Published on April 14th, 2026 by Bob Ciura

The S&P 500 Index is the world’s best-known and most widely recognized stock market index.

The index includes 500 companies and covers approximately 80% of available market capitalization.

As global industry leaders, the companies that comprise the S&P 500 widely enjoy durable competitive advantages, including wide economic moats.

In turn, their strength and stability allows many of the S&P 500 companies to raise their dividends each year.

With this in mind, we created a list of stocks that have increased their dividends for over 10 consecutive years. We collectively refer to these dividend growth stocks as blue chips.

You can download your free copy of the blue chip stocks list by clicking below:

There are currently more than 500 securities in our blue chip stocks list.

Keep reading to see our list of the 10 best S&P 500 stocks for expected total returns over the next five years.

Table of Contents

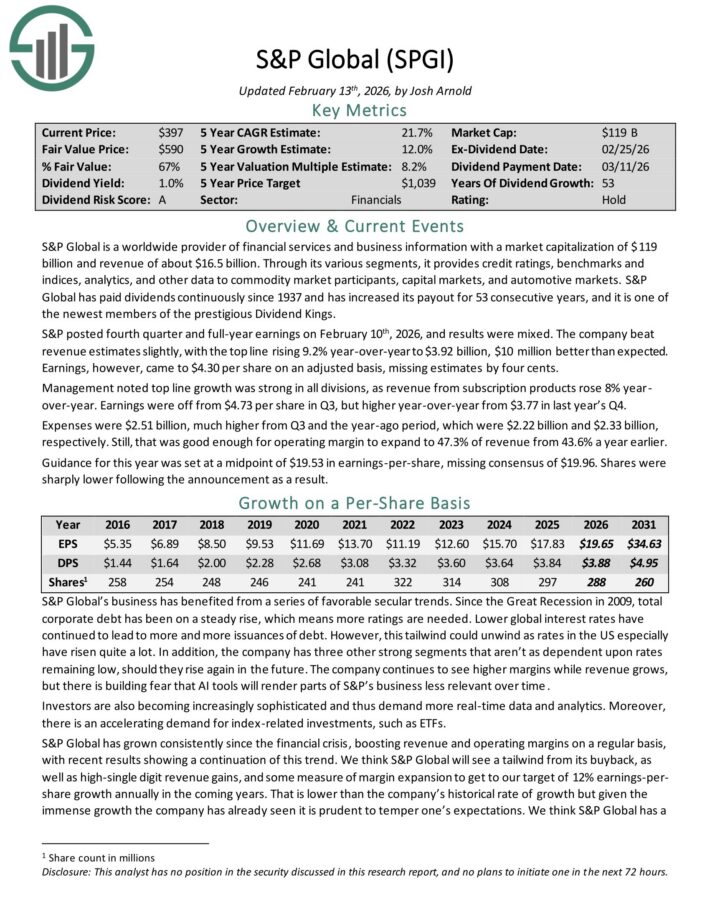

Best S&P 500 Stock #10: S&P Global (SPGI)

Expected Annual Returns: 19.9%

S&P Global is a worldwide provider of financial services and business information with revenue of over $15 billion.

Through its various segments, it provides credit ratings, benchmarks and indices, analytics, and other data to commodity market participants, capital markets, and automotive markets.

S&P Global has paid dividends continuously since 1937 and has increased its payout for 52 consecutive years, and it is one of the newest members of the prestigious Dividend Kings.

S&P posted fourth quarter and full-year earnings on February 10th, 2026, and results were mixed. The company beat revenue estimates slightly, with the top line rising 9.2% year-over-year to $3.92 billion, $10 million better than expected.

Earnings, however, came to $4.30 per share on an adjusted basis, missing estimates by four cents. Management noted top line growth was strong in all divisions, as revenue from subscription products rose 8% year-over-year. Earnings were off from $4.73 per share in Q3, but higher year-over-year from $3.77 in last year’s Q4.

Expenses were $2.51 billion, much higher from Q3 and the year-ago period, which were $2.22 billion and $2.33 billion, respectively. Still, that was good enough for operating margin to expand to 47.3% of revenue from 43.6% a year earlier.

