Published on October 28th, 2025 by Bob Ciura

Most investors focus primarily on the growth prospects of stocks in order to identify the most attractive holdings for their portfolios.

However, valuation is equally important. When market sentiment turns negative for a stock due to a temporary headwind, its valuation may become too cheap.

When the headwind subsides, the valuation of the stock is likely to revert to normal levels.

As a result, investors could potentially earn significant total returns by purchasing quality dividend growth stocks, when they are cheap.

The Dividend Kings are a select group of 56 stocks that have increased their dividends for at least 50 consecutive years.

We created a full list of all 56 Dividend Kings.

You can download the full list, along with important financial metrics such as dividend yields and price-to-earnings ratios, by clicking on the link below:

Stocks with low P/E ratios can offer attractive returns if their valuation multiples expand.

And when a low P/E stock also has a market-beating dividend yield, investors get ‘paid to wait’ for the valuation multiple to increase.

This article will discuss the 10 cheapest Dividend Kings right now.

Table of Contents

The table of contents below allows for easy navigation. The stocks are listed by 5-year annual return expected from an expanding valuation multiple, in ascending order.

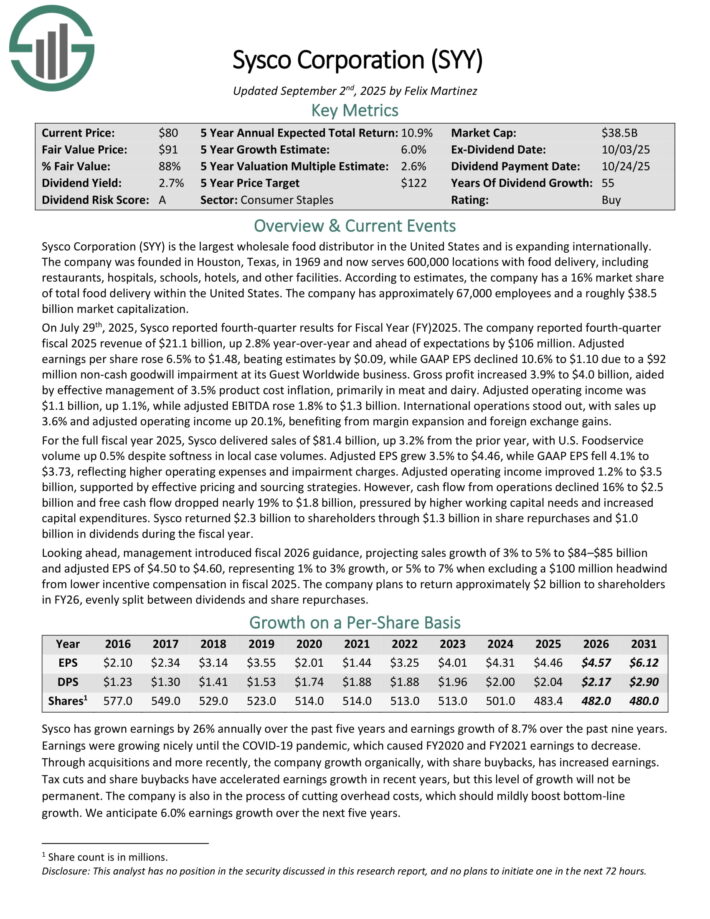

Cheapest Dividend King: Sysco Corp. (SYY)

Annual Valuation Return: 2.6%

Sysco Corporation (SYY) is the largest wholesale food distributor in the United States and is expanding internationally.The company was founded in Houston, Texas, in 1969 and now serves 600,000 locations with food delivery, includingrestaurants, hospitals, schools, hotels, and other facilities. According to estimates, the company has a 16% market shareof total food delivery within the United States.

On July 29th, 2025, Sysco reported fourth-quarter results for Fiscal Year (FY) 2025. The company reported fourth quarter fiscal 2025 revenue of $21.1 billion, up 2.8% year-over-year and ahead of expectations by $106 million.

Adjusted earnings per share rose 6.5% to $1.48, beating estimates by $0.09, while GAAP EPS declined 10.6% to $1.10 due to a $92 million non-cash goodwill impairment at its Guest Worldwide business. Gross profit increased 3.9% to $4.0 billion, aided by effective management of 3.5% product cost inflation, primarily in meat and dairy.

Adjusted operating income was $1.1 billion, up 1.1%, while adjusted EBITDA rose 1.8% to $1.3 billion. International operations stood out, with sales up 3.6% and adjusted operating income up 20.1%, benefiting from margin expansion and foreign exchange gains.

