While the European Commission focuses on improving value-added taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. (VAT) compliance by improving taxpayer compliance and reducing tax fraud, policy is a major contributor to VAT revenue losses. The VAT actionable policy gap—the additional VAT revenue that could realistically be collected by eliminating reduced rates and certain exemptions—amounted to €773.5 billion in 2024, six times the compliance gap.

VAT Is the Leading Driver of Revenue

Addressing the VAT actionable policy gap is important given the substantial revenue VAT generates across the EU. On average, in 2024, EU countries raised 20.7 percent of their total tax revenue from the VAT. In Estonia and Latvia, more than 27.3 percent of tax revenue comes from the VAT, compared to 15.4 percent in Italy and 14.5 percent in Belgium. Member States’ VAT revenue is also the base for one of the EU’s “own resources,” representing roughly 9.5 percent of the EU’s revenue in 2024.

VAT Actionable Policy Gap

The VAT policy gap is made up of two components: the rate gap and the exemption gap. The former represents lost VAT revenue due to reduced VAT rates, while the latter represents lost VAT revenue due to certain goods and services being exempt from the VAT. Policymakers often justify exemptions and reduced rates with arguments that they promote the consumption of certain goods and services to address equity, environmental, and other policy goals. But exemptions and reduced rates are bad policy because they distort consumption patterns, inefficiently deliver fiscal benefits, add complexity for businesses, and reduce revenue, forcing governments to rely on less economically efficient revenue sources.

However, there are some services—namely, imputed rents, the provision of publicly provided goods, and financial services—that are VAT-exempt because it would be difficult to levy VAT on them. Subtracting the amount of lost VAT revenue caused by these services from the general policy gap leaves us with the actionable policy gap (i.e., the actionable exemption gap plus the rate gap), which is the amount of additional VAT revenue lawmakers could realistically raise by eliminating reduced rates and certain exemptions.

In 2024, the average actionable policy gap for the EU was 27.1 percent of potential revenue—of which 12 percentage points were due to reduced rates (rate gap) and 15 percentage points due to the actionable portion of the exemption gap.

The VAT Rate Gap

The rate gap is smaller in countries that rely less on reduced rates, such as Denmark, Estonia, Latvia, Bulgaria, and Lithuania. However, the rate gaps in Poland, Greece, Ireland, Austria, Italy, and Spain show significant forgone revenue because of reduced rates.

On average at the EU level, of the 12‑percentage‑point rate gap, 4.7 points were attributable to reduced rates on food and agricultural products, 2.4 points to reduced rates in the hospitality sector, 1 point to reduced rates in transportation, 0.8 points to utilities, and 0.6 points to pharmaceutical products. However, significant differences emerge, as Member States tend to prioritize and apply reduced rates to different goods and services.

In 2023, Poland and Malta recorded the highest food rate gaps at 10.3 and 7.7 percentage points, respectively. In the hospitality sector, Portugal, Cyprus, Spain, Austria, Greece, and Croatia each had rate gaps exceeding 4 percent.

