peak, meaning far more unwound institutional exposure above current levels.

ScenarioTriggerWhat confirms itWhat breaks itWhy it mattersBull caseThe Fed passes without adding fresh macro stressWeekly digital-asset investment-product inflows stay near or above $1B; U.S. spot Bitcoin ETF demand re-accelerates after the Apr. 27 wobble; Coinbase spot activity closes the gap with offshore venues; Bitcoin clears $80,100 with sustained spot absorptionHawkish Fed language, fading ETF flows, renewed offshore-only buying, or failure to break $80,100Confirms the recent inflow streak as the start of a more durable institutional re-engagement and opens the way for Bitcoin to challenge higher reference levels, including the $263B October 2025 AuM peakBase caseThe Fed is broadly neutral and does not materially change financial conditionsWeekly flows remain positive but below the recent $1B+ pace; ETF flows stay mixed; Bitcoin holds above $78,100 but struggles to decisively clear $80,100A sharp deterioration in ETF demand, rising profit-taking, or a breakdown below $78,100Suggests institutions are re-engaging, but not yet with enough conviction to shift the market into a fully confirmed demand regimeBear caseThe Fed tightens conditions at the margin or signals a less supportive rate pathWeekly flow streak breaks; ETF demand fades; Glassnode’s realized-profit warning starts to dominate price action; Bitcoin fails at $80,100 and loses $78,100A dovish or benign Fed outcome, resumed $1B+ weekly inflows, stronger Coinbase participation, and a reclaim of $80,100Recasts the recent move as another distribution rally rather than a durable recovery, with thin liquidity making downside sharper than inflow data alone would suggest

CoinShares’ three straight billion-dollar weeks, CME’s higher open interest, Strategy’s continued accumulation, and a deeper base of stablecoin liquidity all point to capital returning to Bitcoin with greater conviction.

The recovery runs across enough channels simultaneously to rule out a single-venue anomaly, and the Fed now decides if the market can keep this movement.

-1024x683.jpg "Florida Roads Become a Battleground for Illegal Immigration")

{kind=link}