For the full fiscal year 2025, Sysco delivered sales of $81.4 billion, up 3.2% from the prior year, with U.S. Foodservice volume up 0.5% despite softness in local case volumes.

Adjusted EPS grew 3.5% to $4.46, while GAAP EPS fell 4.1% to $3.73, reflecting higher operating expenses and impairment charges. Adjusted operating income improved 1.2% to $3.5 billion, supported by effective pricing and sourcing strategies.

Cash flow from operations declined 16% to $2.5 billion and free cash flow dropped nearly 19% to $1.8 billion, pressured by higher working capital needs and increased capital expenditures.

Sysco returned $2.3 billion to shareholders through $1.3 billion in share repurchases and $1.0 billion in dividends during the fiscal year.

Looking ahead, management introduced fiscal 2026 guidance, projecting sales growth of 3% to 5% to $84–$85 billion and adjusted EPS of $4.50 to $4.60, representing 1% to 3% growth, or 5% to 7% when excluding a $100 million headwind from lower incentive compensation in fiscal 2025.

The company plans to return approximately $2 billion to shareholders in FY26, evenly split between dividends and share repurchases.

Click here to download our most recent Sure Analysis report on SYY (preview of page 1 of 3 shown below):

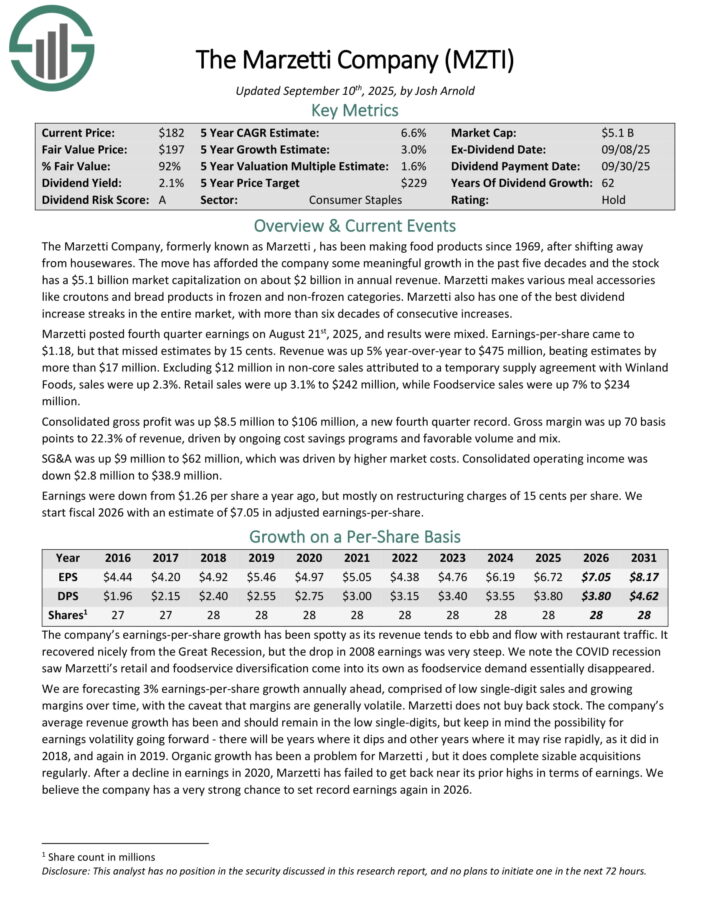

Cheapest Dividend King: The Marzetti Company (MZTI)

Annual Valuation Return: 3.7%

The Marzetti Company has been making food products since 1969, after shifting away from housewares.

Marzetti makes various meal accessories like croutons and bread products in frozen and non-frozen categories. Marzetti also has one of the best dividend increase streaks in the entire market, with more than six decades of consecutive increases.

Marzetti posted fourth quarter earnings on August 21st, 2025, and results were mixed. Earnings-per-share came to $1.18, but that missed estimates by 15 cents. Revenue was up 5% year-over-year to $475 million, beating estimates by more than $17 million.

Excluding $12 million in non-core sales attributed to a temporary supply agreement with Winland Foods, sales were up 2.3%. Retail sales were up 3.1% to $242 million, while Foodservice sales were up 7% to $234 million.

Consolidated gross profit was up $8.5 million to $106 million, a new fourth quarter record. Gross margin was up 70 basis points to 22.3% of revenue, driven by ongoing cost savings programs and favorable volume and mix.

SG&A was up $9 million to $62 million, which was driven by higher market costs. Consolidated operating income was down $2.8 million to $38.9 million.

