Yves here. I hope readers in Europe and the UK and those otherwise knowledgeable about EU politics and governance will pipe up about this piece. At a bare minimum, it’s a good critical thinking exercise, but members of our commentariat can hopefully provide additional insight into regional political and economic dynamics that feed Euroskepticism.

This article makes a bold claim, that Euroskepticism actually leads to (or at least correlates with) lower growth. Its authors contend that the causality runs in the direction opposite of the one described by most economists and analysts: that economic stagnation produces “throw the bums out” voter responses, which in many cases means Euroskepticism.

Some reactions from a non-European, so take this with ample salt.

First, in opposing the conventional “falling behind economically leads to anti-establishment voting” the authors seem to be going in an “either-or” direction. I suspect that there is much more likely to be a very complex interaction. If an area of a country falls behind, some of those who can, mainly the young, will leave. So those who remain will be older and more conservative. Investors do tend to prefer areas with more demographic growth and younger workers because cheaper. This dynamic would appear to be important and I would contend more important than voting preferences.

Second, sometimes choosing to be retrograde pays off over the longer term. Portland, Maine, turned down the opportunity to become a major Ford site, IIRC in the 1930s. The arguably small-minded town fathers wanted to keep their culture. So Maine remained largely rural and poor. But it’s not hard to argue that Portland is now better situated that auto industry darling Detroit, once the wealthiest city in the US that has taken a huge fall.

Third, I wonder about their classification of Euroskeptic. The post specifically mentions Greece’s Syriza as an example. The party has likely changed its messaging, but I recall well when it took power. It campaigned on not being an establishment player and therefore uniquely able to break with existing alliances and negotiate a better bailout package than incumbents could. This may seem to be a distinction without a difference to some readers, but it was the IMF, not the EU, than devised and ran the “programs”: recall that includes lots of non-EU nations, such as Russia, Argentina, South Korea, Indonesia, Thailand, and the UK before it was part of the EU. The Bank reported in 2020 that more than half the world’s nation had asked for assistance. Yes, for Greece, the bulk of the funds actually came from EU member states, but they very much deferred to the IMF and depended on the IMF to monitor progress and devise and implement “reforms” as in austerity.

I chronicled those negotiations almost daily; there was at the time and still is a lot of misreporting of what went down. Almost no one who was Greece-sympathetic (save one MP, whose name I cannot recall) recognized that the gig was up a mere three weeks after Syriza took power. It signed a “memorandum” to get an essential mini-bailout that committed it to a yet another IMF program, fine points to be worked out.

Even more important, neither Syriza nor Greeks in 2015 were anti the EU. They were anti the IMF. From a July 2015 post (this was after the Alex Tsipras stunt of a referendum on a bailout package that had expired):

Yet quite a few pundits who claim they support self-determination for Greece advocate a Grexit despite the clear preference of Syriza leadership and the Greek public otherwise. A Bloomberg poll last week found that 81% wanted to Greece to remain in the Eurozone. That demonstrates that Greek citizens appreciate that as bad as things are under austerity, a Grexit could tip Greece into being a failed state. What is starting to happen now, the inability of companies to import, constrained access to international payment systems like debit and credit card networks, is a pale shadow of what Greece would experience with a Grexit.

Now to the main event.

By Andrés Rodríguez-Pose, Princesa de Asturias Chair and Professor of Economic Geography London School Of Economics And Political Science, Lewis Dijkstra, Urban and Head of the Territorial Analysis Team, Joint Research Centre European Commission, and Chiara Dorati. Originally published at VoxEU

Support for Euroskeptic parties has surged from the political fringes to encompass nearly a third of European voters. These movements promise a ‘free lunch’: prosperity through less integration and more national control. This column offers new evidence from across 1,166 European regions from 2004 to 2023 that Euroskepticism carries a significant economic cost. The more Euroskeptic regions have seen slower GDP per capita, productivity, and employment growth, particularly since the euro area crisis. Far from liberating local economies, Euroskepticism imposes measurable economic penalties on the very places embracing it, creating a vicious cycle of discontent and decline.

In less than two decades, Euroskepticism has moved from the margins of protest to the centre of European politics. Once confined to populist outliers – in the mid-2000s it represented a mere 3.7% of votes in national legislative elections – parties promising to ‘take back control’ now command as much as a third of the vote across EU member states. In some regions, more than half of voters now back Euroskeptic forces. The rise of such parties has reshaped electoral maps from the Po Valley to eastern Germany, from northern France to rural Sweden (Figure 1). The story being told is seductively simple: European integration has shackled prosperity. Only by reclaiming ‘sovereignty’ will prosperity be set free.