Click here to download our most recent Sure Analysis report on SPGI (preview of page 1 of 3 shown below):

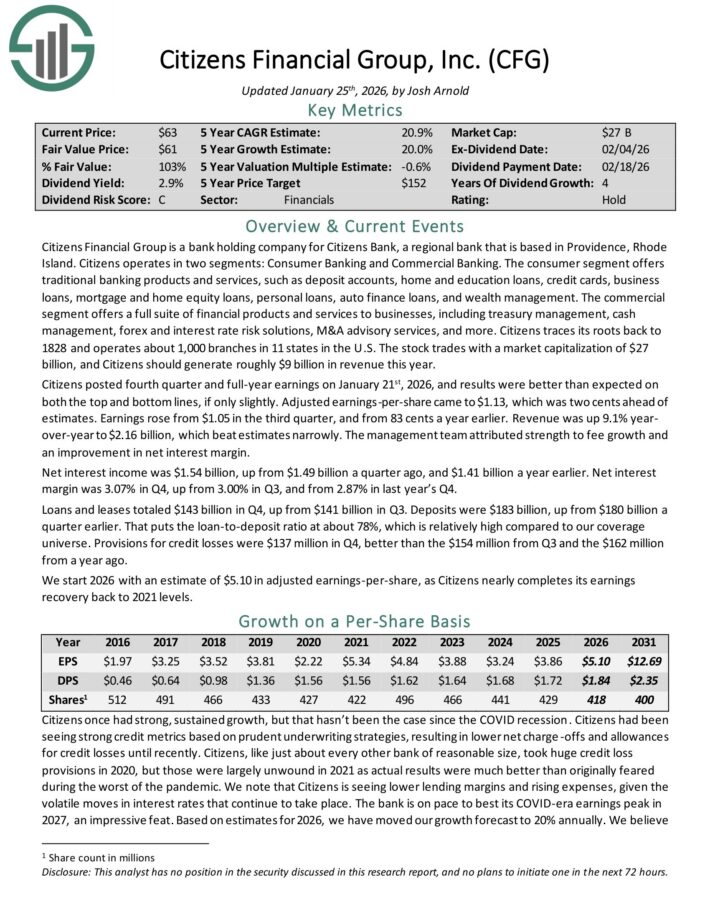

Best S&P 500 Stock #9: Citizens Financial (CFG)

Expected Annual Returns: 20.2%

Citizens Financial Group is a bank holding company for Citizens Bank, a regional bank that is based in Providence, Rhode Island.

Citizens operates in two segments: Consumer Banking and Commercial Banking. The consumer segment offers traditional banking products and services.

The commercial segment offers a full suite of financial products and services to businesses, including treasury management, cash management, forex and interest rate risk solutions, M&A advisory services, and more.

Citizens traces its roots back to 1828 and operates about 1,000 branches in 11 states in the U.S. Citizens should generate roughly $9 billion in revenue this year.

Citizens posted fourth quarter and full-year earnings on January 21st, 2026, and results were better than expected on both the top and bottom lines, if only slightly.

Adjusted earnings-per-share came to $1.13, which was two cents ahead of estimates. Earnings rose from $1.05 in the third quarter, and from 83 cents a year earlier.

Revenue was up 9.1% year-over-year to $2.16 billion, which beat estimates narrowly. Net interest income was $1.54 billion, up from $1.49 billion a quarter ago, and $1.41 billion a year earlier.

We start 2026 with an estimate of $5.10 in adjusted earnings-per-share.

Click here to download our most recent Sure Analysis report on CFG (preview of page 1 of 3 shown below):