Earnings were down from $1.26 per share a year ago, but mostly on restructuring charges of 15 cents per share.

Click here to download our most recent Sure Analysis report on MZTI (preview of page 1 of 3 shown below):

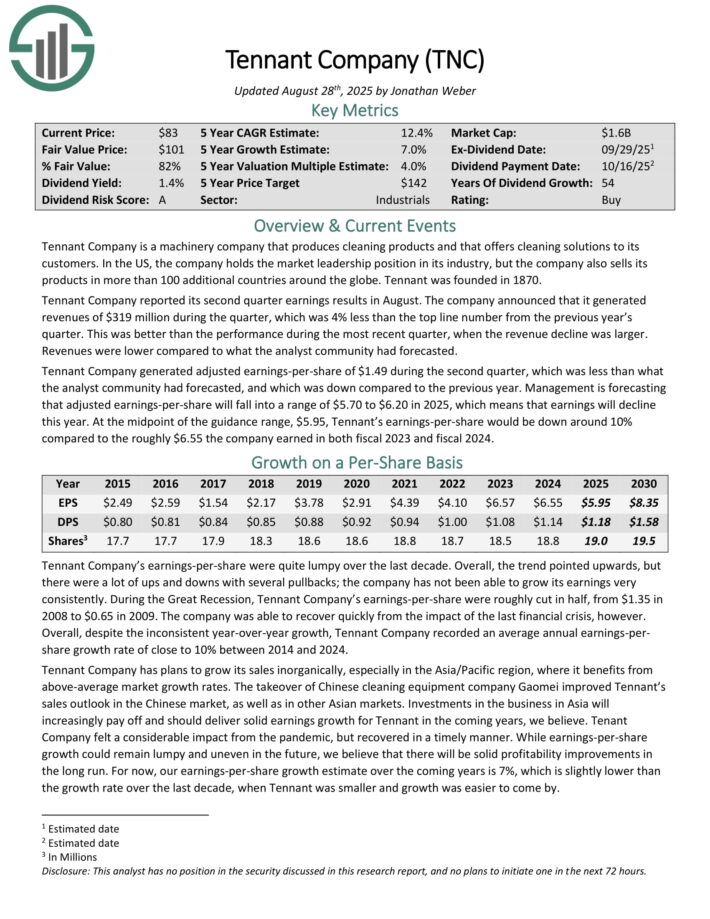

Cheapest Dividend King: Tennant Co. (TNC)

Annual Valuation Return: 4.3%

Tennant Company is a machinery company that produces cleaning products and that offers cleaning solutions to its customers.

In the US, the company holds the market leadership position in its industry, but the company also sells its products in more than 100 additional countries around the globe. Tennant was founded in 1870.

Tennant Company reported its second quarter earnings results in August. The company announced that it generated revenues of $319 million during the quarter, which was 4% less than the top line number from the previous year’s quarter.

This was better than the performance during the most recent quarter, when the revenue decline was larger. Revenues were lower compared to what the analyst community had forecasted.

Tennant Company generated adjusted earnings-per-share of $1.49 during the second quarter, which was less than what the analyst community had forecasted, and which was down compared to the previous year.

Management is forecasting that adjusted earnings-per-share will fall into a range of $5.70 to $6.20 in 2025, which means that earnings will decline this year. At the midpoint of the guidance range, $5.95, Tennant’s earnings-per-share would be down around 10%.

Click here to download our most recent Sure Analysis report on TNC (preview of page 1 of 3 shown below):

Cheapest Dividend King: Hormel Foods (HRL)

Annual Valuation Return: 4.8%

Hormel was founded back in 1891 in Minnesota. Since that time, the company has grown into a juggernaut in the food products industry with nearly $10 billion in annual revenue.

Hormel has kept with its core competency as a processor of meat products for well over a hundred years, but has also grown into other business lines through acquisitions.

Hormel has a large portfolio of category-leading brands. Just a few of its top brands include include Skippy, SPAM, Applegate, Justin’s, and more than 30 others.

Hormel posted third quarter earnings on August 28th, 2025, and results were very weak, including disappointing guidance for the fourth quarter.

Adjusted earnings-per-share came to 35 cents, which was six cents light of estimates. Revenue was up 4.5% year-over-year to $3.03 billion, beating estimates by $50 million. Organic net sales were up 6% year-over-year on volume gains of 4%, with price and mix comprising the other 2%.