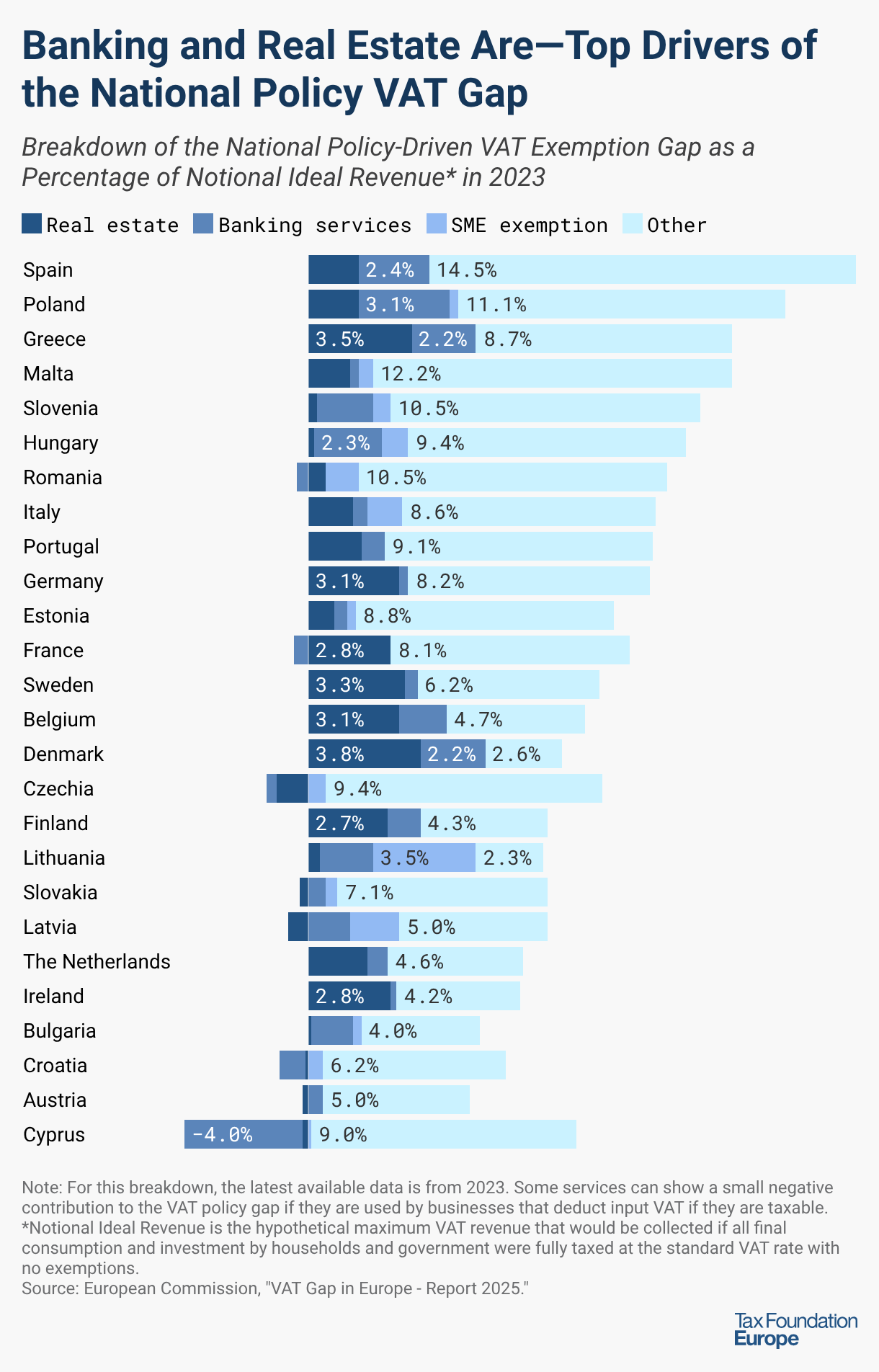

The Actionable Exemption Gap

The VAT exemption gap can be divided into the national policy-driven VAT exemption gap and the EU policy-mandated VAT exemption gap, which is required by the VAT directive. In 2024, the highest EU policy-mandated exemption gaps were observed in Portugal (5.6 percent) and Belgium (5 percent), while the smallest gaps were observed in Bulgaria (1.2 percent), Estonia (1.6 percent), and Croatia (1.8 percent). Member States showed similar EU‑mandated VAT exemption gaps, with economic factors explaining most of the variation. These gaps were primarily driven by the exemptions applied to private health insurance (1.3 percent), private education (1 percent), and insurance-related activities (1.1 percent).

In 2024, the highest national policy-driven exemption gaps were observed in Spain (18.6 percent), Estonia (17.9 percent), and Poland (16.1 percent). The national policy-driven exemption gap was smaller in Bulgaria (4.9 percent), Cyprus (4.9 percent), Austria (5 percent), and Croatia (5.9 percent).

The sectors contributing to the national policy exemption gap varied substantially across Member States, yet many could not be identified because of limited detail. Using the latest data available (2023), on average across the EU, 0.6 percentage points of the national policy-driven exemption gap were due to real‑estate exemptions, 1.7 points to exemptions in the banking sector, and 0.7 points to exemptions for small businesses. However, substantial differences among Member States exist. Nevertheless, the real estate sector, the banking sector, and the broader financial and insurance services sector are subject to different forms of taxation across EU Member States, beyond the VAT framework. For example, in France, the insurance premium tax applicable to motor third-party liability insurance reaches up to 33 percent.