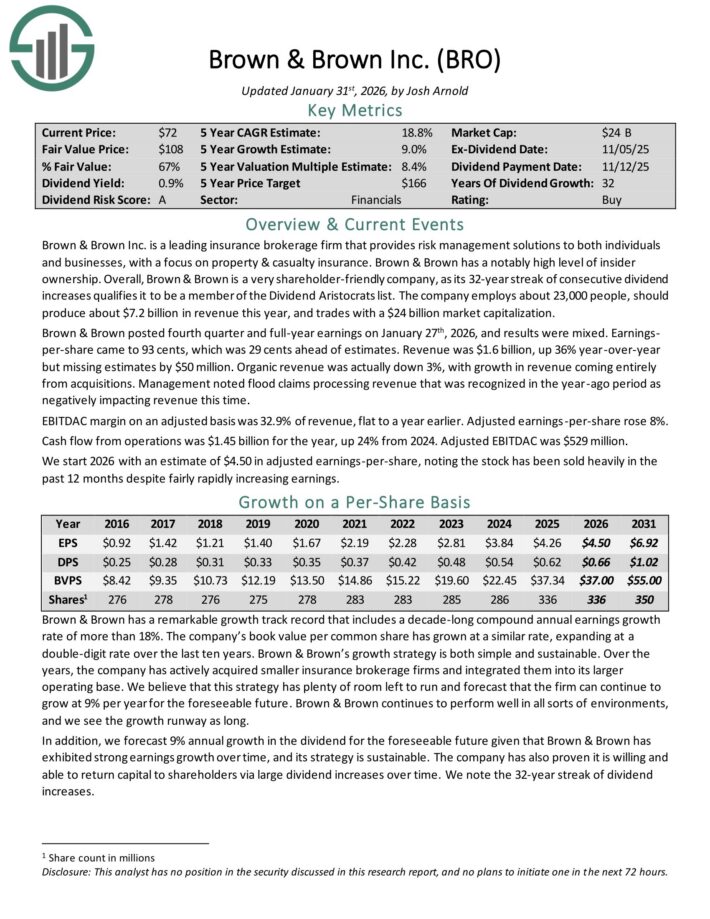

Best S&P 500 Stock #8: Brown & Brown, Inc. (BRO)

Expected Annual Returns: 20.4%

Brown & Brown Inc. is a leading insurance brokerage firm that provides risk management solutions to both individuals and businesses, with a focus on property & casualty insurance.

Brown & Brown posted fourth quarter and full-year earnings on January 27th, 2026, and results were mixed. Earnings-per-share came to 93 cents, which was 29 cents ahead of estimates.

Revenue was $1.6 billion, up 36% year-over-year but missing estimates by $50 million. Organic revenue was actually down 3%, with growth in revenue coming entirely from acquisitions.

Management noted flood claims processing revenue that was recognized in the year-ago period as negatively impacting revenue this time.

EBITDAC margin on an adjusted basis was 32.9% of revenue, flat to a year earlier. Adjusted earnings-per-share rose 8%.

Cash flow from operations was $1.45 billion for the year, up 24% from 2024. Adjusted EBITDAC was $529 million.

Click here to download our most recent Sure Analysis report on BRO (preview of page 1 of 3 shown below):

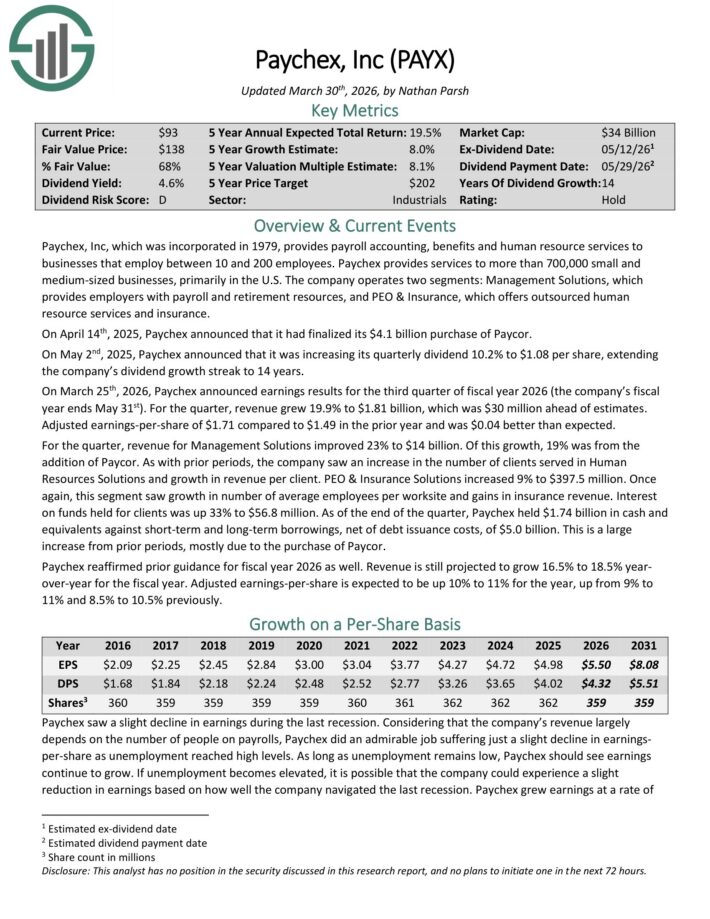

Best S&P 500 Stock #7: Paychex, Inc. (PAYX)

Expected Annual Returns: 20.6%

Paychex provides payroll accounting, benefits and human resource services to businesses that employ between 10 and 200 employees.

It provides services to more than 700,000 small and medium-sized businesses, primarily in the U.S.