The company also noted its cost savings program is working and helping save about $125 million annually. Gross profit was flat year-on-year, with inflationary headwinds offset by top line gains. The company noted 400 basis points of raw material cost inflation, a massive headwind to margins.

Cash flow from operations were $157 million, while capex was $72 million, and dividends paid were $159 million. Guidance for Q4 was for net sales of ~$3.2 billion, about $50 million light of consensus. Earnings are expected at ~39 cents.

Click here to download our most recent Sure Analysis report on HRL (preview of page 1 of 3 shown below):

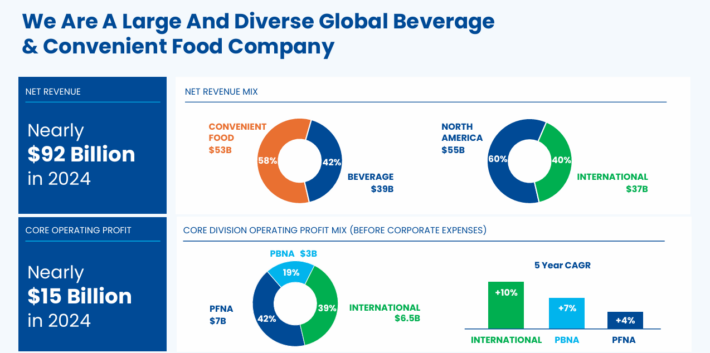

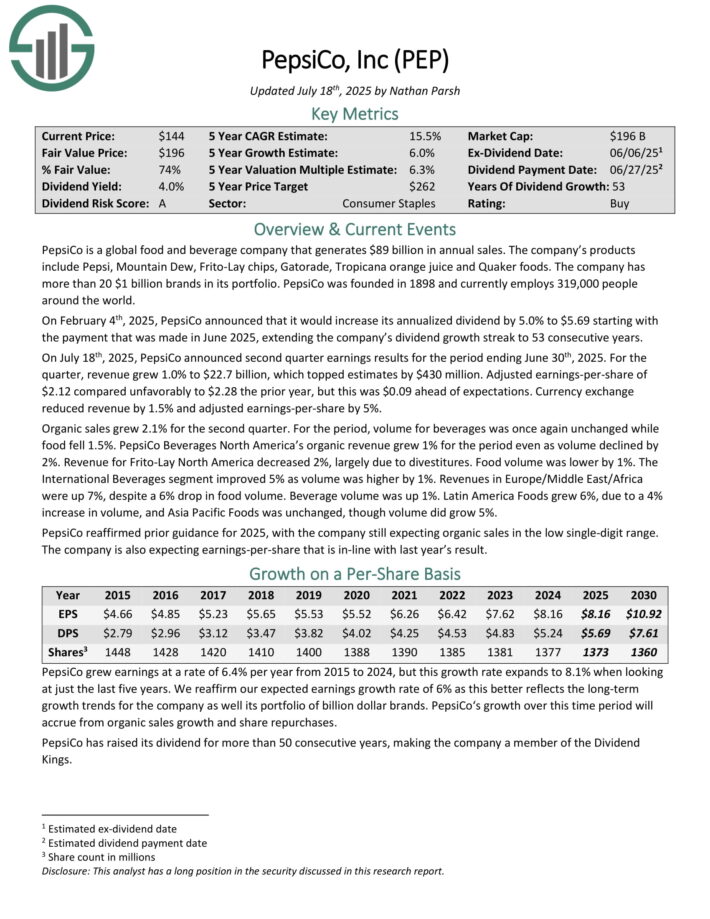

Cheapest Dividend King: PepsiCo Inc. (PEP)

Annual Valuation Return: 5.1%

PepsiCo is a global food and beverage company. Its products include Pepsi, Mountain Dew, Frito-Lay chips, Gatorade, Tropicana orange juice and Quaker foods.

Its business is split roughly 60-40 in terms of food and beverage revenue. It is also balanced geographically between the U.S. and the rest of the world.

Source: Investor Presentation

On July 18th, 2025, PepsiCo announced second quarter earnings results for the period ending June 30th, 2025. For the quarter, revenue grew 1.0% to $22.7 billion, which topped estimates by $430 million.

Adjusted earnings-per-share of $2.12 compared unfavorably to $2.28 the prior year, but this was $0.09 ahead of expectations. Currency exchange reduced revenue by 1.5% and adjusted earnings-per-share by 5%.

Organic sales grew 2.1% for the second quarter. For the period, volume for beverages was once again unchanged while food fell 1.5%.