Figure 1 Change in the regional share of votes for hard Euroskeptic parties in EU national legislative elections, 2004–2008 vs 2020–2023 electoral cycles

Source: Authors’ elaboration.

Our research (Rodríguez-Pose et al. 2025) examines the consequences of the rise of Euroskcepticism and challenges this assumption head-on. Drawing on regional data for all 27 EU member states between 2004 and 2023, we ask what happens to places that turn against European integration. The analysis shows that places that yield to the temptation of Euroskepticism have, over time, grown more slowly, created fewer jobs, and lost ground in productivity relative to their more Europhile peers. In other words, Euroskepticism is no free lunch and appears not merely as a symptom of economic malaise but as a contributor to it.

Going Beyond the Causes of Euroskepticism

Most economic research to date has focused on the causes of Euroskepticism, treating it as a consequence of economic distress. The argument that long-term economic pain breeds political backlash (Rodríguez-Pose 2018) has been central to understanding its rise. The geography of EU discontent closely mirrors that of long-term stagnation (Dijkstra et al. 2020). There also appears to be a strong link between external economic threats, such as the rise of import competition from China, and anti-EU voting (Stanig and Colantone 2017).

Yet this research only covers one side of the story. What happens to economies after voters embrace Euroskeptic parties, even when these parties are not in government? Can political discontent itself become an economic liability, even before Euroskeptic forces can implement policy?

There has been no previous research directly on the consequences of Euroskepticism. The closest is work on the consequences of populism, which shows that anti-system leaders worldwide typically deliver worse economic outcomes, with GDP per capita roughly 10% lower 15 years after they take office (Funke et al. 2023). According to this research, populist leaders systematically undermine performance through institutional degradation and policy mismanagement (Funke et al. 2023).

But populism is not equivalent to Euroskepticism, and most Euroskeptic parties in Europe have rarely governed. Although some, such as Fratelli d’Italia in Italy or Fidesz in Hungary, control the levers of power, many others – such as Rassemblement National in France or Alternative für Deutschland in Germany – have remained in opposition. The question thus becomes: does merely signalling widespread Euroskepticism damage regional economic prospects?

The ‘Free Lunch’ Illusion

Euroskeptic parties across the political spectrum promise renewal through liberation from Brussels. On the far right, this means national competitiveness unburdened by EU rules; on the far left, freedom from austerity and fiscal constraint. Both traditions share a belief that regaining sovereignty will translate into renewed prosperity.

Has that been the case? We draw on a comprehensive dataset covering 1,166 European regions across all EU-27 countries from 2004 to 2023. We measure Euroskeptic support using the vote shares of parties that experts classify as opposed to European integration (scoring 2.5 or below on the Chapel Hill Expert Survey’s 1–7 scale). We then track how regions with different levels of Euroskeptic voting subsequently perform on four key development indicators: GDP per capita growth, productivity growth, employment growth, and population change.

The findings reveal that a region with a 10 percentage points higher Euroskeptic vote share experiences approximately 0.35 percentage points slower annual GDP per capita growth. This may sound modest, but compounded over multiple electoral cycles, it translates into substantial divergence. Over 12 years – three electoral cycles – such a region could find itself roughly 4%–5% poorer than an otherwise similar but less Euroskeptic neighbour.

Productivity tells a similar story. Each additional 10 points of Euroskeptic support is associated with lower annual productivity growth by about 0.10–0.14 percentage points. Employment creation lags by roughly 0.25 percentage points annually, cumulating to about 3% fewer jobs over the same period. Population effects are, by contrast, more muted, although Euroskeptic regions struggle to retain or attract residents. The relationship between Euroskeptic sentiment and subsequent economic underperformance appears robust and substantial.