The company operates two segments: Management Solutions, which provides employers with payroll and retirement resources, and PEO & Insurance, which offers outsourced human resource services and insurance.

Paychex has increased its dividend for 14 consecutive years.

On March 25th, 2026, Paychex announced earnings results for the third quarter of fiscal year 2026. For the quarter, revenue grew 19.9% to $1.81 billion, which was $30 million ahead of estimates.

Adjusted earnings-per-share of $1.71 compared to $1.49 in the prior year and was $0.04 better than expected.

For the quarter, revenue for Management Solutions improved 23% to $14 billion. Of this growth, 19% was from the addition of Paycor.

The company saw an increase in the number of clients served in Human Resources Solutions and growth in revenue per client.

PEO & Insurance Solutions increased 9% to $397.5 million. This segment saw growth in number of average employees per worksite and gains in insurance revenue. Interest on funds held for clients was up 33% to $56.8 million.

Paychex reaffirmed prior guidance for fiscal year 2026. Revenue is still projected to grow 16.5% to 18.5% year-over-year for the fiscal year. Adjusted earnings-per-share is expected to be up 10% to 11% for the year.

Click here to download our most recent Sure Analysis report on PAYX (preview of page 1 of 3 shown below):

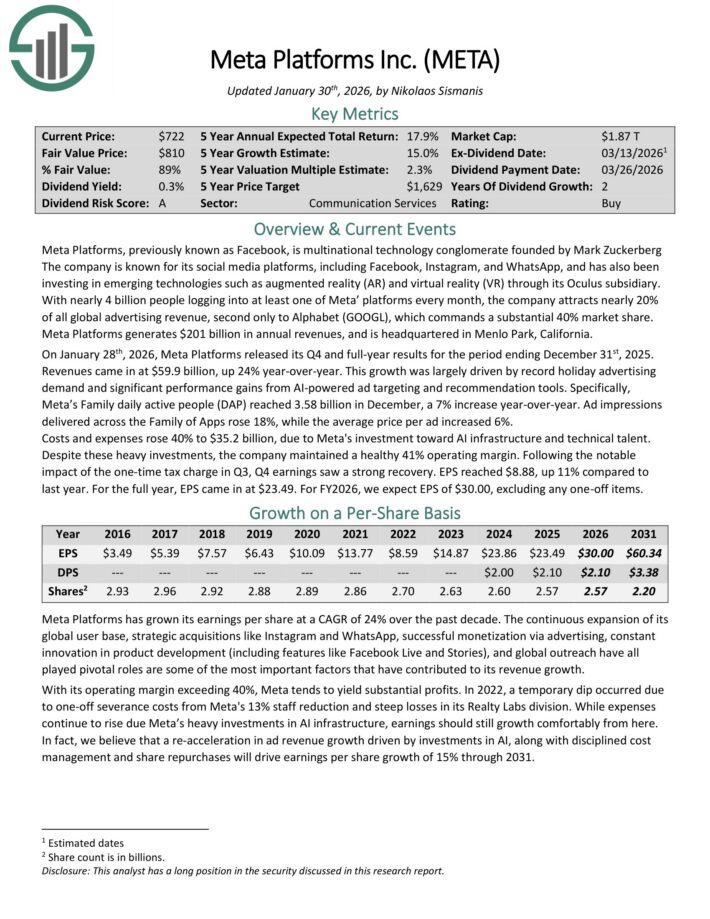

Best S&P 500 Stock #6: Meta Platforms (META)

Expected Annual Returns: 20.8%

Meta Platforms is a technology conglomerate known for its social media platforms, including Facebook, Instagram, and WhatsApp.

It has also been investing in emerging technologies such as augmented reality (AR) and virtual reality (VR) through its Oculus subsidiary.

With nearly 4 billion people logging into at least one of Meta’ platforms every month, the company attracts nearly 20% of all global advertising revenue, second only to Alphabet (GOOGL), which commands a substantial 40% market share.

Meta Platforms generates $201 billion in annual revenue, and is headquartered in Menlo Park, California.

On January 28th, 2026, Meta Platforms released its Q4 and full-year results for the period ending December 31st, 2025.

Revenue came in at $59.9 billion, up 24% year-over-year. This growth was largely driven by record holiday advertising demand and significant performance gains from AI-powered ad targeting and recommendation tools.

Specifically, Meta’s Family daily active people (DAP) reached 3.58 billion in December, a 7% increase year-over-year. Ad impressions delivered across the Family of Apps rose 18%, while the average price per ad increased 6%.