Click here to download our most recent Sure Analysis report on PEP (preview of page 1 of 3 shown below):

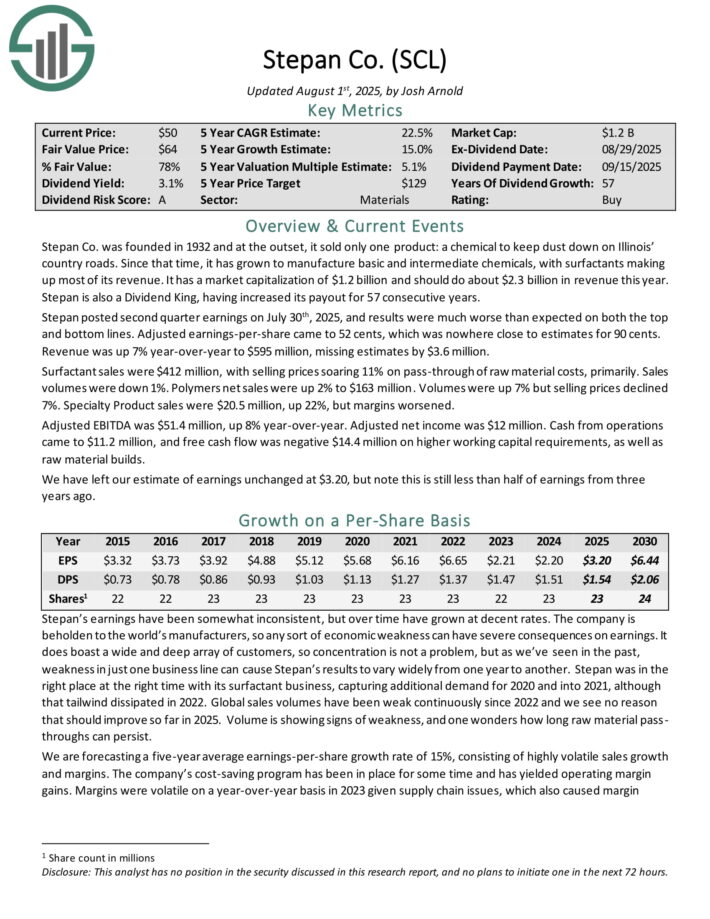

Cheapest Dividend King: Stepan Co. (SCL)

Annual Valuation Return: 7.1%

Stepan manufactures basic and intermediate chemicals, including surfactants, specialty products, germicidal and fabric softening quaternaries, phthalic anhydride, polyurethane polyols and special ingredients for the food, supplement, and pharmaceutical markets.

It is organized into three distinct business lines: surfactants, polymers, and specialty products. These businesses serve a wide variety of end markets.

The surfactants business is Stepan’s largest by revenue. A surfactant is an organic compound that contains both water-soluble and water-insoluble components.

Stepan posted second quarter earnings on July 30th, 2025, and results were much worse than expected on both the top and bottom lines. Adjusted earnings-per-share came to 52 cents, which was nowhere close to estimates for 90 cents. Revenue was up 7% year-over-year to $595 million, missing estimates by $3.6 million.

Surfactant sales were $412 million, with selling prices soaring 11% on pass-through of raw material costs, primarily. Sales volumes were down 1%. Polymers net sales were up 2% to $163 million. Volumes were up 7% but selling prices declined 7%. Specialty Product sales were $20.5 million, up 22%, but margins worsened.

Adjusted EBITDA was $51.4 million, up 8% year-over-year. Adjusted net income was $12 million. Cash from operations came to $11.2 million, and free cash flow was negative $14.4 million on higher working capital requirements, as well as raw material builds.

Click here to download our most recent Sure Analysis report on SCL (preview of page 1 of 3 shown below):