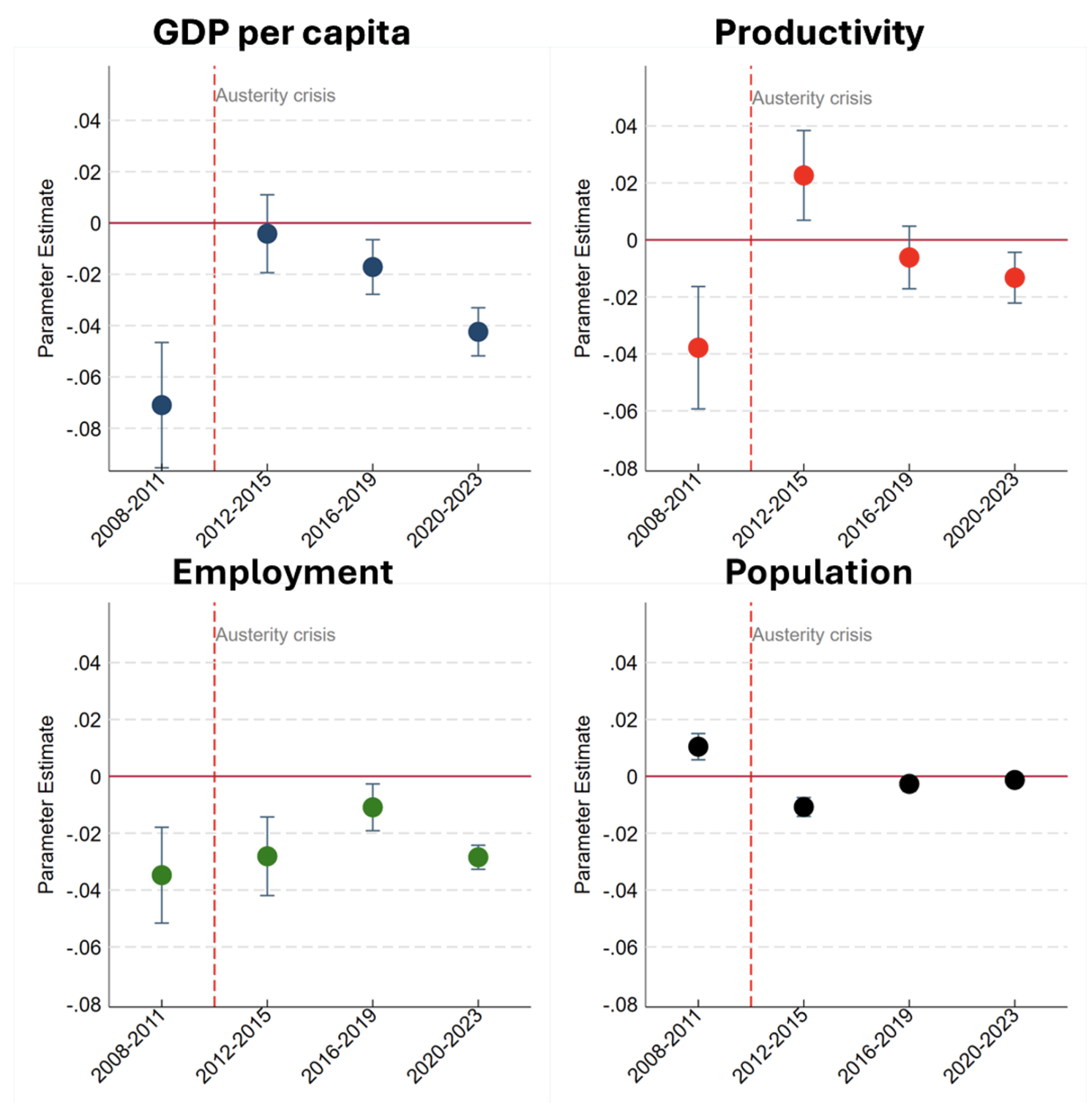

The Crisis as a Catalyst

The 2012–2013 euro area crisis and subsequent austerity acted as a critical juncture. Before the crisis, the economic penalty associated with Euroskepticism was present but muted. The crisis changed everything: citizens of regions with high Euroskeptic sentiment suffered disproportionately during and especially after this period.

For GDP per capita, the post-2012 penalty nearly doubled compared with the pre-crisis period. A region that is to points more Euroskeptic saw annual growth rates fall by an additional 0.16 percentage points after 2012, bringing the total effect to roughly 0.38 percentage points annually. By 2023, this translated into a cumulative income shortfall approaching 5.5% (Figure 2).

Figure 2 Development implications of Eurokceptic support and the crisis (event study analysis)

Note: The period on the horizontal axis refers to the period after the electoral cycle.

Why did the crisis amplify Euroskepticism’s economic impact? Several mechanisms likely operated simultaneously. First, regions vocally opposed to the EU may prove less effective at securing or deploying European funds. As Crescenzi et al. (2020) have shown, EU funds can mitigate rather than fuel Euroskepticism when properly deployed. But achieving this requires institutional capacity and a willingness to engage with EU mechanisms, precisely what Euroskeptic regions often lack (Rodríguez-Pose et al. 2024). Investors confronting scarce capital post-crisis may avoid regions perceived as politically unstable or potentially hostile to EU frameworks. The crisis also heightened regional polarisation. Regions with strong Euroskeptic sentiment may have experienced reduced social cohesion and institutional trust precisely when cooperation was most needed for recovery.

Not Just a Story About Attaining Power

Crucially, these effects materialise largely without Euroskeptic parties actually holding power. Despite their recent rapid rise, most such parties have remained in opposition, with notable exceptions such as Greece’s Syriza, Hungary’s prolonged Fidesz rule, or various Euroskeptic parties in Italy. The economic penalty therefore operates through channels beyond direct policy implementation.