Despite these heavy investments, the company maintained a healthy 41% operating margin. EPS reached $8.88, up 11% compared to last year. For the full year, EPS came in at $23.49.

For FY2026, we expect EPS of $30.00, excluding any one-off items.

Click here to download our most recent Sure Analysis report on Meta (preview of page 1 of 3 shown below):

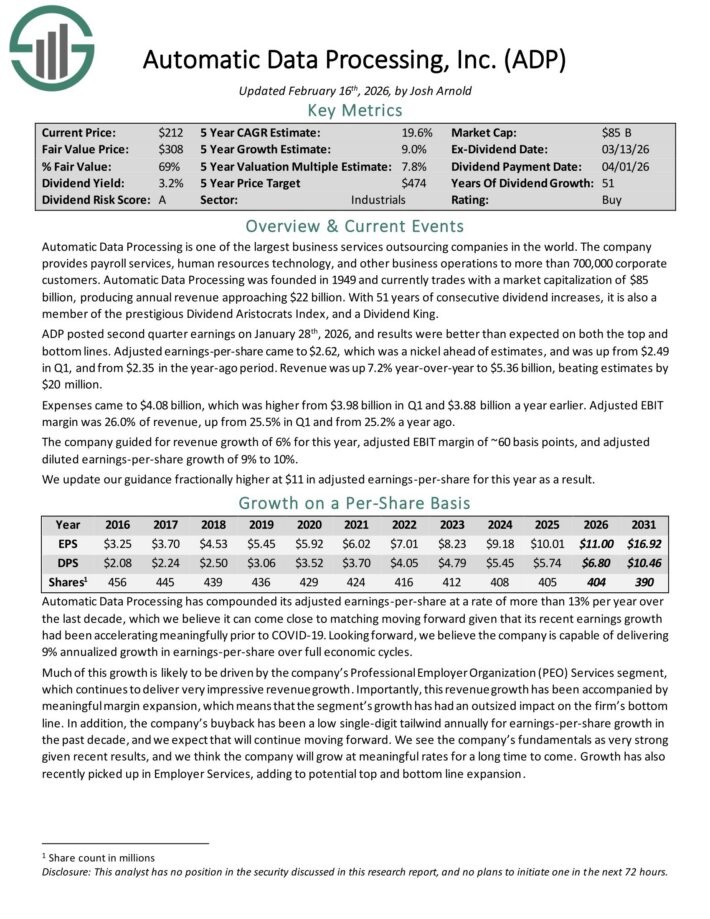

Best S&P 500 Stock #5: Automatic Data Processing (ADP)

Expected Annual Returns: 21.5%

Automatic Data Processing is one of the largest business services outsourcing companies in the world.

The company provides payroll services, human resources technology, and other business operations to more than 700,000 corporate customers.

ADP posted second quarter earnings on January 28th, 2026, and results were better than expected on both the top and bottom lines.

Adjusted earnings-per-share came to $2.62, which was a nickel ahead of estimates, and was up from $2.49 in Q1, and from $2.35 in the year-ago period. Revenue was up 7.2% year-over-year to $5.36 billion, beating estimates by $20 million.

Expenses came to $4.08 billion, which was higher from $3.98 billion in Q1 and $3.88 billion a year earlier. Adjusted EBIT margin was 26.0% of revenue, up from 25.5% in Q1 and from 25.2% a year ago.

For 2026, the company guided for revenue growth of 6% for this year, adjusted EBIT margin of ~60 basis points, and adjusted diluted earnings-per-share growth of 9% to 10%.

ADP has increased its dividend for over 50 consecutive years, qualifying it as a Dividend King.

Click here to download our most recent Sure Analysis report on ADP (preview of page 1 of 3 shown below):