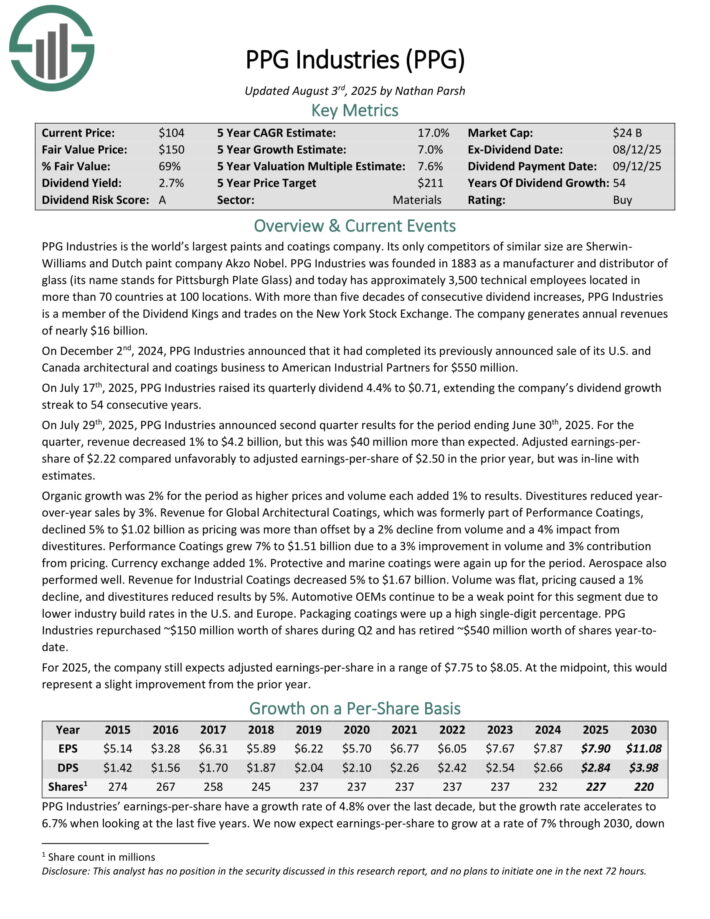

Cheapest Dividend King: PPG Industries (PPG)

Annual Valuation Return: 7.3%

PPG Industries is the world’s largest paints and coatings company. Its only competitors of similar size are Sherwin-Williams and Dutch paint company Akzo Nobel.

PPG Industries was founded in 1883 as a manufacturer and distributor of glass (its name stands for Pittsburgh Plate Glass) and today has approximately 3,500 technical employees located in more than 70 countries at 100 locations.

On July 17th, 2025, PPG Industries raised its quarterly dividend 4.4% to $0.71, extending the company’s dividend growth streak to 54 consecutive years.

On July 29th, 2025, PPG Industries announced second-quarter results. For the quarter, revenue decreased 1% to $4.2 billion, but this was $40 million more than expected. Adjusted earnings-per-share of $2.22 compared unfavorably to adjusted earnings-per-share of $2.50 in the prior year, but was in-line with estimates.

Organic growth was 2% for the period as higher prices and volume each added 1% to results. Divestitures reduced year-over-year sales by 3%. Revenue for Global Architectural Coatings declined 5% to $1.02 billion as pricing was more than offset by a 2% decline from volume and a 4% impact from divestitures.

Performance Coatings grew 7% to $1.51 billion due to a 3% improvement in volume and 3% contribution from pricing. Currency exchange added 1%. Protective and marine coatings were again up for the period.

PPG Industries repurchased ~$150 million worth of shares during Q2 and has retired ~$540 million worth of shares year-to-date.

Click here to download our most recent Sure Analysis report on PPG (preview of page 1 of 3 shown below):

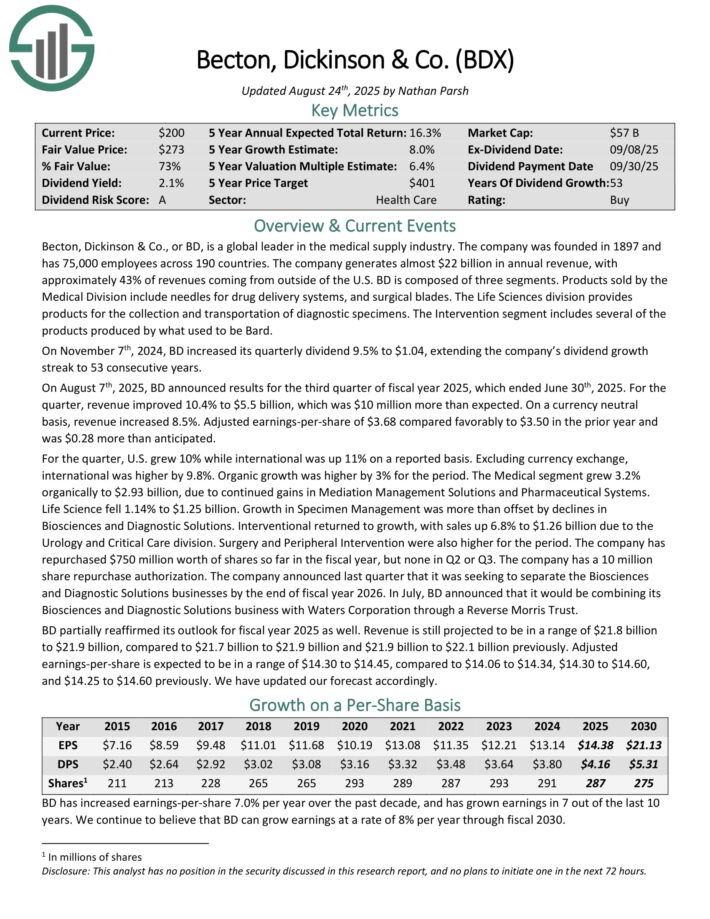

Cheapest Dividend King: Becton Dickinson & Co. (BDX)