Closing the VAT Actionable Policy Gap: Unlocking Major Revenue Gains and Improving Tax Policy

Overall, in 2024, the highest actionable policy gaps were observed in Spain (37.6 percent), Greece (36.3 percent), Ireland (34.7 percent), Poland (33.7 percent), Italy (32 percent), Portugal (29.8 percent), Slovenia (27.9 percent), Belgium (27.6 percent), and France (27.1 percent). Spain’s actionable policy gap was due in part to the application of different indirect taxes in the Canary Islands, Ceuta, and Melilla. The actionable policy gap was smaller in Bulgaria (10.2 percent), Denmark (11.4 percent), Latvia (14.8 percent), and Lithuania (15.5 percent).

European countries could increase their tax revenue by broadening the VAT base through the elimination of exemptions and reduced rates. This would allow policymakers to either increase VAT revenues or reduce the top statutory VAT rate.

Increase VAT Revenues

Closing the VAT actionable policy gap would increase EU countries’ VAT revenues by more than one third (37 percent). VAT revenues will see the biggest increase in Spain (60 percent), Greece (57 percent), Ireland (53 percent), Poland (51 percent), Italy (47 percent), Portugal (42 percent), Slovenia (39 percent), Belgium (38 percent), and France (37 percent). Bulgaria (11 percent), Denmark (13 percent), Latvia (17 percent), and Lithuania (18 percent) will benefit the least from broadening the VAT tax base, as their revenues would increase by less than 20 percent.