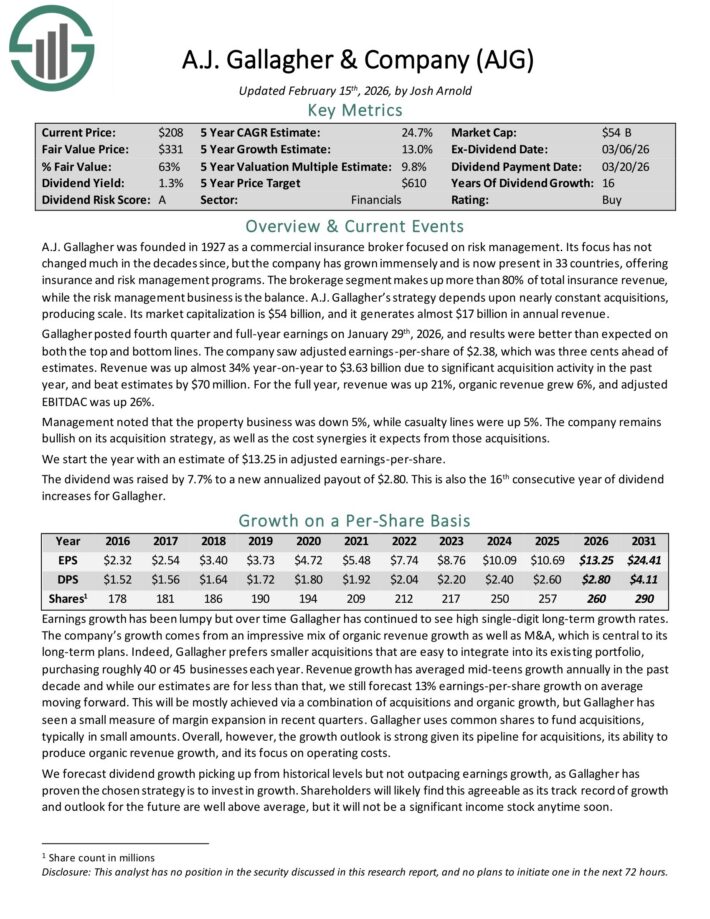

Best S&P 500 Stock #4: Arthur J. Gallagher & Co. (AJG)

Expected Annual Returns: 23.0%

A.J. Gallagher was founded in 1927 as a commercial insurance broker focused on risk management. It offers insurance and risk management programs.

The brokerage segment makes up more than 80% of total insurance revenue, while the risk management business is the balance. It generates over $14 billion in annual revenue.

Gallagher posted fourth quarter and full-year earnings on January 29th, 2026, and results were better than expected on both the top and bottom lines.

The company saw adjusted earnings-per-share of $2.38, which was three cents ahead of estimates. Revenue was up almost 34% year-on-year to $3.63 billion due to significant acquisition activity in the past year, and beat estimates by $70 million.

For the full year, revenue was up 21%, organic revenue grew 6%, and adjusted EBITDAC was up 26%. Management noted that the property business was down 5%, while casualty lines were up 5%.

The dividend was raised by 7.7% to a new annualized payout of $2.80. This was the 16th consecutive year of dividend increases for Gallagher.

Click here to download our most recent Sure Analysis report on AJG (preview of page 1 of 3 shown below):

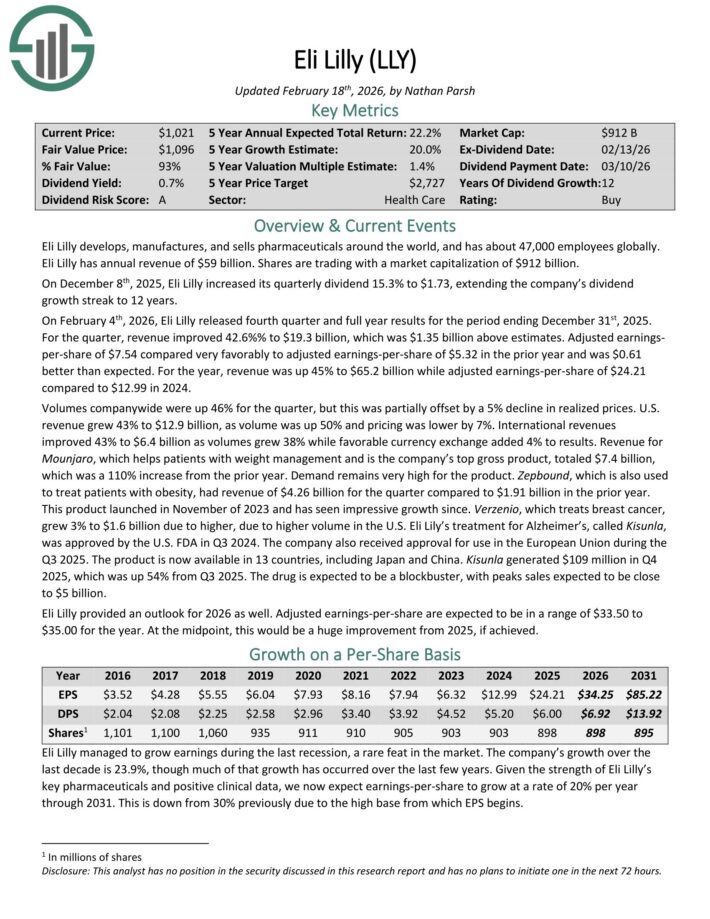

Best S&P 500 Stock #3: Eli Lilly & Co. (LLY)

Expected Annual Returns: 24.5%

Eli Lilly develops, manufactures, and sells pharmaceuticals around the world, and has about 47,000 employees globally. Eli Lilly has annual revenue of $59 billion.