Annual Valuation Return: 7.9%

Becton, Dickinson & Co. is a global leader in the medical supply industry. The company was founded in 1897 and has 75,000 employees across 190 countries.

The company generates about $20 billion in annual revenue, with approximately 43% of revenues coming from outside of the U.S.

Becton, Dickinson & Co., or BD, is a global leader in the medical supply industry. The company generates almost $22 billion in annual revenue, with approximately 43% of revenues coming from outside of the U.S.

On August 7th, 2025, BD announced results for the third quarter of fiscal year 2025, which ended June 30th, 2025. For the quarter, revenue improved 10.4% to $5.5 billion, which was $10 million more than expected.

On a currency neutral basis, revenue increased 8.5%. Adjusted earnings-per-share of $3.68 compared favorably to $3.50 in the prior year and was $0.28 more than anticipated.

For the quarter, U.S. grew 10% while international was up 11% on a reported basis. Excluding currency exchange, international was higher by 9.8%. Organic growth was higher by 3% for the period.

BD partially reaffirmed its outlook for fiscal year 2025 as well. Revenue is still projected to be in a range of $21.8 billion to $21.9 billion, compared to $21.7 billion to $21.9 billion previously. Adjusted earnings-per-share is expected to be in a range of $14.30 to $14.45.

Click here to download our most recent Sure Analysis report on BDX (preview of page 1 of 3 shown below):

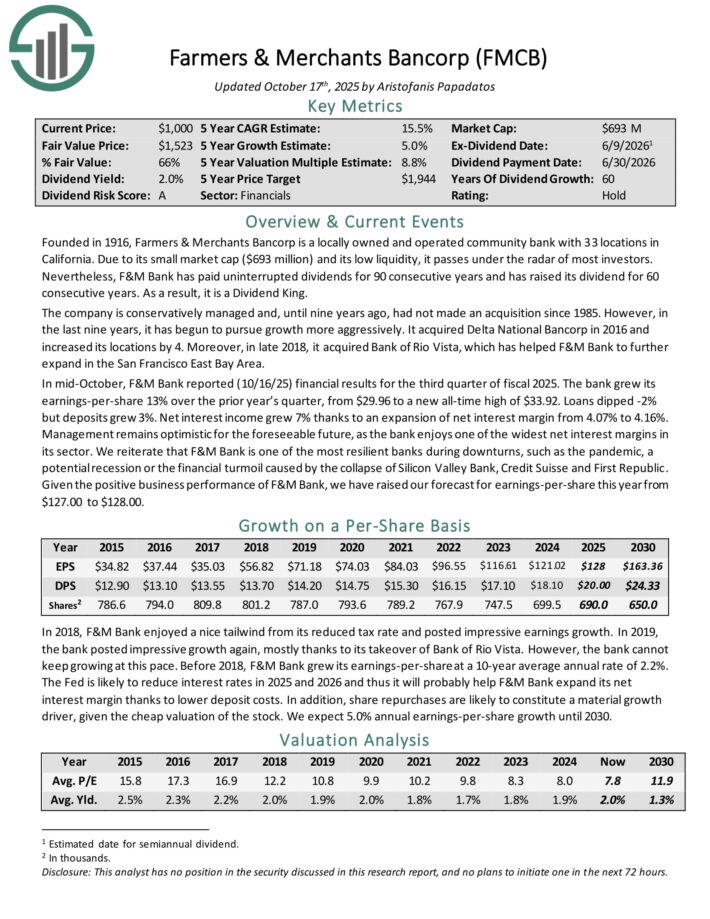

Cheapest Dividend King: Farmers & Merchants Bancorp (FMCB)

Annual Valuation Return: 8.3%

Founded in 1916, Farmers & Merchants Bancorp is a locally owned and operated community bank with 33 locations in California. Due to its small market cap and its low liquidity, it passes under the radar of most investors.