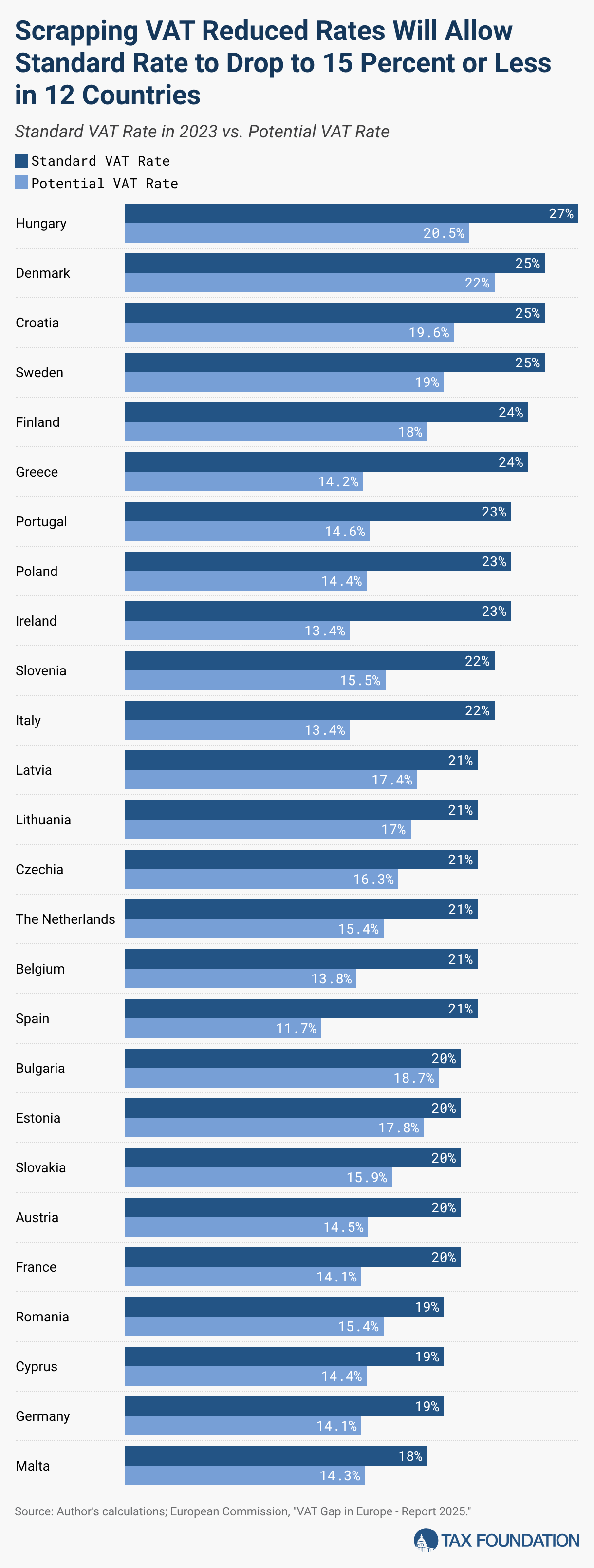

Reduce the General VAT Rate

By eliminating actionable exemptions and reducing rates across the EU, the standard VAT rate would drop on average by 5.7 percentage points to 15.4 percent.

On one hand, Greece, Ireland, Spain, Italy, Poland, and Portugal would reduce their standard rate by more than 8 percentage points. On the other hand, Malta, Latvia, Romania, Denmark, Estonia, and Bulgaria would reduce their standard VAT rate by less than 4 percentage points.

The benefits of implementing a single VAT tax rate are twofold: the reduction of compliance costs by simplifying the tax return process for businesses and a more neutral tax code for consumption decisions.

The main political justification for reduced VAT rates and VAT-exempted goods/services is to promote equity because lower-income households tend to spend a larger share of income on food and public transport. Some policymakers also want to encourage the consumption of “merit goods” (e.g., books), promote local services (e.g., tourism), and correct externalities (e.g., clean power). However, the positive externalities of these goods and services are likely not proportional to their value-added. There are also more targeted policies to correct environmental externalities, such as carbon pricing.

However, in absolute terms, higher-income households tend to benefit more than lower-income households from VAT reduced rates because they tend to consume more (and more expensive) goods at those reduced rates. Evidence shows that reduced VAT rates and VAT exemptions are not necessarily effective in achieving redistributive policy goals and can even be regressive in some instances. A recent European Commission study finds that reduced rates have an overall regressive effect in nine countries—Belgium, Bulgaria, Cyprus, Estonia, Finland, Greece, the Netherlands, Poland, and Slovenia—and a negligible effect in five Member States: France, Ireland, Latvia, Lithuania, and Slovakia. Moreover, in Bulgaria, Cyprus, Estonia, Finland, Greece, the Netherlands, and Poland, the goods subject to reduced rates are not those most likely to be consumed by lower‑income households. Instead of reduced rates, governments can implement compensation measures for poorer households, such as targeted tax credits or direct transfers to low-income earners.

Abolishing Distortive Taxes Like DSTs

VAT has been changing in recent years to account for the digitalization of the economy. The reforms require non-EU businesses to register and remit VAT in the Member State of the consumer, effectively taxing digital services at the point of consumption. The EU VAT revenues collected from these measures increased tenfold, from €3 billion in 2015, €4.5 billion in 2018, and €20 billion in 2022, to more than €33 billion in 2024.

Expanding VAT to include digital services would allow Member States to eliminate their digital services taxes (DSTs). Abolishing DSTs would also eliminate the distortions that taxes on gross revenues create.

Positively Impact the EU’s Own Resources

In addition to being an important source of revenue for EU countries, VAT revenue is also one of the EU’s own resources. However, the share of VAT-based resources accounted for only 9.5 percent of the EU’s total revenue in 2024, down from 60 percent in 1988. This decline is due to own resources policy reforms that reduced both the VAT base and the VAT rate. Since the VAT revenue collected by each Member State determines the VAT base for own resources, closing the VAT actionable policy gap, and especially the actionable exemption gap, would not only positively impact EU countries’ VAT revenues but could also contribute to the EU’s sources of revenue. Closing the VAT system’s gaps would reinforce VAT as an important and stable revenue source for the EU budget.

In fact, EU countries could raise up to €773 billion simply by closing the VAT actionable policy gap, an amount equal to four times the EU’s 2026 budget.

If the EU truly intends to reform its financing system, the simplest path is to reform the VAT.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

Share this article

?")

-1024x683.jpg "Florida Roads Become a Battleground for Illegal Immigration")

")

{kind=link}