On December 8th, 2025, Eli Lilly increased its quarterly dividend 15.3% to $1.73, extending the company’s dividend growth streak to 12 years.

On February 4th, 2026, Eli Lilly released fourth quarter and full year results for the period ending December 31st, 2025.

For the quarter, revenue improved 42.6%% to $19.3 billion, which was $1.35 billion above estimates. Adjusted earnings-per-share of $7.54 compared very favorably to adjusted earnings-per-share of $5.32 in the prior year and was $0.61 better than expected.

For the year, revenue was up 45% to $65.2 billion while adjusted earnings-per-share of $24.21 compared to $12.99 in 2024.

Volumes were up 46% for the quarter, but this was partially offset by a 5% decline in realized prices. U.S. revenue grew 43% to $12.9 billion, as volume was up 50% and pricing was lower by 7%.

International revenues improved 43% to $6.4 billion as volumes grew 38% while favorable currency exchange added 4% to results..

Click here to download our most recent Sure Analysis report on LLY (preview of page 1 of 3 shown below):

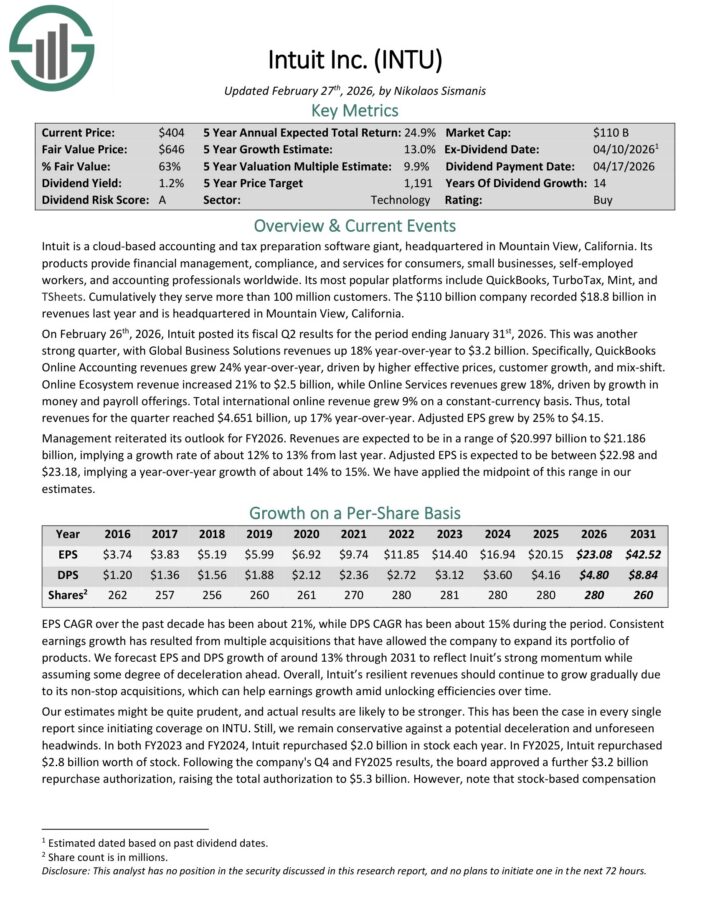

Best S&P 500 Stock #2: Intuit Inc. (INTU)

Expected Annual Returns: 27.0%

Intuit is a cloud-based accounting and tax preparation software giant, headquartered in Mountain View, California.

Its products provide financial management, compliance, and services for consumers, small businesses, self-employedworkers, and accounting professionals worldwide.

Its most popular platforms include QuickBooks, TurboTax, Mint, and TSheets. Cumulatively they serve more than 100 million customers.

The company recorded $18.8 billion in revenue last year and is headquartered in Mountain View, California.

On February 26th, 2026, Intuit posted its fiscal Q2 results for the period ending January 31st, 2026. This was another strong quarter, with Global Business Solutions revenues up 18% year-over-year to $3.2 billion.