Nevertheless, F&M Bank has paid uninterrupted dividends for 90 consecutive years and has raised its dividend for 60 consecutive years. As a result, it is a Dividend King.

The company is conservatively managed and, until nine years ago, had not made an acquisition since 1985. However, in the last nine years, it has begun to pursue growth more aggressively.

It acquired Delta National Bancorp in 2016 and increased its locations by 4. Moreover, in late 2018, it acquired Bank of Rio Vista, which has helped F&M Bank to further expand in the San Francisco East Bay Area.

In mid-October, F&M Bank reported (10/16/25) financial results for the third quarter of fiscal 2025. The bank grew its earnings-per-share 13% over the prior year’s quarter, from $29.96 to a new all-time high of $33.92. Loans dipped -2% but deposits grew 3%. Net interest income grew 7% thanks to an expansion of net interest margin from 4.07% to 4.16%.

Click here to download our most recent Sure Analysis report on FMCB (preview of page 1 of 3 shown below):

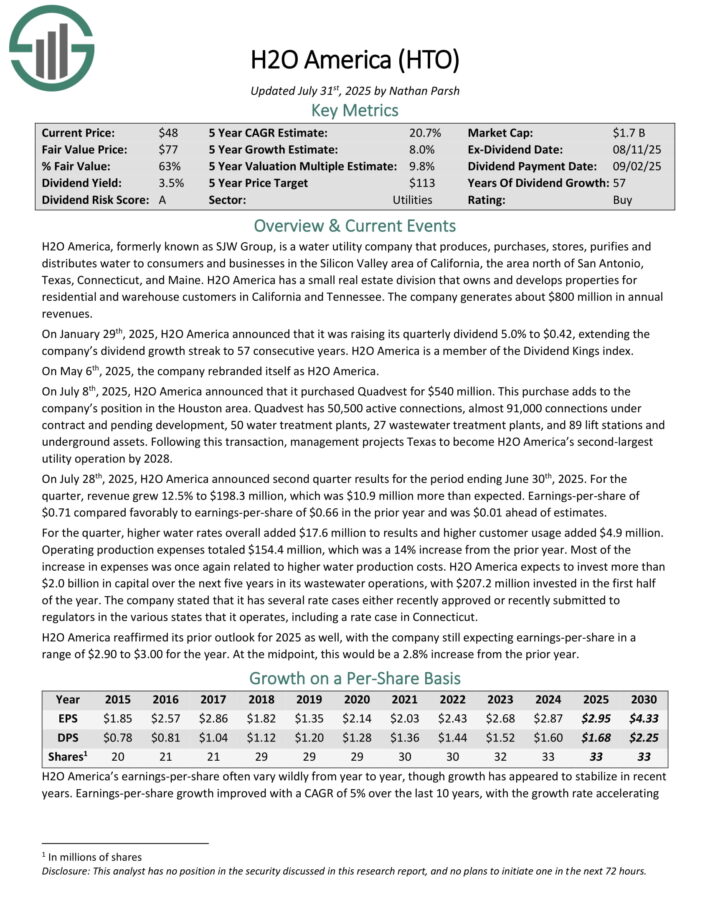

Cheapest Dividend King: H2O America (HTO)

Annual Valuation Return: 9.0%

H2O America, formerly known as SJW Group, is a water utility company that produces, purchases, stores, purifies and distributes water to consumers and businesses in the Silicon Valley area of California, the area north of San Antonio, Texas, Connecticut, and Maine.

It also has a small real estate division that owns and develops properties for residential and warehouse customers in California and Tennessee. The company generates about $670 million in annual revenues.

On July 8th, 2025, H2O America announced that it purchased Quadvest for $540 million. This purchase adds to the company’s position in the Houston area.

Quadvest has 50,500 active connections, almost 91,000 connections under contract and pending development, 50 water treatment plants, 27 wastewater treatment plants, and 89 lift stations and underground assets.

On July 28th, 2025, H2O America announced second quarter results for the period ending June 30th, 2025. For the quarter, revenue grew 12.5% to $198.3 million, which was $10.9 million more than expected.

Earnings-per-share of $0.71 compared favorably to earnings-per-share of $0.66 in the prior year and was $0.01 ahead of estimates.

For the quarter, higher water rates overall added $17.6 million to results and higher customer usage added $4.9 million. Operating production expenses totaled $154.4 million, which was a 14% increase from the prior year.

Click here to download our most recent Sure Analysis report on HTO (preview of page 1 of 3 shown below):

Additional Reading

The following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Judge Who Helped Violent Illegal Alien Evade ICE Faces New Test")

{kind=link}