High Euroskeptic vote shares may signal deep institutional distrust and political uncertainty to businesses and investors. When investors perceive hostility towards the EU or uncertainty about future relations with Brussels, capital flows slow, businesses hesitate to invest, and national investment and structural funds may be underused or diverted.

The political act of repudiating integration appears to carry economic penalties even before it translates into policy. Firms considering investments may hesitate when local electorates demonstrate hostility towards the EU frameworks that underpin the single market. Even without policy changes, widespread Euroskepticism can deter outside investment and raise perceived risk. The Brexit experience, where business investment stalled well before actual withdrawal, offers a vivid illustration of how political uncertainty alone can chill economic activity (van Oort et al. 2017). Uncertainty can ripple through regional economies long before Euroskeptics reach power.

Regional leaders in highly Euroskeptic areas may also adjust their agendas in response to strong anti-EU sentiment, leading to lower or different engagement in EU programmes, European cooperation initiatives, or business development strategies, even when those leaders are not from Euroskeptic parties themselves. The cumulative effect of such micro-decisions, multiplied across firms, governments, and individuals, can significantly alter growth trajectories.

A Vicious Cycle

These findings expose a troubling feedback loop. Economic stagnation and regional decline fuel Euroskeptic voting, as demonstrated by research on Europe’s ‘development trap’ (Diemer et al. 2022, Rodríguez-Pose et al. 2024). Many European regions have become trapped in persistent low growth, unable to adapt to structural economic change (Iammarino et al. 2020). As our analysis shows, Euroskeptic sentiment then becomes part of the problem, not just a symptom. Regions embracing Euroskeptic parties experience slower economic dynamism and prosperity, which likely further intensifies discontent, potentially driving even stronger Euroskeptic support in subsequent elections.

This dynamic creates a particularly pernicious form of path dependence. Voters in struggling regions turn to Euroskeptic parties seeking change and prosperity. Yet their choice – however understandable given their frustrations – appears to worsen their economic prospects, deepening the very stagnation that motivated the protest vote initially. The promised ‘free lunch’ of reduced EU integration delivering economic revival proves illusory. Instead, citizens in Euroskeptic regions effectively pay for their political discontent through foregone growth and missed opportunities.

Breaking the Cycle

The policy implications are profound. The solution is not to disparage Euroskeptic voters, whose grievances are often real, but to recognise the economic cost of channelling them through anti-European politics. Labelling the inhabitants of these regions as “deplorables”, as Hillary Clinton did in her failed 2016 presidential campaign, or treating their regions as lost causes will only reinforce alienation (Rodríguez-Pose 2018). Nor will simple fiscal transfers suffice (Borin et al. 2021). Money without engagement may soothe symptoms but not the underlying malaise. Left-behind people and left-behind places need honest political re-engagement alongside targeted economic reinvestment.

A dual strategy appears necessary. Politically, the EU and national governments must listen and respond to concerns about fairness, visibility, and local voice that drive Euroskepticism. Economically, targeted initiatives promoting regional development, education, access to capital, and economic diversification are essential. Recent EU initiatives such as the joint recovery fund and the emphasis on a ‘just transition’ in climate policy represent positive steps, but these must demonstrably target vulnerable regions to succeed.

Above all, humility is required. Many voters embraced Euroskeptic parties because mainstream politics failed them for too long. Yet their choice seemingly worsened their economic prospects; an irony that should give everyone pause. The problem resides not solely with voters or institutions but in their fractured relationship. Rebuilding trust in democratic institutions, including the EU’s capacity to deliver broad-based prosperity, remains paramount.

Crucially, governance and institutional quality matter. Improvements in regional institutions are often more decisive for growth than physical capital alone (Rodríguez-Pose and Ketterer 2019). Where local governments are transparent, accountable, and effective, EU funds translate into genuine development; where they are not, cynicism festers. The vicious cycle of discontent can only be broken by a virtuous one of competence.

Conclusion

Euroskepticism is no free lunch. Its rise exacts an economic toll that disproportionately affects those who expected to benefit from it. Europe’s future depends on ensuring that Euroskepticism does not become a permanent barrier to economic development across the continent. This requires more than platitudes about European unity or technocratic adjustments to cohesion policy. It demands responsive governance that helps transform today’s Euroskeptic strongholds into tomorrow’s success stories, reintegrating disenfranchised citizens into a more prosperous and unified Europe. The alternative – allowing the vicious cycle of discontent and decline to continue – risks fragmenting the European project from within, region by region, vote by vote.

See original post for references

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}