Specifically, QuickBooks Online Accounting revenues grew 24% year-over-year, driven by higher effective prices, customer growth, and mix-shift.

Online Ecosystem revenue increased 21% to $2.5 billion, while Online Services revenues grew 18%, driven by growth in money and payroll offerings. Total international online revenue grew 9% on a constant-currency basis.

Adjusted EPS grew by 25% year-over-year, to $4.15.

Management reiterated its outlook for FY2026. Revenue is expected to be in a range of $20.997 billion to $21.186 billion, implying a growth rate of about 12% to 13% from last year.

For 2026, adjusted EPS is expected to be between $22.98 and $23.18, implying a year-over-year growth of about 14% to 15%.

Click here to download our most recent Sure Analysis report on INTU (preview of page 1 of 3 shown below):

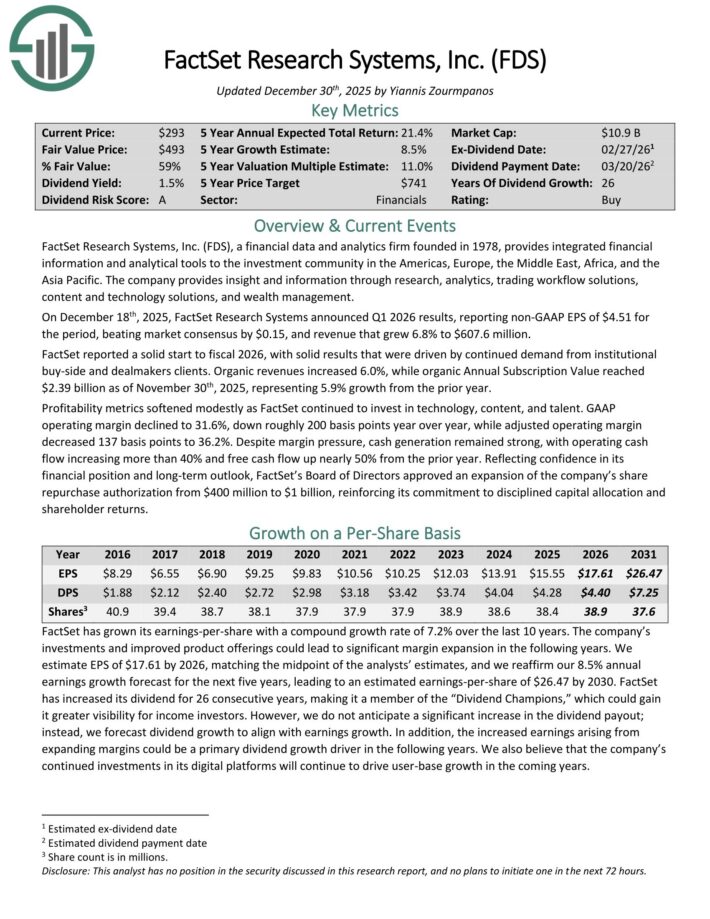

Best S&P 500 Stock #1: Factset Research Systems (FDS)

Expected Annual Returns: 27.8%

FactSet Research Systems, a financial data and analytics firm founded in 1978, provides integrated financial information and analytical tools to the investment community in the Americas, Europe, the Middle East, Africa, and Asia-Pacific.

The company provides insight and information through research, analytics, trading workflow solutions, content and technology solutions, and wealth management.

On December 18th, 2025, FactSet Research Systems announced Q1 2026 results, reporting non-GAAP EPS of $4.51 for the period, beating market consensus by $0.15, and revenue that grew 6.8% to $607.6 million.

FactSet reported a solid start to fiscal 2026, with solid results that were driven by continued demand from institutional buy-side and dealmakers clients.

Organic revenues increased 6.0%, while organic Annual Subscription Value reached $2.39 billion as of November 30th, 2025, representing 5.9% growth from the prior year.

Profitability metrics softened modestly as FactSet continued to invest in technology, content, and talent. GAAP operating margin declined to 31.6%, down roughly 200 basis points year over year, while adjusted operating margin decreased 137 basis points to 36.2%.

Despite margin pressure, cash generation remained strong, with operating cash flow increasing more than 40% and free cash flow up nearly 50% from the prior year.

Reflecting confidence in its financial position and long-term outlook, FactSet’s Board of Directors approved an expansion of the company’s share repurchase authorization from $400 million to $1 billion.

Click here to download our most recent Sure Analysis report on FDS (preview of page 1 of 3 shown below):

Additional Reading

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

Other Sure Dividend Resources

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

{kind=link}